Does Medicare Supplemental Insurance Cover Part A Deductible?

If you have Medicare, or you are getting close to age 65, you may hear people talk about Medicare Supplement Insurance, also called Medigap, as a way to lower your out-of-pocket costs.

That leads to a very common question:

Does Medicare Supplemental Insurance cover Part A deductible?

The short answer is:

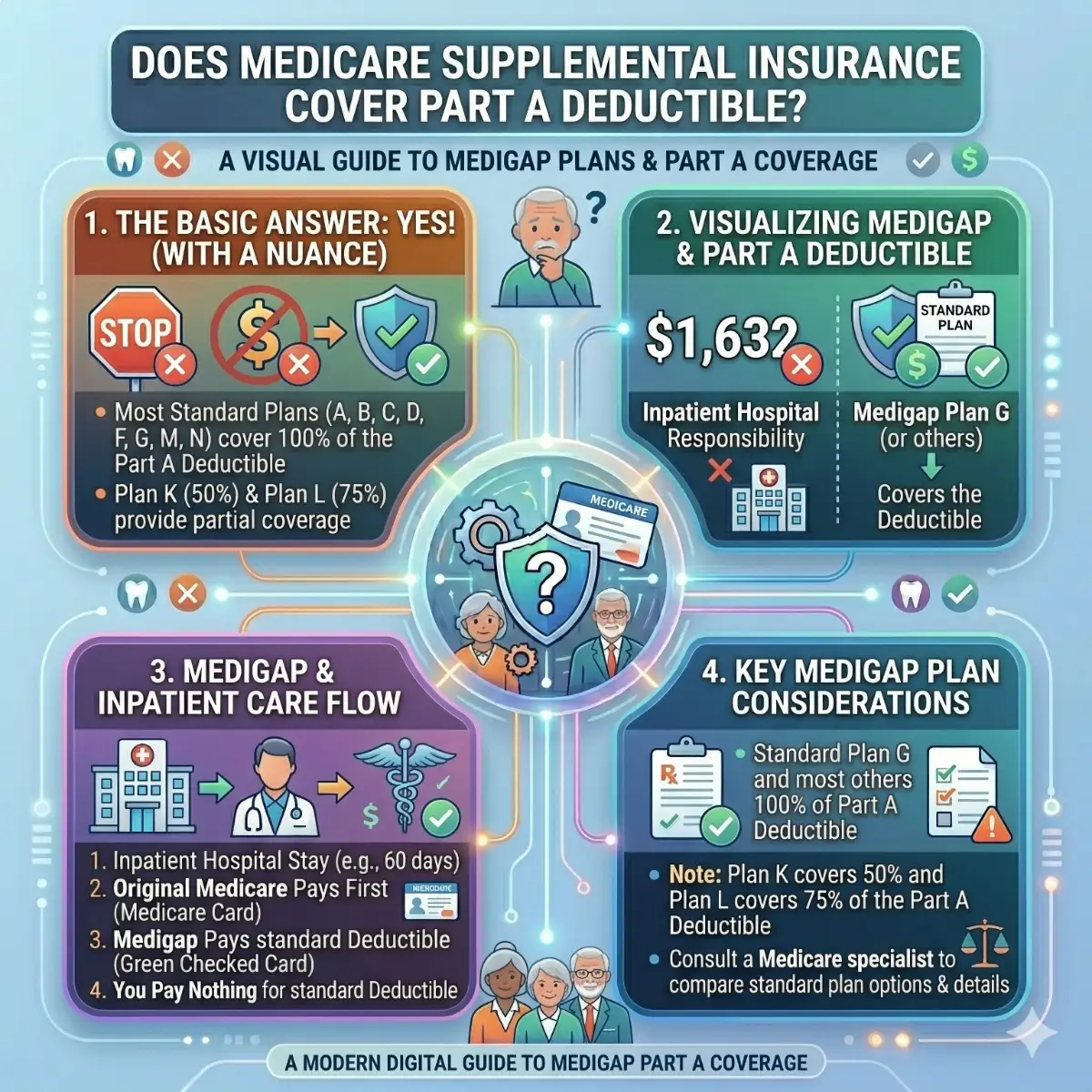

Sometimes yes, but not every Medigap plan covers it. Medicare says Medigap helps pay your share of out-of-pocket costs under Original Medicare, such as copayments, coinsurance, and deductibles. Medicare’s official Medigap comparison chart also shows that some Medigap plans cover the Part A deductible in full, some cover part of it, and one standard plan does not cover it at all. (Medicare)

That means the answer is not just “yes” or “no.” It depends on which Medigap plan letter you have or are thinking about buying. Medicare’s standardized Medigap chart shows that:

- Plan A does not cover the Part A deductible,

- Plans B, C, D, F, and G cover it 100%.

- Plan K covers 50%,

- Plan L covers 75%,

- Plan M covers 50%,

- and Plan N covers it 100%. (Medicare)

This matters because the Medicare Part A deductible is not small. Medicare says the 2026 Part A deductible is $1,736 per inpatient hospital benefit period. Medicare also says there is no limit to the number of benefit periods you can have in a year, so in some situations, a person could owe that deductible more than once in the same year. (Medicare)

So if you are trying to decide whether a Medigap policy is worth it, this is one of the first benefits to consider.

This guide explains all of that in plain English.

It will show you:

- What the Part A deductible is,

- when you owe it,

- How Medigap works,

- which Medigap plans cover the Part A deductible,

- which ones do not,

- what “partial coverage” means,

- How is this different from the Part B deductible?

- and how to decide whether this benefit matters for you. All of the facts below come from official Medicare sources. (Medicare)

The short answer in plain English

If you want the fastest useful answer, here it is:

Yes, many Medicare Supplement plans cover the Medicare Part A deductible, but not all of them. Medicare’s official Medigap comparison chart shows that some plans pay the full Part A deductible, some pay part of it, and one plan does not cover it. (Medicare)

The Part A deductible is the amount you must pay before Original Medicare starts paying for an inpatient hospital stay during a benefit period. Medicare says that in 2026, the amount is $1,736 for each inpatient hospital benefit period. Medicare also explains that a benefit period can restart, meaning the deductible can be reset later. (Medicare)

So if you have a Medigap plan that covers the Part A deductible, that plan may save you a large bill when you are admitted to the hospital as an inpatient. But if you have a plan that does not cover it, or only covers part of it, you may still owe some or all of that deductible yourself. (Medicare)

That is the main takeaway.

Now, let’s slow down and make the whole thing easy to understand.

First, what Medicare Supplement Insurance is

Medicare Supplement Insurance is also called Medigap.

Medicare says Medigap is extra insurance you can buy from a private health insurance company to help pay your share of out-of-pocket costs under Original Medicare, such as copayments, coinsurance, and deductibles. Medicare also says you generally must have Part A and Part B to buy a Medigap policy. (Medicare)

That definition matters a lot.

A Medigap policy does not replace Medicare. It works with Medicare. Medicare pays its share first for covered services under Original Medicare. Then your Medigap policy may help cover the portion you still have to pay, depending on the plan letter you have. Medicare’s Medigap materials are built around exactly that idea. (Medicare)

This is why Medigap is called “supplement” insurance. It supplements Medicare. It does not create a full new health insurance system of its own. It is designed to fill some of the gaps left behind by Original Medicare’s cost-sharing rules. (Medicare)

What Original Medicare Part A is

To understand the Part A deductible, you first need to understand what Part A is.

Medicare says Part A is hospital insurance. It helps cover:

- inpatient hospital stays,

- skilled nursing facility care,

- hospice care,

- and some home health care. (Medicare)

For many people, Part A does not have a monthly premium because they or a spouse paid Medicare taxes long enough while working. Medicare says that in 2026, most people pay $0 for Part A, while some who do not qualify for premium-free Part A pay either $311 or $565 per month, depending on their work history. (Medicare)

But even if your Part A premium is $0, that does not mean hospital care is free.

Medicare says Part A still has a deductible, and this is the deductible most people mean when they ask this keyword question. (Medicare)

What the Part A deductible is

The Part A deductible is the amount you pay before Original Medicare starts to pay for your inpatient hospital care during a benefit period.

Medicare says the 2026 Part A deductible is $1,736 for each inpatient hospital benefit period. Medicare also says there is no limit to the number of benefit periods you can have in a year, which means you may have to pay that deductible more than once in the same year if you have separate hospital stays that begin new benefit periods. (Medicare)

This is one reason the Part A deductible matters so much.

A lot of people hear the word “deductible” and think of something that happens once per year, like the Part B deductible. But Medicare does not structure the Part A deductible that way. The Part A deductible is tied to a benefit period, not simply the calendar year. (Medicare)

That means a Medigap plan that covers the Part A deductible can be very valuable, because it may protect you not just once, but each time that deductible comes up under Medicare’s rules. (Medicare)

What does a benefit period mean

This is one of the most important Medicare words to understand.

Medicare says the Part A deductible applies to each inpatient hospital benefit period. A benefit period is not the same thing as a calendar year. It starts when you are admitted as a hospital inpatient and ends when you have not received inpatient hospital care or skilled nursing facility care for 60 days in a row. (Medicare)

This matters because if you go into the hospital, recover, leave, and then later have another hospital stay after the first benefit period has ended, Medicare can apply a new Part A deductible. (Medicare)

That is why the Part A deductible can become a serious cost. It is not just a one-time hospital fee for life. It can return whenever a new benefit period starts. (Medicare)

So if your Medigap plan covers the Part A deductible, that benefit can protect you every time Medicare applies that deductible under a new benefit period. (Medicare)

Why do people care so much about the Part A deductible

People care about this deductible for one very simple reason:

It is large.

Medicare says the Part A deductible is $1,736 in 2026. That is a meaningful bill for most households. It often arrives at a stressful time, too, because you only face it when you are dealing with a hospital stay or related inpatient care. (Medicare)

For many families, a hospital admission is exactly when they do not want to be thinking about a four-digit deductible bill.

That is why one of the biggest selling points of many Medigap plans is that they cover the Part A deductible, either fully or partly, depending on the plan letter. Medicare’s plan comparison chart makes this very clear. (Medicare)

So when someone asks, “Does Medicare Supplemental Insurance cover Part A deductible?” they are usually asking whether their Medigap plan can protect them from one of the biggest immediate hospital bills Original Medicare can leave behind. The answer is often yes, but the exact answer depends on the plan letter. (Medicare)

Which Medigap plans cover the Part A deductible

Now let’s answer the keyword directly and clearly.

Medicare’s standardized Medigap comparison chart shows the following for the Part A deductible:

- Plan A: does not cover the Part A deductible

- Plan B: covers 100%

- Plan C: covers 100%

- Plan D: covers 100%

- Plan F: covers 100%

- Plan G: covers 100%

- Plan K: covers 50%

- Plan L: covers 75%

- Plan M: covers 50%

- Plan N: covers 100% (Medicare)

That means the answer is not simply “all supplements cover it.”

They do not.

It is more accurate to say:

Most Medigap plans cover the Part A deductible in full, some cover only part of it, and Plan A does not cover it at all. (Medicare)

This is one of the most important differences among Medigap plans, and it is a major reason people carefully compare letter plans rather than looking only at monthly premiums. (Medicare)

Which Medigap plan does not cover the Part A deductible

If you want the simplest “which one does not?” answer, it is this:

Plan A does not cover the Part A deductible. Medicare’s plan comparison chart marks the Part A deductible as not covered for Plan A. (Medicare)

That does not mean Plan A is a bad plan. It simply means it provides the basic core Medigap protections without this particular benefit. If someone buys Plan A, they should expect to pay the full Medicare Part A deductible themselves when it applies. (Medicare)

This is a good example of why the cheapest Medigap premium is not always the cheapest total cost in a bad health year. A lower-premium plan that leaves you exposed to the full Part A deductible may cost less every month, but more when you are admitted to the hospital. (Medicare)

Which Medigap plans cover only part of the Part A deductible

Some Medigap plans provide partial coverage instead of full coverage.

Medicare’s chart says:

- Plan K covers 50% of the Part A deductible,

- Plan L covers 75%,

- Plan M covers 50%. (Medicare)

That means if the Part A deductible is $1,736 in 2026:

- a 50% plan would leave about half of that for you to pay,

- a 75% plan would leave about one-quarter for you to pay,

- A full-coverage plan would leave none of that deductible for you to pay, assuming the service and claim fit Medicare and plan rules. (Medicare)

So when a person says, “My supplement covers the Part A deductible,” it is worth asking one more question:

Does it cover all of it, or only part of it? (Medicare)

That question matters a lot in real life.

Which Medigap plans cover the Part A deductible in full

If your goal is full Part A deductible coverage, Medicare’s chart shows that these plans cover it 100%:

- Plan B

- Plan C

- Plan D

- Plan F

- Plan G

- Plan N (Medicare)

This is one of the reasons Plans G and N get so much attention in the Medigap world. They are among the widely discussed plans that provide strong protection against the Part A deductible while involving different trade-offs elsewhere in the plan design. Medicare’s standardized chart is the best official source for seeing those plan-by-plan differences. (Medicare)

The key point is not that one of these plans is automatically best for every person. The key point is that if the Part A deductible is a major concern for you, several Medigap plan letters fully cover it. (Medicare)

How is this different from the Part B deductible

This is where many people get confused.

The keyword is about the Part A deductible, but many people mix that up with the Part B deductible.

They are not the same thing.

Medicare says the 2026 Part B deductible is $283, paid once each year before Original Medicare begins paying for many Part B services. Medicare’s Medigap materials also explain that, since January 1, 2020, Medigap plans sold to people new to Medicare are not allowed to cover the Part B deductible. That is why Plans C and F are not available to people new to Medicare on or after January 1, 2020. (Medicare)

That means you should not assume:

“If my Medigap covers the Part A deductible, it must also cover the Part B deductible.”

That is often false.

In fact, for people new to Medicare, Medigap generally cannot cover the Part B deductible at all under current federal rules. (Medicare)

So if you are specifically asking about the Part A deductible, the answer is often yes. If you are asking about the Part B deductible, the answer is much more limited. (Medicare)

Why the Part A deductible benefit matters even more than some people think

A lot of people focus on the monthly premium and ignore the benefit details.

That can be a mistake.

Medicare says the Part A deductible is $1,736 in 2026 for each inpatient hospital benefit period. Medicare also says there is no limit to the number of benefit periods you can have in a year. (Medicare)

That means the Part A deductible is not just a one-time issue in a dramatic major surgery year. It can also matter if someone has:

- more than one serious hospital stay,

- a hospital stay followed by another after a new benefit period starts,

- or repeated serious illness over time. (Medicare)

So a Medigap plan that covers this deductible is not just a “nice perk.” For some people, it can be one of the biggest ways the policy lowers the financial shock of inpatient care. (Medicare)

Medigap helps with Medicare-approved costs, not everything

This is another important reminder.

Medicare says Medigap helps cover your share of out-of-pocket costs in Original Medicare. That means it is tied to services covered by Original Medicare. It is not a blank check for every kind of health or care expense. (Medicare)

For example, Medicare says Medigap generally does not cover:

- long-term care,

- vision or dental care,

- hearing aids,

- glasses,

- private-duty nursing,

- And Medigap plans sold after 2005 do not include prescription drug coverage. (Medicare)

This matters because when people hear that Medigap covers the Part A deductible, they sometimes assume it covers “all major hospital and care costs.”

That is too broad.

It covers specific cost-sharing items under Medicare’s benefit structure, and the Part A deductible is one of them. (Medicare)

What if I have a Medicare Advantage plan instead of Medigap?

Then this keyword question changes a lot.

Medicare says Medicare Supplement Insurance works with Original Medicare, and you generally need Part A and Part B to buy a Medigap policy. Medicare also says Medigap is different from Medicare Advantage, because Medicare Advantage is another way to get your Part A and Part B benefits rather than a supplement to Original Medicare. (Medicare)

So if you have a Medicare Advantage plan, you generally do not look at Medigap plan letters to see whether your Part A deductible is covered. Your plan has its own cost structure, copays, deductibles, and yearly out-of-pocket limits. Medicare says Medicare Advantage costs vary by plan and that you must keep paying your Part B premium to stay in the plan. (Medicare)

So the answer to the user’s keyword applies mainly to people who:

- have Original Medicare,

- have Medigap,

- or are shopping for a Medigap plan. (Medicare)

Why do people compare Plan G, Plan N, and Plan M so often on this issue

You will often hear people compare these plan letters because they answer the Part A deductible question differently.

Medicare’s chart shows:

- Plan G covers the Part A deductible fully,

- Plan N covers it fully,

- Plan M covers only 50%. (Medicare)

That means a person deciding between those plans is really choosing among different levels of hospital-deductible protection, among many other differences.

For example:

- Someone who wants stronger protection against inpatient hospital costs may care a lot about whether Plan G or N covers the full Part A deductible. In contrast,

- someone focused on lower monthly premiums may accept a plan with less Part A deductible coverage. (Medicare)

This is exactly why Medicare says Medigap plans with the same letter have the same basic benefits, but different letters offer different benefit structures. (Medicare)

The “same letter, different company” rule

This is one of the most useful Medigap facts for shoppers.

Medicare says policies with the same letter offer the same basic benefits, no matter which insurance company sells them. Price is the only difference between the same-letter plans sold by different insurance companies, aside from service and company factors. (Medicare)

So if you are shopping specifically for Part A deductible coverage:

- The first question is which letter plan covers it the way you want,

- the second question is which company offers that letter plan at the price and customer service level you want. (Medicare)

This helps simplify the shopping process.

First, choose the benefit design.

Then compare companies selling that design. (Medicare)

Why is the best time to think about this early

Medicare says your 6-month Medigap Open Enrollment Period starts the first month you have Part B and are 65 or older. During this period, you can enroll in any Medigap policy, and the insurance company cannot deny you coverage due to pre-existing health problems. Medicare also says that after this period, you may not be able to buy a Medigap policy, or it may cost more. (Medicare)

That means the best time to think hard about whether you want Part A deductible coverage is usually right when your Medigap window opens.

If you delay casually and later decide you really want a plan that fully covers the Part A deductible, it may be more difficult or expensive to get. (Medicare)

This is one of the biggest mistakes people make.

They focus only on current health and premiums, forgetting that future switching may not be as easy as during their first enrollment period. (Medicare)

What if I already have a Medigap plan and want a different one that better covers the Part A deductible?

This is a very common real-life issue.

Maybe you already have Plan A, and you learned it does not cover the Part A deductible. Or maybe you have a partial-coverage plan like K, L, or M, and you now want fuller protection.

Can you switch?

You can apply to switch, but Medicare says after your Medigap Open Enrollment Period, you may not always be able to buy another Medigap policy, or it may cost more. So the answer becomes a switching question, not just a benefit question. (Medicare)

That means if you want stronger Part A deductible protection later, the issue is not only:

“Which plan covers it?”

It is also:

“Can I still switch into that plan on good terms?” (Medicare)

This is another reason why choosing your Medigap letter carefully the first time can matter a lot.

How to read the Part A deductible line on the Medigap chart

The Medicare comparison chart uses symbols, and that can confuse people at first.

The chart explains:

- A full mark means the plan covers 100% of the benefit,

- an X means the plan does not cover the benefit,

- and a % means the plan covers only that percentage, and you are responsible for the rest. (Medicare)

So when you look at the Part A deductible row:

- If your plan shows full coverage, your Medigap plan pays all of that deductible benefit under the plan rules;

- If it shows 50% or 75%, you still owe the remaining portion.

- And if it shows X, you owe the full Medicare Part A deductible yourself. (Medicare)

This makes the keyword answer much easier to understand.

What does Part A deductible coverage not mean

This is worth saying clearly.

If your Medigap plan covers the Part A deductible, that does not mean:

- Every hospital-related cost is automatically free,

- every nursing home cost is covered,

- and every health need tied to a hospital is fully paid. (Medicare)

It means one very specific thing:

The plan helps with the Medicare Part A deductible when that deductible applies under Medicare rules. (Medicare)

That is a big benefit, but it is still one line in a broader Medigap design.

So it is smart to look at the whole plan, not only this one deductible line.

Common mistakes people make

Mistake 1: Assuming all Medigap plans cover the Part A deductible

They do not. Medicare’s chart shows that Plan A does not cover it, and Plans K, L, and M cover only part of it. (Medicare)

Mistake 2: Mixing up the Part A deductible and the Part B deductible

These are different. Medicare says the Part A deductible is $1,736 per benefit period in 2026, while the Part B deductible is $283. Medicare also says people new to Medicare cannot buy Medigap plans that cover the Part B deductible. (Medicare)

Mistake 3: Looking only at the monthly premium

A lower-premium plan may leave you exposed to a large Part A deductible bill if you are hospitalized. (Medicare)

Mistake 4: Thinking the Part A deductible happens only once per year

Medicare says it applies per benefit period, not simply once each calendar year. (Medicare)

Mistake 5: Waiting too long to choose the right Medigap level

Medicare says after your one-time 6-month Medigap Open Enrollment Period, you may not be able to buy the Medigap policy you want, or it may cost more. (Medicare)

A simple way to decide whether this benefit matters to you

Ask yourself these questions:

Would a $1,736 hospital deductible be a strain on my budget if it were incurred unexpectedly? Medicare says that the Part A deductible amount is in 2026. (Medicare)

Do I want stronger protection against hospital costs, even if it means a higher monthly premium? Medigap plans that fully cover the Part A deductible usually provide more hospital-related protection than plans that do not. (Medicare)

Am I comfortable accepting more risk in exchange for lower monthly premiums? If so, a plan with a partial or no Part A deductible may still fit your preferences. (Medicare)

Am I still in my best Medigap buying window? Medicare says your strongest federal buying protection is during your 6-month Medigap Open Enrollment Period. (Medicare)

These questions usually matter more than memorizing every plan letter.

Frequently asked questions

Does Medicare Supplemental Insurance cover the Part A deductible?

Many Medigap plans do, but not all. Medicare’s chart shows that some plans cover it fully, some partially, and Plan A does not cover it. (Medicare)

Which Medigap plans cover the Part A deductible in full?

Medicare’s chart shows that Plans B, C, D, F, G, and N cover 100% of the Part A deductible. (Medicare)

Which Medigap plan does not cover the Part A deductible?

Plan A does not cover the Part A deductible. (Medicare)

Which Medigap plans cover only part of the Part A deductible?

Medicare says Plan K covers 50%, Plan L covers 75%, and Plan M covers 50% of the Part A deductible. (Medicare)

How much is the Medicare Part A deductible in 2026?

Medicare says the Part A deductible is $1,736 for each inpatient hospital benefit period in 2026. (Medicare)

Is the Part A deductible once per year?

Not exactly. Medicare says it is charged per benefit period, and there is no limit to the number of benefit periods you can have in a year. (Medicare)

Does Medigap cover the Part B deductible too?

For people new to Medicare, generally no. Medicare says plans sold to people new to Medicare on or after January 1, 2020, are not allowed to cover the Part B deductible. (Medicare)

Final answer

So, does Medicare Supplemental Insurance cover Part A deductible?

Yes, many Medigap plans do—but not all. Medicare’s official Medigap comparison chart shows that the answer depends on the plan letter. Plans B, C, D, F, G, and N cover the Part A deductible in full. Plans K, L, and M cover only part of it. Plan A does not cover it at all. (Medicare)

That matters because Medicare says the Part A deductible is $1,736 in 2026 for each inpatient hospital benefit period, and you may face it more than once in a year if you have more than one benefit period. (Medicare)

So the clearest plain-English answer is this:

Many Medicare Supplement plans help protect you from the Medicare Part A hospital deductible, but you have to choose the right plan letter if that benefit is important to you. (Medicare)

OUR CLIENT REVIEWS

CONTACT STEVE TURNER INSURANCE AGENT & BROKER

I’m here to take your calls and emails and answer your questions 7 Days a week from 7:00 a.m. to 8:00 p.m., excluding posted holidays.

Steve Turner is a licensed agent, broker, and a longstanding member of the National Association of Benefits and Insurance Professionals®. Steve holds the prestigious designation of Registered Employee Benefits Consultant®. NABIP® is the preeminent organization for health insurance and employee benefits professionals and works diligently to ensure all Americans have access to high-quality, affordable Healthcare and related services.

Steve Turner is a licensed agent appointed by Florida Blue.

EMAIL ME: 24×7

OFFICE LOCATION

Website: steveturnerinsurancespecialist.com

Email: [email protected]

Phone and Text: +1-813-388-8373

Business Hours:

Monday: 7 am to 8 pm

Tuesday: 7 am to 8 pm

Wednesday: 7 am to 8 pm

Thursday: 7 am to 8 pm

Friday: 7 am to 8 pm

Saturday: 7 am to 8 pm

Sunday: 7 am to 8 pm

SOCIAL FOLLOW + SHARE

LIFE INSURANCE POSTS

INSURANCE OFFERINGS

Does Medicare Supplemental Insurance Cover Part A Deductible?

HEALTH INSURANCE

MEDICARE ADVANTAGE

MEDICARE SUPPLEMENT

PRESCRIPTION DRUGS

LIFE INSURANCE

DISABILITY INSURANCE

DENTAL INSURANCE

GROUP HEALTH INSURANCE

ACCIDENT INSURANCE

LONG TERM CARE INSURANCE

MEDICAID INSURANCE

MEDICARE INSURANCE

MEDICARE PART A INSURANCE

MEDICARE PART B INSURANCE

MEDICARE PART C INSURANCE

MEDICARE PART D INSURANCE

MEDICARE PLAN G INSURANCE

MEDICARE PLAN N INSURANCE

SERVICE AREA

MEDICARE STATEMENT

The Medicare Annual Enrollment Period is October 15th to December 7th. Steve Turner is not connected with or endorsed by the United States Government or the Federal Medicare Program. Some plans may not be available in your area, and any information I provide is limited to those offered. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

There’s no one-size-fits-all answer. Carefully evaluate your health status, anticipated medical needs, prescription drug usage, budget, preferred doctors and hospitals, and tolerance for network rules. During the Medicare Annual Enrollment Period (October 15th to December 7th), thoroughly research the specific plans available in your Florida county using the Medicare Plan Finder on Medicare.gov, compare their costs and benefits, and consider seeking free, personalized counseling from Florida’s SHINE (Serving Health Insurance Needs of Elders) program.