Medicare Part B Insurance Apollo Beach FL

Steve Turner Insurance Specialist offers you, your family and your business the complete array of Insurance Services you need to protect and provide for their Medicare Part B Insurance Apollo Beach FL needs.

My goals are to (1) Listen to you tell me about your insurance needs, budget, and the outcome you require, and (2) Educate you on your various options, and (3) Setup the insurance plans you have selected and get your insurance coverage established.

Not sure what what type of insurance is best for your Personal, Family, or Business? No worries! Most of my clients aren’t sure when they first reach out to us. I’ll discuss with you all your insurance options pro’s and con’s so YOU can make the choices that fit your budget.

Tap the “+1.813.388.8373” button to call me now, or the “Book-A-Call” button to pick a time on my calendar for a chat. I look forward to answering your questions and helping you find the right insurance to fit your needs.

OUR RESULTS

LISTENING SKILLS

SCORE = 100

PLAN CHOICES

SCORE = 100

BUDGET FIT

SCORE = 100

Medicare Part B Insurance Apollo Beach FL

As an Apollo Beach, FL-based independent insurance agent with extensive experience, my first duty is to clear up a significant misunderstanding common among Apollo Beach residents. It’s vital to understand that “Medicare Part B Insurance Plans” are not products offered by private companies or agents. Medicare Part B is your fundamental Medical Insurance, provided by the federal government. This isn’t a commercial plan you can select, whether you’re here in Apollo Beach, FL, or any other part of the country.

What we, as expert Apollo Beach-based agents, do provide are the private insurance strategies crafted to address the substantial, and critically, unlimited out-of-pocket expenses tied to your Part B coverage. The main financial vulnerability of Part B for Apollo Beach beneficiaries is the 20% coinsurance, which lacks any annual cap.

Our professional service guides Apollo Beach, FL residents in selecting the optimal solution from two main pathways to shield them from this exposure: Medicare Supplement (Medigap) Plans, which cover the 20% on your behalf, or Medicare Advantage (Part C) Plans, which substitute the 20% coinsurance with a structured system of predictable copayments and a yearly out-of-pocket maximum. When selecting an agent in Apollo Beach, it is crucial to have them detail how both options protect you from the uncapped 20% coinsurance risk of Part B.

An Apollo Beach Expert’s Guide to Covering Your Doctor & Outpatient Costs

As an Apollo Beach-based Medicare specialist with extensive experience, I frequently encounter new clients here in Apollo Beach who ask to “compare Medicare Part B plans.” This is an entirely reasonable question, but it stems from one of the most prevalent misunderstandings in the Medicare framework. The fact is, Medicare Part B is not a plan you select from a menu as you would with other insurance products. Part B is your essential Medical Insurance provided by the federal government.

The truly vital decision Apollo Beach residents must face is how to safeguard their retirement assets right here in Apollo Beach, FL, from the substantial and potentially devastating out-of-pocket expenses of Part B. This is precisely where we, as independent insurance agents, deliver our most crucial service to our Apollo Beach clients. Our role isn’t to “sell” you Part B; it’s to furnish you with the expert counsel and private insurance options specifically engineered to pay for the expenses Part B does not cover.

This guide is intended as a complete resource for Apollo Beach beneficiaries. We will begin by clarifying what your government Part B benefit includes and, more critically, what it costs you. Next, we will break down the private insurance solutions we provide to protect Apollo Beach, FL, residents from those expenses. Lastly, we will equip you with the vital questions you must pose to select the right Apollo Beach-area agent to be your reliable partner in this important choice.

Part 1: Demystifying Medicare Part B – Your Federal Medical Benefit (And Its Costs)

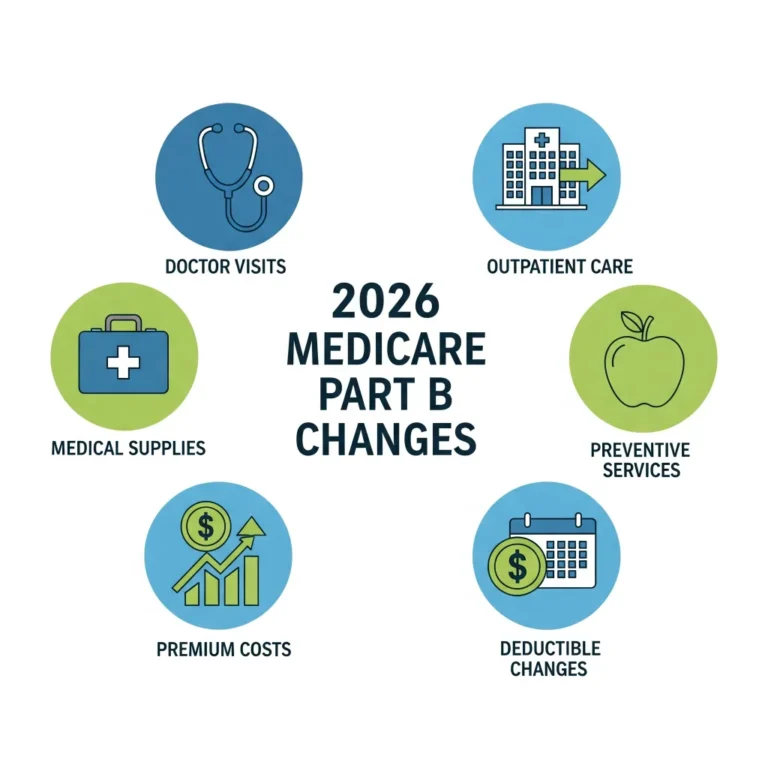

Before selecting a plan to fill the gaps, it’s essential for Apollo Beach beneficiaries to understand the gaps themselves. While Part A is your “Hospital Insurance,” Part B is your “Medical Insurance” for services received outside of an inpatient hospital setting, like at an outpatient clinic in Apollo Beach.

What Part B Covers:

- Doctor’s Visits: This covers your primary care doctor and specialists in the Apollo Beach, FL, area and nationwide.

- Outpatient Medical Care: This encompasses services such as outpatient procedures (perhaps at an Apollo Beach-area surgical center), emergency room care, lab diagnostics, imaging, and chemotherapy.

- Preventive Services: Annual wellness check-ups, flu vaccinations, and a variety of cancer screenings available to all Apollo Beach residents.

- Durable Medical Equipment (DME): Items including walkers, wheelchairs, and oxygen.

- Ambulance Services and various other medical necessities and supplies.

The Significant Out-of-Pocket Costs of Part B (The Problem We Solve):

The expenses for Part B are continuous and, lacking supplementary coverage, entirely unlimited. This creates a significant financial risk for seniors in Apollo Beach, FL. For 2025, the anticipated costs for Apollo Beach residents include:

- The Monthly Part B Premium: All beneficiaries pay a standard monthly premium, determined annually by the government (projected around $178 for 2025). This is usually deducted from your Social Security benefit. Higher-income individuals in Apollo Beach may pay an increased amount due to IRMAA.

- The Annual Part B Deductible: Before Medicare contributes, you must first satisfy an annual deductible for Part B services (projected around $250 for 2025).

- The 20% Coinsurance: This represents the single largest financial vulnerability in Original Medicare for our Apollo Beach clients. Once your annual deductible is met, you are liable for 20% of the Medicare-approved amount for most medical services and outpatient care. The most critical point for Apollo Beach residents to grasp is that there is NO ANNUAL CAP on this 20% coinsurance. A severe illness with costly treatments could potentially leave an Apollo Beach resident liable for tens of thousands of dollars in a single year. Our entire profession is dedicated to protecting Apollo Beach, FL, clients from this uncapped risk.

Part 2: The Solutions We Offer – Private Plans to Manage Your Part B Costs

As an independent agency serving Apollo Beach, FL, we provide the two main solutions Apollo Beach residents utilize to handle the unlimited costs of Medicare Part B. Your decision between these two options in Apollo Beach will fundamentally shape how you get your healthcare during retirement.

A. Medicare Supplement (Medigap) Plans: The “Comprehensive Coverage” Solution

A Medigap plan is a private insurance policy that partners with your Original Medicare. It is designed to pay the costs that Medicare does not.

- How It Works: You present your red, white, and blue Medicare card for all your Part B needs. Medicare pays its 80% share, and your Medigap plan then automatically covers its portion.

- How It Covers Your Part B Costs: This is the primary purpose of a Medigap plan. The most common choice for new Apollo Beach beneficiaries, Plan G, will cover your Part B expenses almost entirely. After you pay the small annual Part B deductible once, Plan G pays the 20% coinsurance for you, 100% of the time. This action completely neutralizes the threat of the uncapped 20% liability. Another popular option for Apollo Beach residents, Plan N, also handles the 20% but has you pay a minor copay (up to $20) for doctor’s appointments.

- The Key Benefit for Apollo Beach Residents: The greatest advantage of this path is the complete freedom of choice. You have the liberty to see any doctor or visit any hospital in the United States, provided they accept Original Medicare. No networks or referrals are required. For Apollo Beach’s “snowbirds” or those who love to travel, this offers unmatched peace of mind. In return for this freedom and predictable costs, you pay a monthly premium to the Medigap provider.

B. Medicare Advantage (Part C) Plans: The “All-in-One” Solution

A Medicare Advantage plan is a private insurance alternative that bundles all your benefits (Part A, Part B, and often Part D) into one single plan.

- How It Works: When you enroll in a Medicare Advantage plan, you use the plan’s ID card (from carriers like Humana, UnitedHealthcare, Aetna) for all your healthcare services. This private plan is responsible for delivering all your Part A and Part B benefits.

- How It Covers Your Part B Costs: Rather than being responsible for the 20% coinsurance, you will pay the plan’s defined, predictable copayments for services. For instance, a typical plan structure in the Apollo Beach area might involve a $10 copay for a primary care visit and a $45 copay for a specialist. You know your cost exposure upfront.

- The Built-in Safety Net: Every single Medicare Advantage plan includes an annual Maximum Out-of-Pocket (MOOP) limit. This is the absolute most you could pay in a calendar year for all your combined Part A and Part B covered services. This MOOP is the plan’s mechanism for protecting Apollo Beach beneficiaries from the limitless 20% coinsurance risk of Original Medicare.

- The Key Benefit for Apollo Beach Residents: The highly competitive Medicare Advantage market in Apollo Beach, FL, results in numerous plans featuring a $0 monthly premium and a robust set of extra benefits. These often include comprehensive dental, vision, and hearing coverage, which Part B does not cover. The trade-off is that you generally must utilize the plan’s local Apollo Beach network of providers.

Part 3: Our Service Process – A Partnership for Your Healthcare Journey

Our objective as Apollo Beach advisors is to transcend being a simple insurance agency; we aim to be your trusted, lifelong partner for everything related to Medicare. Our service process for Apollo Beach residents is structured to be informative, detailed, and solely centered on your best interests.

- The Educational Consultation: We begin with a no-cost, no-obligation consultation for Apollo Beach, FL, residents to educate you on the fundamental choices, particularly how to shield yourself from Part B’s 20% coinsurance.

- The Comprehensive Needs Analysis: We invest the time to listen. We will review your health situation, budget, risk tolerance, and, critically, we will gather a full list of your primary care physicians and specialists here in the Apollo Beach area.

- The Unbiased Market Analysis: As an independent agency, we are appointed with all the major, top-rated carriers in Apollo Beach, FL. We leverage our professional tools to assess every Medigap and Medicare Advantage plan available in your specific Apollo Beach zip code.

- The Clear Recommendation & Enrollment: We will present the top 2-3 options that best suit your unique needs, outlining the pros and cons of each in straightforward terms. Once you, an Apollo Beach resident, have made an informed decision, we manage the entire enrollment process for you.

- Lifelong Support: Our partnership doesn’t conclude at enrollment. We are your Apollo Beach-based advocate. If you have a query about a medical bill or a claim, you call us. Every year, we proactively reach out to our Apollo Beach clients to perform an annual review of your coverage.

Part 4: The Ultimate Vetting Checklist – 10 Questions to Ask Any Medicare Agent

Selecting the right agent in Apollo Beach is as crucial as selecting the right plan. Here are ten vital questions you should pose to any agent you are considering working with in Apollo Beach, FL.

- “Can you clearly explain how a Medigap plan versus a Medicare Advantage plan would handle the costs for an expensive outpatient surgery that costs $50,000?”

- Why it matters: This is a direct challenge to test their grasp of the core Part B risk. The correct answer for an Apollo Beach resident should be: “With Original Medicare alone, you’d owe 20%, or $10,000. With a Medigap Plan G, you’d owe $0 after your small deductible. With a Medicare Advantage plan, you’d pay a fixed copay for the surgery, perhaps $500, and that payment would count toward your annual maximum out-of-pocket.”

- “Are you an independent agent, or are you a ‘captive’ agent who only works for one insurance company?”

- Why it matters: An independent agent serves you and can provide plans from a wide array of companies. A captive agent can only present the products from their specific employer.

- “What is your precise method for confirming that my primary care doctor and all of my specialists are in a Medicare Advantage plan’s network?”

- Why it matters: This assesses their diligence. A top-tier agent serving Apollo Beach will never guess; they will use the insurer’s official provider directory to carefully check every single one of your Apollo Beach-area doctors by name and location.

- “Is there any fee for your services, either now or in the future?”

- Why it matters: The answer must be an unequivocal “no.” Agents are compensated directly by the insurance carriers when they assist a beneficiary with enrollment. You should never pay a fee for an agent’s guidance.

- “How do you assist clients who are worried about the monthly Part B premium? Do you help screen for Medicare Savings Programs?”

- Why it matters: This checks if their knowledge extends beyond just the insurance policies. A well-informed Apollo Beach agent will know about these state-run programs that can help low-income Apollo Beach beneficiaries pay their Part B premium.

- “If I opt for a Medicare Advantage plan, can you describe the difference between an HMO and a PPO, and which might be a better choice for me here in Apollo Beach?”

- Why it matters: This tests their understanding of the most common plan types available here in Apollo Beach, FL. They must be able to articulate the trade-offs between an HMO’s lower costs and a PPO’s greater flexibility.

- “How do you stay current with the annual updates to Medicare plans, especially the frequent changes to provider networks and drug formularies?”

- Why it matters: This probes their professional commitment. An expert will describe their annual carrier certifications and the sophisticated tools they use to monitor changes impacting Apollo Beach residents.

- “What ongoing support do you offer if I have a question about a doctor’s bill or an Explanation of Benefits?”

- Why it matters: This determines their commitment to being your advocate. You want an Apollo Beach-based agent who will be in your corner long after the enrollment is complete.

- “If I select a Medigap plan, how do you help me choose a carrier based on their rate increase history and financial stability?”

- Why it matters: This is an advanced Medigap question. Since benefits are standardized by law, the key long-term factors are price and rate stability. An expert agent will have access to this historical data for plans in Apollo Beach.

- “Why should I work with a local Apollo Beach agent like you instead of just calling the 1-800 number I see on TV?”

- Why it matters: This prompts them to directly state their value. A great agent will emphasize that they offer personalized, local Apollo Beach expertise, a broad range of options, and serve as your personal advocate for life—something a national call center cannot provide.

Part 5: Red Flags vs. Green Lights – Making Your Final Choice of Agent

🚩 Major Red Flags to Run From 🚩

- Cannot clearly articulate the unlimited 20% coinsurance risk of Original Medicare Part B.

- Represents Only One Company: They are a captive agent, not an independent broker focused on the best outcome for Apollo Beach clients.

- Does not meticulously check your doctor network for Medicare Advantage plans. This is a critical step for Apollo Beach residents.

- Pushes one type of plan (e.g., only Medigap or only Advantage) without first performing a thorough needs assessment.

- Uses high-pressure sales tactics or tries to create a false sense of urgency.

✅ Bright Green Lights to Look For ✅

- An Educational, Patient Approach: They prioritize teaching you your options as an Apollo Beach resident.

- Represents a Wide Range of Carriers: They are genuinely independent and can offer you a true, unbiased selection.

- Performs a Detailed, Personalized Needs Analysis, including a meticulous verification of your Apollo Beach-area doctors and your prescriptions.

- Commits to a Lifelong Relationship with ongoing annual reviews and dedicated support for Apollo Beach clients.

- Feels like a trusted, local Apollo Beach advisor.

Your Final Decision

Protecting yourself from the open-ended and potentially catastrophic costs of Medicare Part B is the key to achieving financial security in your retirement healthcare here in Apollo Beach, FL. The choice you make between a Medigap plan and a Medicare Advantage plan will have a significant impact on both your monthly budget and how you access medical care for years to come.

You do not have to make this critical decision alone in Apollo Beach. By partnering with a knowledgeable, independent Apollo Beach agent who is dedicated to your best interests, you gain a trusted advisor who can simplify the complex, provide you with the best options the market has to offer, and serve as your advocate for all the years to come.

Medicare Part B INSURANCE AGENT AND BROKER

As your Insurance Agent and Broker serving you, my goal is to “help you” and ensure, without a shadow of a doubt, that you and your family are secure and protected from risk. As a licensed Medicare Advantage and Medicare Supplement agent, I take the burden off your shoulders by doing a thorough needs analysis and researching the benefits best suited to you and your needs.

I can help you save on severe medical emergencies and find a plan that offers low- to no-cost doctor visits, prescription medication, and extra benefits such as dental, vision and hearing, gym membership, and over-the-counter items. I will show you plans where your doctors are in-network and a side-by-side comparison of your prescription costs with the different plans.

Medicare is constantly changing, and I work tirelessly to stay informed about the latest developments in the market. Not a year goes by without new government regulations, new or modified coverages, and new techniques for controlling benefit costs. To best serve their clients, professionals must understand each type of benefit or program’s provisions, advantages, and limitations to meet economic security.

I am a long-standing National Association of Benefits and Insurance Professionals® (NABIP.ORG) member and hold the prestigious Registered Employee Benefits Consultant® designation (https://nabip.org/professional-development/rebc-designation). I can provide information on your market’s availability and any expected changes.

After you choose your Medicare Insurance plan, I provide ongoing support all year; you won’t have to call an (800) number any longer.

If you have any questions, issues, or concerns about your plan’s benefits, you can contact me via phone, text, or my simple-to-use email contact form using the buttons below.

Steve Turner, your Helpful Licensed Agent and Broker

Medicare Part B Insurance Apollo Beach FL FAQ

OUR CLIENT REVIEWS

CONTACT STEVE TURNER INSURANCE AGENT & BROKER

I’m here to take your calls and emails and answer your questions 7 Days a week from 7:00 a.m. to 8:00 p.m., excluding posted holidays.

Steve Turner is a licensed agent, broker, and a longstanding member of the National Association of Benefits and Insurance Professionals®. Steve holds the prestigious designation of Registered Employee Benefits Consultant®. NABIP® is the preeminent organization for health insurance and employee benefits professionals and works diligently to ensure all Americans have access to high-quality, affordable Healthcare and related services.

Steve Turner is a licensed agent appointed by Florida Blue.

EMAIL ME: 24×7

OFFICE LOCATION

Website: steveturnerinsurancespecialist.com

Email: [email protected]

Phone and Text: +1-813-388-8373

Business Hours:

Monday: 7 am to 8 pm

Tuesday: 7 am to 8 pm

Wednesday: 7 am to 8 pm

Thursday: 7 am to 8 pm

Friday: 7 am to 8 pm

Saturday: 7 am to 8 pm

Sunday: 7 am to 8 pm

SOCIAL FOLLOW + SHARE

SERVICE AREA FACTS APOLLO BEACH FL

Apollo Beach is a census-designated place (CDP) located in Hillsborough County, Florida, United States.

Area code: 813

Elevation: 3 ft (1 m)

Zip Codes: 33572

Population (2026): 31,645 (Projected)

GPS: Latitude: 27.7662 Longitude: -82.4003

An Overview of Apollo Beach, Florida

Apollo Beach is a thriving waterfront community located on the eastern shores of Tampa Bay. Positioned south of Riverview and north of Ruskin, it serves as a premier destination for those seeking a coastal lifestyle without leaving the mainland. The community is defined by its extensive canal system, providing many residents with direct deep-water access to the bay. Originally developed in the 1950s and named after the sun god Apollo, the area has transformed from low-lying wetlands into an affluent residential suburb. Its strategic location along the I-75 corridor makes it an ideal spot for professionals commuting to Tampa or Bradenton, offering a serene, aquatic-focused retreat that remains less than 30 minutes from the urban amenities of downtown Tampa.

Key Statistics and Economic Overview

Apollo Beach’s demographics reflect a wealthy, growing, and well-educated community with a strong emphasis on family life and high-end homeownership.

- Population & Demographics: With a projected population exceeding 31,000, Apollo Beach is experiencing rapid growth, increasing at roughly 3.6% annually. The median age is approximately 41 years, characterizing the area as a dynamic community of established professionals and active families. It is a diverse enclave with a significant veteran presence and a highly educated workforce.

- Economic Profile: The local economy is exceptionally robust, with a median household income of approximately $127,617—significantly higher than the Florida average. The workforce is predominantly white-collar, with a high percentage of residents employed in management, finance, and “knowledge-based” professions. A notable 24% of the workforce telecommutes, reflecting a modern, tech-savvy economic base.

- Housing and Lifestyle: Apollo Beach is defined by an exceptionally high homeownership rate of over 85%. The housing market consists primarily of single-family homes, ranging from mid-century builds to sprawling, multi-million dollar waterfront estates. The lifestyle centers on maritime recreation, including boating, fishing, and paddleboarding, maintained by the community’s intricate network of man-made canals and its proximity to nature preserves.

Top Places for Visitors to Explore in Apollo Beach

While Apollo Beach is cherished for its residential privacy, its unique geography provides immediate access to some of the most famous ecological and recreational sites in the Tampa Bay region.

- Manatee Viewing Center: This award-winning sanctuary is a designated state bird sanctuary and a primary winter refuge for Florida manatees. Visitors can walk the tidal boardwalks to see hundreds of manatees huddling in the warm water discharge from the nearby Big Bend Power Station.

- E.G. Simmons Regional Park: Located just south of the main community, this 469-acre park offers a rustic, natural experience. It features a popular public beach, a boat launch, and one of the best waterfront campgrounds in the county, surrounded by native mangroves and bird-rich wetlands.

- Apollo Beach Nature Preserve: Situated at the northern tip of the community, this 63-acre preserve is a quiet spot for shoreline fishing and sunset viewing. It features a 2-acre sandy beach and a 37-foot observation tower offering panoramic views of the Tampa skyline across the bay.

- Little Manatee River State Park: A short drive away, this park offers visitors a chance to explore the rare ecosystems of the Little Manatee River. It is a premier destination for kayaking, horseback riding, and hiking through sand pine and oxbow wetlands.

- Beer Can Island (Pine Key): A local favorite accessible only by boat, this island is a popular social hub for boaters. It offers a unique “primitive” party atmosphere with sandy shores and clear water, serving as a central spot for weekend social activity.

- Golden Aster Scrub Nature Preserve: Part of the Bullfrog Creek Watershed, this 1,181-acre preserve offers miles of marked trails through sandhill and scrub habitats. It is a critical sanctuary for the rare Florida Golden Aster and home to gopher tortoises and various native birds.

MEDICare Part B INSURANCE POSTS

SERVICE AREA

MEDICARE STATEMENT

The Medicare Annual Enrollment Period is October 15th to December 7th. Steve Turner is not connected with or endorsed by the United States Government or the Federal Medicare Program. Some plans may not be available in your area, and any information I provide is limited to those offered. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

There’s no one-size-fits-all answer. Carefully evaluate your health status, anticipated medical needs, prescription drug usage, budget, preferred doctors and hospitals, and tolerance for network rules. During the Medicare Annual Enrollment Period (October 15th to December 7th), thoroughly research the specific plans available in your Florida county using the Medicare Plan Finder on Medicare.gov, compare their costs and benefits, and consider seeking free, personalized counseling from Florida’s SHINE (Serving Health Insurance Needs of Elders) program.