What Does Medicare Supplemental Insurance Cover?

If you are getting close to age 65, already on Medicare, or helping a parent compare plans, you may be asking one of the most important Medicare questions:

What does Medicare Supplemental Insurance cover?

That is a smart question.

It is also a question that confuses many people.

Many people hear the words Medicare Supplement Insurance and assume it means “extra insurance that covers everything Medicare does not.” That sounds reasonable, but it is not how the program works. Medicare says Medicare Supplement Insurance, also called Medigap, is extra insurance you can buy from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare. Medicare specifically states that these costs can include copayments, coinsurance, and deductibles. (Medicare)

So the short answer is this:

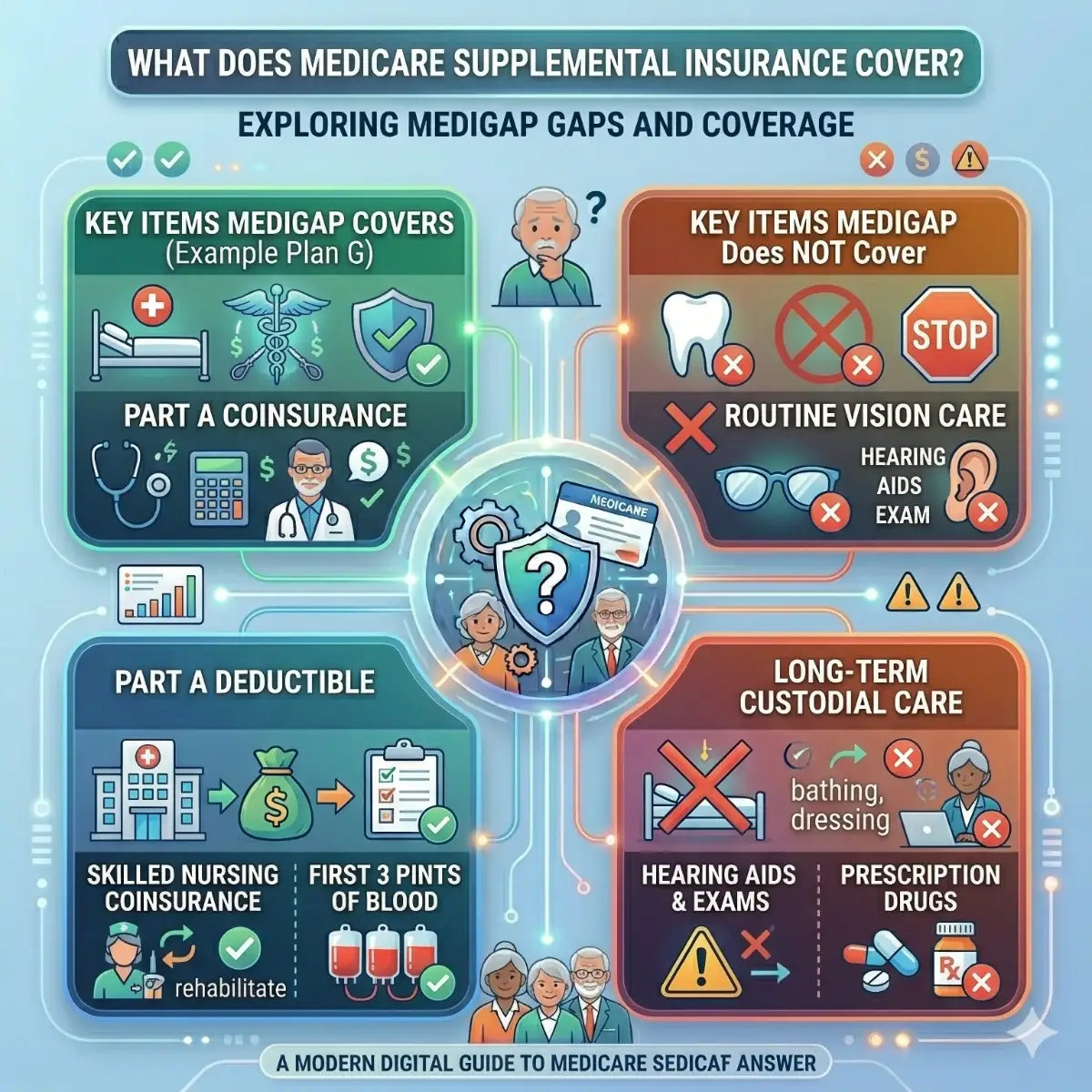

Medicare Supplemental Insurance covers some of the bills left over after Original Medicare Part A and Part B pay their share. It does not replace Medicare, and it does not usually create large new categories of coverage such as routine dental, routine vision, hearing aids, or prescription drugs. Medicare says Medigap plans help cover your share of costs for services that are covered by Original Medicare (Part A and Part B), and it also says Medigap plans sold after 2005 do not include prescription drug coverage. (Medicare)

That means Medigap is best understood as a cost-sharing helper, not an all-purpose health plan.

This matters because Original Medicare covers many important medical services, but Medicare says it does not have a yearly limit on what you pay out of pocket on its own. That is one big reason people buy Medigap. They want help paying the deductibles, coinsurance, and copayments that Medicare leaves behind. (Medicare)

But Medigap plans are not all the same.

Medicare says there are 10 different types of Medigap plans in most states, named by letters A–D, F, G, and K–N. The benefits in each lettered plan are standardized, meaning the same letter provides the same basic benefits no matter which company sells it. But different letter plans cover different things. Medicare also notes that Massachusetts, Minnesota, and Wisconsin standardize Medigap differently. (Medicare)

So the real answer to “What does Medicare Supplemental Insurance cover?” is:

It depends on the Medigap plan letter you choose, but in general, Medigap helps cover some of the out-of-pocket costs tied to Medicare-covered hospital and medical services.

This guide explains that in plain English.

It will show you:

- What Medigap is

- What it covers in general

- which benefits many plans include

- What some plans cover only partly

- What Medigap does not cover

- How Medigap is different from Medicare Advantage

- and how to think about whether Medigap may fit your needs

All of the factual details below come from official Medicare sources. (Medicare)

The short answer in plain English

If you want the fastest, most useful answer before going deeper, here it is.

Medicare says Medigap plans help cover your share of costs for services covered by Original Medicare Part A and Part B. That means Medigap may help pay things like:

- deductibles

- coinsurance

- copayments

- and certain other cost-sharing, depending on the plan letter you buy. (Medicare)

Medicare’s official Medigap comparison chart shows that different plans may help cover:

- Part A coinsurance and hospital costs

- Part B coinsurance or copayment

- blood (the first 3 pints)

- Part A hospice care coinsurance or copayment

- skilled nursing facility care coinsurance

- Part A deductible

- Part B excess charges in some plans

- and foreign travel emergency costs up to plan limits in some plans. (Medicare)

But Medigap usually does not cover everything people hope it will.

Medicare says Medigap policies generally do not cover:

- long-term care

- vision

- dental

- hearing aids

- eyeglasses

- private-duty nursing

- and, for plans sold after 2005, prescription drugs. (Medicare)

So the clearest short answer is:

Medicare Supplemental Insurance covers many of the out-of-pocket costs left behind by Original Medicare. Still, it does not usually cover services that Medicare does not cover in the first place. (Medicare)

First, what Medicare Supplemental Insurance is

To understand what Medigap covers, you first need to understand what it is.

Medicare says Medigap is extra insurance you buy from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare. Medicare also says you generally must have Original Medicare — Part A and Part B — to buy a Medigap policy. (Medicare)

That definition matters a lot.

Medigap is not:

- another official “part” of Medicare

- a stand-alone health plan that replaces Medicare

- or a broad catch-all policy for every expense people face as they age

Instead, it is a supplement to Original Medicare. Medicare’s “How Medigap works” page says exactly that: a Medigap policy is a supplement to Original Medicare coverage. (Medicare)

That means the order is important.

First, Original Medicare Part A and Part B cover approved services under Medicare’s rules.

Then, Medigap may help with some of the remaining bills. (Medicare)

So if you want one memory sentence, use this:

Medigap covers Medicare’s cost-sharing gaps, not all gaps in health care. (Medicare)

Why do people buy Medigap in the first place

The main reason people buy Medigap is simple.

Original Medicare does not pay for everything.

Medicare’s Medigap guide says Original Medicare pays for many, but not all, health care services and supplies. Medicare’s cost information also explains that what you pay depends on the care you use and the coverage you have. (Medicare)

That means even if Medicare approves and pays for your hospital or outpatient care, you may still owe Part of the bill yourself.

Depending on the service, that may include:

- a deductible

- a coinsurance amount

- a copayment

- or another cost-sharing charge. Medicare says those are exactly the kinds of costs Medigap is built to help with. (Medicare)

This is why people often compare Medigap plans soon after they enroll in Part B.

They are not trying to replace Medicare.

They are trying to reduce the financial risk associated with Medicare’s leftover cost-sharing. (Medicare)

Medigap only works with Original Medicare

This point is one of the most important in the entire article.

Medicare says a Medigap policy is a supplement to Original Medicare. It also says a Medigap policy is different from a Medicare Advantage Plan (Part C). When you are getting started with Medicare, Medicare says you can either buy Medigap or enroll in a Medicare Advantage Plan, but you can’t have both in the normal way. (Medicare)

That means Medigap is designed for people who keep:

- Part A, which is hospital insurance

- and Part B, which is medical insurance. Medicare’s parts page clearly lays out that structure. (Medicare)

This matters because people sometimes ask:

“Will my Medigap plan cover this?”

The better question is often:

“Does Original Medicare cover this service first?” (Medicare)

If the answer is no, then Medigap usually does not create brand-new coverage for that service. That is why understanding Original Medicare is the first step to understanding Medigap. (Medicare)

The main categories Medigap can cover

Now let’s answer the keyword directly and in detail.

Medicare’s official Medigap plan comparison chart shows the categories of benefits that Medigap plans may cover. These include:

1. Part A coinsurance and hospital costs

Medicare’s chart says all standardized Medigap plans help cover Part A coinsurance and hospital costs for up to an additional 365 days after Medicare benefits are exhausted. That is one of the strongest and most universal Medigap protections. (Medicare)

This matters because if you have a long hospital stay, hospital-related cost-sharing can become large. Medigap is designed to soften that risk. (Medicare)

2. Part B coinsurance or copayment

Medicare’s chart also shows that Medigap plans help with Part B coinsurance or copayment, though not every plan covers it in the same way. Some plans cover it fully, and Plans K and L cover it partly. Plan N has special notes about copayments in some situations. (Medicare)

This is important because Part B covers many day-to-day health care services, such as doctor visits, outpatient care, and medical equipment. Medigap may help reduce the recurring bills associated with that care. (Medicare)

3. Blood benefit

Medicare’s chart says Medigap plans may cover the first 3 pints of blood. Again, some plans cover this fully, while others cover it partially. (Medicare)

This is not the most famous Medigap feature, but it is Part of the standardized benefit structure Medicare uses. (Medicare)

4. Part A hospice care coinsurance or copayment

Medicare’s chart also lists Part A hospice care coinsurance or copayment as a covered Medigap category. Many plans cover it fully, while Plans K and L cover Part of it. (Medicare)

This means Medigap may help lower some hospice-related cost-sharing under Original Medicare. (Medicare)

5. Skilled nursing facility care coinsurance

Medicare says many Medigap plans cover skilled nursing facility care coinsurance, with some plans covering 100% and others less. (Medicare)

This is another important cost-sharing area because post-hospital skilled care can create bills under Medicare’s rules. Medigap may help soften those bills. (Medicare)

6. Part A deductible

Medicare’s chart shows that many Medigap plans cover the Part A deductible, either fully or partly. Plan A does not cover it. Plans K, L, and M cover it partly. Several other plans cover it fully. (Medicare)

This is a big deal because Medicare’s costs page says the 2026 Part A deductible is $1,736 per inpatient hospital benefit period. So a Medigap plan that covers the Part A deductible can save you a meaningful amount of money during a hospital stay. (Medicare)

7. Part B excess charges

Medicare’s chart says some Medigap plans cover Part B excess charges, while others do not. (Medicare)

This is another example of how different plan letters cover different things. It is one reason people compare letter plans carefully rather than just choosing the lowest premium. (Medicare)

8. Foreign travel emergency

Medicare’s chart says some Medigap plans cover foreign travel emergency costs up to plan limits, usually at 80%. Not every plan includes this benefit. (Medicare)

This can matter a lot for people who travel internationally and want some limited emergency protection outside the United States. (Medicare)

So if you want the simplest summary of what Medigap covers, it is this:

Medigap mainly covers cost-sharing for hospital and medical services under Original Medicare. (Medicare)

What all standardized Medigap plans cover

It also helps to know what almost every standard Medigap structure starts with.

Medicare’s chart shows that Part A coinsurance and hospital costs up to an additional 365 days after Medicare benefits are used up is a core benefit across standardized Medigap plans. Many of the plans also include at least some help with Part B coinsurance or copayment, blood, and hospice cost-sharing. (Medicare)

This is why Medigap is often viewed as a hospital-and-medical bill protector rather than a brand-new medical benefit system.

It is not changing what Original Medicare covers.

It is lowering what you may owe when Original Medicare covers something. (Medicare)

What some Medigap plans cover only partly

Another thing many people do not realize is that some Medigap plans do not fully cover certain benefits.

Medicare’s chart shows that:

- Plan K covers some benefits at 50%

- Plan L covers some benefits at 75%

- Plan M covers some benefits only partially

- And Plan N has special copayment rules for some Part B services. (Medicare)

This matters because two people can both say they have “Medigap,” but their actual out-of-pocket experience may be very different.

One person may have a plan with broad protection.

Another may have a lower-premium plan that leaves more cost-sharing in place. (Medicare)

So the question is not only:

“What does Medigap cover?”

It is also:

“Which Medigap plan letter am I talking about?” (Medicare)

The role of plan letters

Medicare says there are 10 different types of Medigap plans offered in most states, named by letters A–D, F, G, and K–N. It also says all Medigap policies are standardized, which means policies with the same letter offer the same basic benefits no matter where you live or which insurance company you buy from. Medicare also says price is the only difference between plans with the same letter that different insurance companies sell. (Medicare)

This is one of the most helpful Medigap facts for shoppers.

If you are comparing two Plan G policies, the core benefits are the same.

If you are comparing Plan G and Plan N, the benefits differ. (Medicare)

That means the smart order is:

- Pick the plan letter that fits your needs,

- then compare companies selling that same letter plan. (Medicare)

This helps explain what Medigap covers in a very practical way.

What Medigap does not cover

Now let’s cover the other side of the keyword, because this is where many people make expensive assumptions.

Medicare says Medigap plans help cover your share of costs for services covered by Original Medicare Parts A and B. That means Medigap usually does not create big new service categories that Medicare does not cover in the first place. (Medicare)

Medicare specifically says Medigap plans generally don’t cover:

- long-term care

- vision

- dental

- hearing aids

- eyeglasses

- private-duty nursing. (Medicare)

Medicare also says Medigap plans sold after 2005 do not include prescription drug coverage. If you want drug coverage, you can join a separate Medicare drug plan, which is Part D. (Medicare)

This is a major point.

A lot of people hear “supplement” and assume it means:

“extra help with whatever Medicare does not pay.”

But Medicare defines Medigap much more narrowly. It is mainly about deductibles, coinsurance, and copayments for covered Original Medicare services. (Medicare)

So the cleanest sentence here is:

Medigap covers many Medicare cost gaps but few service gaps. (Medicare)

Does Medigap cover prescriptions?

This deserves its own section because it is one of the most common points of confusion.

Medicare says Medigap plans sold after 2005 do not include prescription drug coverage. It says that if you want drug coverage, you can join a separate Medicare drug plan, which is Part D. (Medicare)

That means:

- Medigap is not your modern prescription plan

- Part D is your prescription plan if you stay with Original Medicare. (Medicare)

This matters because if someone mistakenly assumes their Medigap policy covers prescriptions and never joins Part D, Medicare may later impose a late-enrollment penalty if they go too long without creditable drug coverage before enrolling. (Medicare)

So, Medigap does not just fail to cover prescriptions in most current cases. Confusing it with Part D can create real financial problems later.

Does Medigap cover dental, vision, and hearing?

Usually no.

Medicare says Medigap generally does not cover vision, dental, hearing aids, or eyeglasses. (Medicare)

This surprises many people because these are common real-life needs as people age.

If those benefits matter a lot to you, Medicare says some Medicare Advantage plans may offer extra benefits that Original Medicare does not cover, such as vision, hearing, and dental services. But that is a different path from Medigap. (Medicare)

So if you want Medigap mainly because you hope it will pay for routine dental cleanings, glasses, or hearing aids, Medicare’s official rules say that expectation is usually wrong. (Medicare)

Does Medigap cover long-term care?

Usually no.

Medicare’s Medigap materials say long-term care is generally not covered by Medigap. (Medicare)

This is one of the most important non-coverage points because families often assume that a Medicare supplement must help with nursing home or long-term home care costs.

But Medigap is not long-term care insurance. It is a cost-sharing help for Original Medicare services. (Medicare)

So if long-term care planning is one of your main goals, Medigap is usually not the right product for that.

How Medigap is different from Medicare Advantage

This is one of the biggest misunderstandings in Medicare.

Medicare says a Medigap policy is different from a Medicare Advantage Plan (Part C). A Medicare Advantage plan is another way to get your Medicare coverage, in addition to Original Medicare. A Medigap policy is a supplement to Original Medicare coverage. When you’re getting started with Medicare, Medicare says you can either buy Medigap or enroll in a Medicare Advantage Plan, but you can’t have both in the normal way. (Medicare)

That means:

- Medigap works with Original Medicare

- Medicare Advantage replaces Original Medicare as your delivery system for Medicare-covered benefits. (Medicare)

This is a huge structural difference.

Original Medicare + Medigap

You keep Part A and Part B as your base coverage.

Then, Medigap helps with some leftover cost-sharing.

You may also add a separate Part D drug plan. (Medicare)

Medicare Advantage

You get your Part A and Part B benefits through a private Medicare-approved plan instead.

Most plans also include Part D.

Many include extra benefits.

Many use provider networks and plan rules. (Medicare)

This matters because some people ask what Medigap covers when they are really deciding between supplemental protection and bundled plan coverage. Those are two different Medicare paths. (Medicare)

Why do people buy Medigap

People usually buy Medigap for one big reason:

They want help paying the cost-sharing that Original Medicare leaves behind.

Medicare’s Medigap guide says Original Medicare pays for many, but not all, health care services and supplies. Medigap exists to help pay your share of those out-of-pocket costs. (Medicare)

This can appeal to people who:

- want broad provider freedom under Original Medicare

- want help with deductibles and coinsurance

- want more predictable costs when they use care

- and do not want the network rules common in many Medicare Advantage plans. Medicare’s comparison page between Original Medicare and Medicare Advantage supports those tradeoffs. (Medicare)

So if you want one simple reason why people buy Medigap, it is this:

They want financial help with Medicare-approved hospital and medical bills. (Medicare)

What Medigap does not do for your drug costs

This is a useful reminder, especially because the keyword invites confusion.

Even though Medigap may lower a lot of hospital and doctor-related out-of-pocket costs, it does not usually lower your pharmacy bills in the way Part D does. Medicare says newer Medigap policies do not include prescription drug coverage. (Medicare)

So Medigap may be excellent at helping with:

- hospital coinsurance

- doctor copays or coinsurance

- Part A deductible in many plans

- skilled nursing facility coinsurance in many plans. (Medicare)

But it is not designed to be your modern retail drug plan.

That is what Part D is for. (Medicare)

A simple way to decide what you need

If you are trying to decide what Medigap covers and whether it may fit you, ask yourself these questions.

1. Do I want to keep Original Medicare?

If yes, Medigap may be relevant. Medicare says Medigap works with Original Medicare. (Medicare)

2. Do I want help with deductibles, coinsurance, and copayments?

If yes, Medigap may help because Medicare says that is exactly what it is designed to do. (Medicare)

3. Do I also need prescription drug coverage?

If so, Medigap is usually not enough on its own. Medicare says newer Medigap plans do not include drug coverage so that you may need a separate Part D plan. (Medicare)

4. Am I mainly looking for dental, vision, or hearing benefits?

If so, Medigap may disappoint you, as Medicare generally does not cover those things. (Medicare)

5. Would I rather have one bundled plan?

If so, you may want to compare Medicare Advantage plans instead, because Medicare says many Medicare Advantage plans bundle hospital, medical, drug, and extra benefits. (Medicare)

Those questions usually lead people to the right Medicare path.

Common mistakes people make

One common mistake is assuming Medigap is drug coverage because it is “supplemental.” Medicare says that it is generally wrong for current Medigap plans because plans sold after 2005 do not include prescription drug coverage. (Medicare)

Another mistake is assuming any private Medicare-related plan works the same way. Medicare says Medigap and Medicare Advantage are different products that do different jobs. (Medicare)

Another common mistake is assuming Medigap covers every service Medicare does not fully cover. Medicare says it generally does not cover long-term care, dental, vision, hearing aids, eyeglasses, private-duty nursing, or prescription drugs in newer plans. (Medicare)

Another mistake is forgetting that Part D penalties can happen. Medicare says if you delay Part D too long without creditable drug coverage, you may owe a late enrollment penalty if you join later. (Medicare)

And another mistake is failing to compare plan letters. Medicare says different Medigap letters cover different benefits, so “I have Medigap” does not tell the whole story. (Medicare)

A simple way to remember it

If you want one quick memory tool, use this:

Part A = hospital insurance

Part B = medical insurance

Part D = prescription drug insurance

Medigap = extra private insurance that helps with some Original Medicare cost-sharing (Medicare)

That one four-line summary clears up most of the confusion around this keyword.

Frequently asked questions

What does Medicare Supplemental Insurance cover in general?

Medicare says Medigap helps cover your share of costs for services covered by Original Medicare Part A and Part B, such as deductibles, coinsurance, and copayments. (Medicare)

Does Medigap cover the Part A deductible?

Many plans do. Medicare’s comparison chart shows that several standardized Medigap plans fully cover the Part A deductible, while others cover it partially or not at all. (Medicare)

Does Medigap cover Part B coinsurance?

Yes, many plans help with Part B coinsurance or copayment, but not all plans cover it the same way. Medicare’s chart shows the differences. (Medicare)

Does Medigap cover prescription drugs?

For plans sold after 2005, generally no. Medicare says those Medigap plans do not include prescription drug coverage. (Medicare)

Does Medigap cover dental and vision?

Usually no. Medicare says Medigap generally does not cover dental, vision, hearing aids, or eyeglasses. (Medicare)

Does Medigap cover long-term care?

Usually no. Medicare says Medigap generally does not cover long-term care. (Medicare)

Can I have Medigap and Part D together?

Yes. Medicare says if you want prescription drug coverage and you enroll in Medigap for the first time, you can join a separate Medicare drug plan. (Medicare)

Is Medigap the same as Medicare Advantage?

No. Medicare says Medigap supplements Original Medicare, while Medicare Advantage is another way to get your Medicare coverage. (Medicare)

Final answer

So, what does Medicare Supplemental Insurance cover?

Medicare Supplemental Insurance covers some of the out-of-pocket costs not covered by Original Medicare Parts A and B. Medicare says Medigap may help pay deductibles, copayments, and coinsurance for Medicare-covered hospital and medical services. Depending on the plan letter, it may also help with benefits such as Part A coinsurance and hospital costs, the Part A deductible, skilled nursing facility care coinsurance, hospice cost-sharing, Part B excess charges, and foreign travel emergency costs up to plan limits. (Medicare)

But Medigap does not cover everything. Medicare says it generally does not cover long-term care, dental, vision, hearing aids, eyeglasses, private-duty nursing, or prescription drugs in plans sold after 2005. If you want prescription drug coverage, Medicare says you can join a separate Part D plan. (Medicare)

The clearest plain-English answer is this:

Medigap covers many Medicare cost gaps, but not many Medicare service gaps.

That is the key idea to remember when comparing supplements, drug plans, and broader Medicare coverage options.

OUR CLIENT REVIEWS

CONTACT STEVE TURNER INSURANCE AGENT & BROKER

I’m here to take your calls and emails and answer your questions 7 Days a week from 7:00 a.m. to 8:00 p.m., excluding posted holidays.

Steve Turner is a licensed agent, broker, and a longstanding member of the National Association of Benefits and Insurance Professionals®. Steve holds the prestigious designation of Registered Employee Benefits Consultant®. NABIP® is the preeminent organization for health insurance and employee benefits professionals and works diligently to ensure all Americans have access to high-quality, affordable Healthcare and related services.

Steve Turner is a licensed agent appointed by Florida Blue.

EMAIL ME: 24×7

OFFICE LOCATION

Website: steveturnerinsurancespecialist.com

Email: [email protected]

Phone and Text: +1-813-388-8373

Business Hours:

Monday: 7 am to 8 pm

Tuesday: 7 am to 8 pm

Wednesday: 7 am to 8 pm

Thursday: 7 am to 8 pm

Friday: 7 am to 8 pm

Saturday: 7 am to 8 pm

Sunday: 7 am to 8 pm

SOCIAL FOLLOW + SHARE

LIFE INSURANCE POSTS

INSURANCE OFFERINGS

What Does Medicare Supplemental Insurance Cover?

HEALTH INSURANCE

MEDICARE ADVANTAGE

MEDICARE SUPPLEMENT

PRESCRIPTION DRUGS

LIFE INSURANCE

DISABILITY INSURANCE

DENTAL INSURANCE

GROUP HEALTH INSURANCE

ACCIDENT INSURANCE

LONG TERM CARE INSURANCE

MEDICAID INSURANCE

MEDICARE INSURANCE

MEDICARE PART A INSURANCE

MEDICARE PART B INSURANCE

MEDICARE PART C INSURANCE

MEDICARE PART D INSURANCE

MEDICARE PLAN G INSURANCE

MEDICARE PLAN N INSURANCE

SERVICE AREA

MEDICARE STATEMENT

The Medicare Annual Enrollment Period is October 15th to December 7th. Steve Turner is not connected with or endorsed by the United States Government or the Federal Medicare Program. Some plans may not be available in your area, and any information I provide is limited to those offered. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

There’s no one-size-fits-all answer. Carefully evaluate your health status, anticipated medical needs, prescription drug usage, budget, preferred doctors and hospitals, and tolerance for network rules. During the Medicare Annual Enrollment Period (October 15th to December 7th), thoroughly research the specific plans available in your Florida county using the Medicare Plan Finder on Medicare.gov, compare their costs and benefits, and consider seeking free, personalized counseling from Florida’s SHINE (Serving Health Insurance Needs of Elders) program.