Is Medicare Supplemental Insurance Part B Insurance?

If you are new to Medicare, it is very easy to mix up the names.

You may hear:

Part A,

Part B,

Original Medicare,

Medicare Supplement Insurance,

Medigap,

and Medicare Advantage.

Those terms sound related because they are related. But they are not the same thing.

That is why many people ask this exact question:

Is Medicare Supplemental Insurance Part B insurance?

The short answer is:

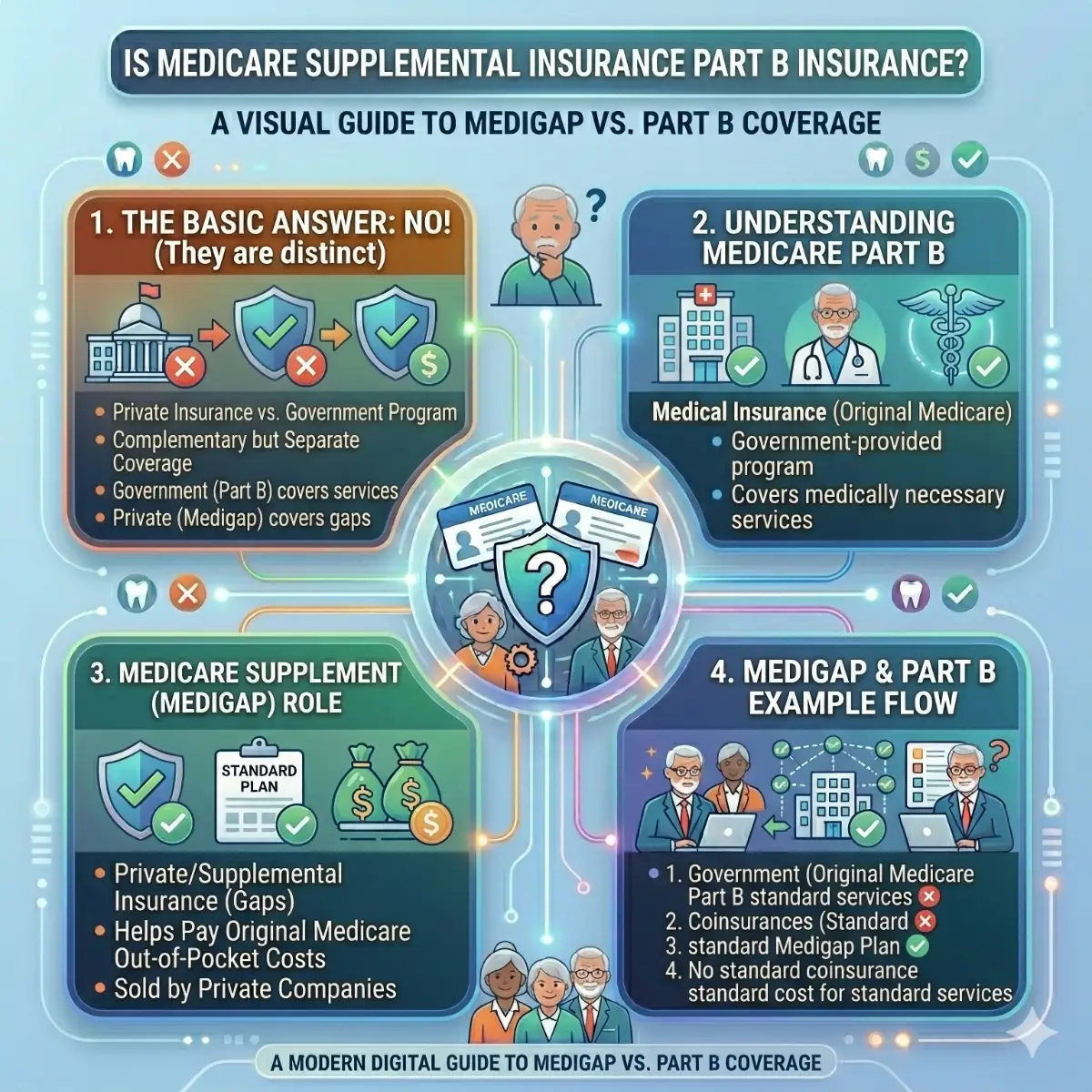

No. Medicare Supplemental Insurance is not Part B insurance. Medicare says Part B is Medical Insurance and one of its official parts. Medicare also says Medicare Supplement Insurance, also called Medigap, is extra insurance you can buy from a private company to help pay your share of out-of-pocket costs in Original Medicare. That means Part B is part of Medicare itself, while Medigap is a separate private insurance that works with Medicare. (Medicare)

That one difference clears up most of the confusion.

Part B is Medicare.

Medigap is not Medicare. It supplements Medicare. (Medicare)

Still, the confusion makes sense.

People get confused because Medigap may help with some costs associated with Part B, such as coinsurance, copayments, and sometimes other cost-sharing. Medicare’s Medigap coverage page says Medigap plans help cover your share of costs for services covered by Original Medicare Part A and Part B. So, Medigap can work closely with Part B, but it is still not the same thing as Part B. (Medicare)

So the best plain-English answer is this:

Medicare Supplemental Insurance is not Part B insurance. Part B is medical insurance inside Medicare. Medigap is extra private insurance that may help pay some of the bills left over after Part A and Part B pay their share. (Medicare)

This guide explains the step-by-step process in easy English.

It will show you:

What Part B is,

What Medigap is,

how they work together,

what Medigap may help pay,

What Medigap does not cover,

And the biggest mistake people make is assuming Medigap is the same as Medicare Part B. Medicare’s official Medicare basics, Medigap, and cost pages support each of these distinctions. (Medicare)

The fastest useful answer

If you want the quickest, most useful answer before reading the full guide, here it is.

No, Medicare Supplemental Insurance is not Part B insurance. Medicare says Part B covers services from doctors and other health care providers, outpatient care, home health care, durable medical equipment, and many preventive services. Medicare also says Medigap is extra private insurance you buy to help pay your share of out-of-pocket costs under Original Medicare, such as copayments, coinsurance, and deductibles. (Medicare)

That means the two are linked, but they are not the same.

Part B is the actual Medicare medical benefit.

Medigap is extra insurance that may help with some of the costs Part B leaves you to pay. (Medicare)

So if someone says, “My supplement helps with doctor bills,” that does not mean the supplement is Part B. It means Part B covers the service first under Medicare rules, and the supplement may then help with some of the remaining cost-sharing. (Medicare)

That is the core idea of the whole article.

First, what Medicare is

Before you can understand the difference between Part B and Medigap, it helps to understand Medicare itself.

Medicare is the federal health insurance program mainly for people age 65 and older and for some younger people with disabilities or certain medical conditions. Medicare’s parts page says there are different parts of Medicare, each covering different types of health care. (Medicare)

The main parts are:

Part A, which is hospital insurance.

Part B, which is medical insurance.

Part D, which is prescription drug coverage.

Part C, also called Medicare Advantage, is another way to get your Medicare coverage through a private health plan approved by Medicare. (Medicare)

Medicare says that Original Medicare includes Part A and Part B. It also says that if you keep Original Medicare, you can join a separate Medicare drug plan for Part D, and you can shop for and buy supplemental coverage that helps pay your out-of-pocket costs. (Medicare)

That last sentence matters a lot.

It shows the order clearly:

First comes Medicare,

then maybe comes supplemental coverage. (Medicare)

So if you want one simple memory line, use this:

Part B is one of Medicare’s official parts. Medigap is an optional extra insurance that sits on top of Original Medicare. (Medicare)

What Part B actually is

Medicare says Part B is Medical Insurance. It helps cover:

services from doctors and other health care providers,

outpatient care,

home health care,

durable medical equipment like wheelchairs, walkers, and hospital beds,

and many preventive services, such as screenings, shots or vaccines, and yearly wellness visits. (Medicare)

That makes Part B one of the most important parts of Medicare in everyday life.

If Part A is more about hospital-type coverage, Part B is the part many people use regularly for:

doctor visits,

specialist appointments,

testing,

outpatient treatment,

and other ongoing medical care. Medicare’s official description makes that clear. (Medicare)

Part B is not a private add-on.

It is not a side policy.

It is not a lettered plan like Plan G or Plan N.

It is a core Medicare benefit. (Medicare)

That is why the answer to the keyword starts with a firm no:

Medicare Supplemental Insurance is not Part B insurance because Part B is already one of Medicare’s official parts. (Medicare)

What Medicare Supplemental Insurance actually is

Now, let’s clearly define the other side.

Medicare says Medicare Supplement Insurance (Medigap) is extra insurance you can buy from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare, like copayments, coinsurance, and deductibles. Medicare also says you generally must have Original Medicare — Part A and Part B — to buy a Medigap policy. (Medicare)

That definition tells you almost everything you need to know.

First, Medigap is extra insurance.

Second, it is sold by a private company.

Third, it is designed to help with your share of costs in Original Medicare.

Fourth, you normally need to have Part A and Part B before you can buy them. (Medicare)

That means Medigap is not “Part B insurance.”

It is better described as:

Cost-sharing help for people who already have Part B and Original Medicare. (Medicare)

So the best simple sentence is this:

Part B is Medicare’s medical insurance. Medigap is private insurance that may help with some of the costs left after Part B and Part A pay for covered services. (Medicare)

Why do people confuse Medigap with Part B

The confusion is understandable.

There are three big reasons people mix them up.

The first reason is the word supplement. When people hear “supplemental insurance,” they assume it must be some official add-on to Medicare. But Medicare says that is not what it is. Medigap is private extra insurance, not a Medicare part. (Medicare)

The second reason is that Medigap helps with costs related to Part B-covered care. Medicare’s Medigap coverage page says Medigap plans help cover your share of costs for services covered by Original Medicare Part A and Part B. So Medigap works closely with Part B, even though it is not Part B. (Medicare)

The third reason is everyday language. A person might say, “My supplement covers my doctor bills,” and someone else might hear that as, “My supplement is my medical insurance.” But Medicare’s structure is different. Part B is the medical insurance. The supplement helps with some of the leftover share. (Medicare)

So if you have ever felt confused by the wording, that is normal.

But Medicare itself draws a very clear line:

Part B is Medicare. Medigap is a separate private supplemental coverage. (Medicare)

How Part B works in real life

To really understand why Medigap is not Part B, it helps to look at how Part B works in the real world.

Let’s say you go to a doctor for outpatient care. Or you need lab work, a scan, medical equipment, or a preventive visit. Medicare says those are the kinds of services Part B helps cover. (Medicare)

Now, Medicare does not mean “free” in every case. Medicare’s cost page says what you pay depends on your coverage and services. It also says there is no yearly limit on what you pay out of pocket in Original Medicare unless you have supplemental coverage or a Medicare Advantage plan. (Medicare)

That means Part B provides the actual medical insurance benefit, but it can still leave you with a share of the bill.

That leftover share is where Medigap may help. (Medicare)

So in real life, Part B is the first layer of medical coverage under Original Medicare. Medigap is not replacing that first layer. It helps after the first layer has already done its job. (Medicare)

How Medigap works in real life

Now look at the Medigap side.

Medicare says Medigap plans help cover your share of costs for services covered by Original Medicare Parts A and B. It also says Medigap helps cover out-of-pocket costs like:

copayments,

coinsurance,

and deductibles. (Medicare)

That means Medigap does not decide whether the doctor visit is covered.

Part B does that.

Medigap does not create the doctor benefit.

Part B does that.

Medigap does not become your medical insurance.

Part B is already your medical insurance. (Medicare)

Medigap’s job is narrower:

It helps with some of the cost-sharing after Medicare approves and processes covered services. (Medicare)

So if someone says, “My supplement paid some of my outpatient bill,” the correct Medicare-language version is:

Part B covered outpatient services, and Medigap may have helped with some of the remaining out-of-pocket costs. (Medicare)

That is the cleanest way to explain the difference.

Medigap only works with Original Medicare

This point makes the answer even clearer.

Medicare says you generally must have Original Medicare — Part A and Part B — to buy a Medigap policy. (Medicare)

That is a huge clue.

If Medigap were actually “Part B insurance,” Medicare would not say you need to have Part B before buying it.

But Medicare does say that.

So the order is:

- You get Part A and Part B.

- Then, if you want extra help with costs, you may buy a Medigap plan. (Medicare)

That means Medigap is not a substitute for Part B. It is not a replacement for Part B. It is not a renamed Part B. It is an optional private supplement for people who already have Part B and Original Medicare. (Medicare)

What Medigap can help pay for that relates to Part B

Now let’s talk about why the confusion feels so believable.

Medicare’s Medigap comparison chart shows that Medigap plans may help with several benefits connected to Part B, including:

Part B coinsurance or copayment,

the Part B deductible in some older plan situations,

and Part B excess charges in some plans. (Medicare)

This is why people often think of Medigap as “art B insurance.” It is not. But it can closely affect what you pay for Part B-covered care. (Medicare)

For example, Medicare’s chart says:

- Part B coinsurance or copayment is covered 100% by some plans,

- partially by Plans K and L,

- and certain notes apply to Plan N. (Medicare)

That means Medigap can make a big difference in what your doctor visits and outpatient care costs after Part B covers the service.

So it is perfectly fair to say:

Medigap can help with Part B costs.

But it is not accurate to say:

Medigap is Part B insurance. (Medicare)

Those are two different ideas.

The Part B deductible issue

This is one of the easiest places to get confused, so it deserves its own section.

Medicare’s cost page says the Part B deductible is $283 in 2026. (Medicare)

Now here is the important Medigap rule: Medicare’s Medigap comparison chart says that Plan C and Plan F aren’t available if you turned 65 on or after January 1, 2020. However, some people who were eligible for Medicare before that date may still be able to get them. Those older plans are the ones people often associate with Part B deductible coverage. (Medicare)

This matters because some people think:

“If I buy Medigap, it must pay the Part B deductible.”

That is not broadly true now.

Medicare’s rules changed for people new to Medicare. So even though Medigap can help with many Part B-related costs, that does not mean it automatically pays every Part B deductible expense for everyone. (Medicare)

Again, that shows Medigap is not Part B itself. It is a private helper plan with specific rules and benefit limits.

The Part B excess charge issue

Another example helps prove the same point.

Medicare’s Medigap plan chart includes Part B excess charge as a separate benefit line. Some Medigap plans cover it, some do not. (Medicare)

That means there are Part B-related costs that may or may not be softened by Medigap, depending on the plan letter.

If Medigap were actually Part B insurance, there would be no reason for Medicare to present it this way. It would all already be inside Part B.

But Medicare separates them:

- Part B is the medical insurance,

- and Medigap is an optional extra insurance that may help with certain Part B-related charges. (Medicare)

That is another reason the keyword answer stays no.

Medigap is bought from a private company

This is another easy way to separate the two in your mind.

Medicare says Part B is Medicare’s medical insurance. Medigap, by contrast, is extra insurance you buy from a private health insurance company. (Medicare)

That means Part B is a federal Medicare benefit.

Medigap is a private insurance product designed to work with that federal benefit. (Medicare)

You can see the difference in how you pay for them, too.

Medicare’s Medigap costs page says you pay a monthly premium to your private insurance company for your Medigap policy. Medicare also says you must still pay your monthly Part B premium, and the premium typically increases each year. (Medicare)

So in real life:

- Part B has its own premium and rules,

- and Medigap has its own separate premium and rules. (Medicare)

That is another strong sign they are not the same insurance.

Medigap plan letters do not make it a Medicare “part.”

Another point confuses people.

Medicare says Medigap policies are standardized and, in most states, are named by letters like Plan G or Plan K. It also says the benefits in each lettered plan are the same, no matter which insurance company sells them. (Medicare)

Because these plans are standardized, some people assume they must be official Medicare parts.

They are not.

The letters are just Medicare’s way of standardizing private supplemental insurance so people can compare plans more easily. They do not turn Plan G or Plan N into something like Part A or Part B. (Medicare)

So, standardized does not mean “part of Medicare.”

It means “private insurance with federally standardized benefits.”

What Medigap does not cover

This is also useful because it shows that Medigap is not the main medical insurance.

Medicare’s Medigap coverage page says Medigap does not cover everything. It generally doesn’t cover:

long-term care,

vision or dental care,

hearing aids,

glasses,

or private-duty nursing. Medicare also notes that Medigap plans sold after 2005 do not include prescription drug coverage. (Medicare)

That means Medigap is not a complete all-purpose medical plan.

It is a narrower supplement built to help with cost-sharing in Original Medicare. (Medicare)

If it were “Part B insurance,” people would expect it to act more like a full primary medical plan. But Medicare’s own definition and exclusions show that it is something different. (Medicare)

Medigap is different from Medicare Advantage, too

This matters because many people mix up all three:

Part B,

Medigap,

and Medicare Advantage.

Medicare says there are two main ways to get your Medicare coverage:

- Original Medicare, which includes Part A and Part B,

- or Medicare Advantage, also known as Part C. Medicare Advantage is an alternative to Original Medicare and usually includes Part A, Part B, and often Part D. Medicare also says Medicare Advantage plans usually have different out-of-pocket costs and usually include a limit on out-of-pocket costs, so you do not need supplemental coverage like Medigap. (Medicare)

This is important because Medigap supplements Original Medicare. It is not used the same way as Medicare Advantage. (Medicare)

So if someone asks whether Medicare Supplemental Insurance is Part B insurance, another helpful correction is:

No. And it is not Medicare Advantage either. It is its own separate category: private supplemental insurance for people with Original Medicare. (Medicare)

A simple real-life example

Here is the easiest way to picture it.

Let’s say Linda has Original Medicare.

She goes to a doctor for outpatient treatment. Medicare says doctor services and outpatient care are generally covered under Part B. (Medicare)

Part B processes claims because it is the medical insurance component of Medicare.

Now Linda also has a Medigap policy.

If her Medigap plan covers some of the Part B coinsurance or copayment, the Medigap policy may help with that leftover amount. Medicare’s Medigap comparison chart shows that many plans do help with Part B coinsurance or copayment. (Medicare)

So what happened?

- Part B was the actual medical insurance.

- Medigap was the extra helper with some of the remaining bills. (Medicare)

That example is the whole answer in real life.

Another example: durable medical equipment

Medicare says Part B helps cover durable medical equipment, such as wheelchairs, walkers, and hospital beds. (Medicare)

If you have a Part B-covered wheelchair expense, Part B is the benefit that covers it under Medicare’s rules.

If you also have Medigap, your plan may help with part of the cost-sharing, depending on its design. (Medicare)

Again:

- Part B creates the medical insurance benefit,

- Medigap helps with some of the leftover share. (Medicare)

That is why Medigap is not Part B insurance.

Another example: preventive services

Medicare says Part B helps cover many preventive services, including screenings, shots or vaccines, and yearly wellness visits. (Medicare)

If you get a Medicare-covered preventive service, Part B is the reason that service is covered under Original Medicare. Medigap does not create that preventive benefit. At most, it may help with certain cost-sharing where the service involves out-of-pocket amounts under Medicare’s rules. (Medicare)

This is another easy way to see the difference:

Part B is the engine. Medigap is the cushion.

Common mistakes people make

One common mistake is saying, “My supplement is my Part B.” That is not how Medicare defines it. Medicare says Part B is Medical Insurance, while Medigap is extra private insurance that helps pay your share of costs in Original Medicare. (Medicare)

Another mistake is thinking Medigap is one of the official Medicare parts. Medicare’s official parts are A, B, C, and D. Medigap is described separately as supplemental private insurance. (Medicare)

Another mistake is assuming Medigap can replace Part B. Medicare says you generally must already have Part A and Part B to buy a Medigap policy. (Medicare)

Another common mistake is assuming Medigap covers everything Original Medicare does not cover. Medicare says it does not cover everything and lists several categories it generally does not cover, like long-term care, vision or dental care, hearing aids, glasses, and private-duty nursing. (Medicare)

And a final mistake is confusing Medigap with Medicare Advantage. Medicare says Medicare Advantage is another way to get Medicare benefits, while Medigap is supplemental insurance for Original Medicare. (Medicare)

A simple way to remember it

If you want a quick memory tool, use this:

Part A = hospital insurance inside Medicare.

Part B = medical insurance inside Medicare.

Medigap = extra private insurance that may help with some leftover Part A and Part B costs. (Medicare)

That one summary solves most of the confusion.

Frequently asked questions

Is Medicare Supplemental Insurance the same as Part B?

No. Medicare says Part B is Medical Insurance within Original Medicare, while Medigap is extra private insurance that helps pay your share of out-of-pocket costs in Original Medicare. (Medicare)

Is Medigap part of Medicare?

Not as one of the official Medicare parts. Medicare’s official parts are A, B, C, and D. Medigap is a separate supplemental insurance sold by private companies. (Medicare)

Can Medigap help with Part B costs?

Yes. Medicare says Medigap helps with your share of costs for services covered by Original Medicare Parts A and B, including copayments, coinsurance, and deductibles, depending on the plan. (Medicare)

Do I need Part B before I can buy Medigap?

Generally yes. Medicare says you must have Original Medicare — Part A and Part B — to buy a Medigap policy. (Medicare)

Is Medigap doctor insurance?

Not in the official Medicare sense. Part B is the medical insurance that covers doctor and outpatient services. Medigap may help with some of the cost-sharing after Part B covers approved services. (Medicare)

Is Medicare Advantage the same as Medigap?

No. Medicare says Medicare Advantage is another way to get Medicare coverage, while Medigap is supplemental insurance for people who keep Original Medicare. (Medicare)

Final answer

So, is Medicare Supplemental Insurance Part B insurance?

No. Medicare Part B is the medical insurance part of Original Medicare. Medicare Supplement Insurance, also called Medigap, is separate private insurance you can buy to help pay your share of out-of-pocket costs in Original Medicare, like copayments, coinsurance, and deductibles. (Medicare)

The clearest plain-English answer is this:

Part B is Medicare. Medigap is extra insurance that may help with some Part B and Part A bills, but it is not Part B itself. (Medicare)

That is the key distinction to keep in mind when comparing Medicare options, doctor coverage, and supplemental insurance.

OUR CLIENT REVIEWS

CONTACT STEVE TURNER INSURANCE AGENT & BROKER

I’m here to take your calls and emails and answer your questions 7 Days a week from 7:00 a.m. to 8:00 p.m., excluding posted holidays.

Steve Turner is a licensed agent, broker, and a longstanding member of the National Association of Benefits and Insurance Professionals®. Steve holds the prestigious designation of Registered Employee Benefits Consultant®. NABIP® is the preeminent organization for health insurance and employee benefits professionals and works diligently to ensure all Americans have access to high-quality, affordable Healthcare and related services.

Steve Turner is a licensed agent appointed by Florida Blue.

EMAIL ME: 24×7

OFFICE LOCATION

Website: steveturnerinsurancespecialist.com

Email: [email protected]

Phone and Text: +1-813-388-8373

Business Hours:

Monday: 7 am to 8 pm

Tuesday: 7 am to 8 pm

Wednesday: 7 am to 8 pm

Thursday: 7 am to 8 pm

Friday: 7 am to 8 pm

Saturday: 7 am to 8 pm

Sunday: 7 am to 8 pm

SOCIAL FOLLOW + SHARE

LIFE INSURANCE POSTS

INSURANCE OFFERINGS

Is Medicare Supplemental Insurance Part B Insurance?

HEALTH INSURANCE

MEDICARE ADVANTAGE

MEDICARE SUPPLEMENT

PRESCRIPTION DRUGS

LIFE INSURANCE

DISABILITY INSURANCE

DENTAL INSURANCE

GROUP HEALTH INSURANCE

ACCIDENT INSURANCE

LONG TERM CARE INSURANCE

MEDICAID INSURANCE

MEDICARE INSURANCE

MEDICARE PART A INSURANCE

MEDICARE PART B INSURANCE

MEDICARE PART C INSURANCE

MEDICARE PART D INSURANCE

MEDICARE PLAN G INSURANCE

MEDICARE PLAN N INSURANCE

SERVICE AREA

MEDICARE STATEMENT

The Medicare Annual Enrollment Period is October 15th to December 7th. Steve Turner is not connected with or endorsed by the United States Government or the Federal Medicare Program. Some plans may not be available in your area, and any information I provide is limited to those offered. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

There’s no one-size-fits-all answer. Carefully evaluate your health status, anticipated medical needs, prescription drug usage, budget, preferred doctors and hospitals, and tolerance for network rules. During the Medicare Annual Enrollment Period (October 15th to December 7th), thoroughly research the specific plans available in your Florida county using the Medicare Plan Finder on Medicare.gov, compare their costs and benefits, and consider seeking free, personalized counseling from Florida’s SHINE (Serving Health Insurance Needs of Elders) program.