Life Insurance

Steve Turner Insurance Specialist offers you, your family and your business the complete array of Insurance Services you need to protect and provide for their Life Insurance needs.

My goals are to (1) Listen to you tell me about your insurance needs, budget, and the outcome you require, and (2) Educate you on your various options, and (3) Setup the insurance plans you have selected and get your insurance coverage established.

Not sure what what type of insurance is best for your Personal, Family, or Business? No worries! Most of my clients aren’t sure when they first reach out to us. I’ll discuss with you all your insurance options pro’s and con’s so YOU can make the choices that fit your budget.

Tap the “+1.813.388.8373” button to call me now, or the “Book-A-Call” button to pick a time on my calendar for a chat. I look forward to answering your questions and helping you find the right insurance to fit your needs.

OUR RESULTS

LISTENING SKILLS

SCORE = 100

PLAN CHOICES

SCORE = 100

BUDGET FIT

SCORE = 100

Life Insurance

As an independent insurance broker with extensive experience in Florida, we offer a comprehensive portfolio of Life Insurance Plans tailored to your specific needs and life stage. Our services include providing options for Term Life Insurance (for temporary needs like income replacement and mortgage protection), a variety of Permanent Life Insurance policies (including Whole Life and Universal Life for lifelong protection and legacy planning), and specialized Final Expense Insurance for seniors. Furthermore, we are experts in modern Hybrid Life Insurance plans that include a Long-Term Care (LTC) rider, allowing you to use your death benefit for care expenses while you are living.

When choosing an agent, it is essential to ask if they are an independent broker who represents a wide variety of insurance carriers, not a captive agent tied to a single company. You must inquire about their process for conducting a thorough financial needs analysis to determine the appropriate amount and type of coverage for you. A great agent will educate you on the pros and cons of Term versus Permanent insurance for your unique situation, and will act as a long-term advisor, not just a salesperson. Their services should always be provided at no cost to you.

Life Insurance Plans We Offer: A Florida Expert’s Guide to Protecting Your Family and Securing Your Legacy

Life insurance is one of the most misunderstood and yet most important financial products you will ever purchase. It’s often associated with a single, somber event, but in reality, its purpose is vibrant and full of life. In my many years as an insurance broker helping Florida families, I’ve learned a fundamental truth: life insurance isn’t about you; it’s about the people you love.

It is the ultimate financial safety net, a profound promise you make to your family that they will be protected and provided for, no matter what happens. It’s the policy that ensures your spouse can stay in your family home in Citrus Park without financial strain. It’s the check that guarantees your children’s college education is funded. It’s the final, tax-free gift that allows you to leave a meaningful legacy.

But with so many different types of policies—Term, Whole, Universal, Final Expense—how do you choose the right one? The answer is that life insurance is not a one-size-fits-all product. The “best” plan depends entirely on your stage of life, your financial goals, your budget, and the specific promise you want to make to your loved ones.

This guide is my comprehensive blueprint for you. It’s designed to demystify the world of life insurance, explain the different types of plans we offer, and arm you with the critical questions you must ask to choose not just the right policy, but the right independent agent to be your trusted guide.

Part 1: Understanding the “Why” – The Core Reasons for Life Insurance

Before we look at the different types of plans, it’s essential to understand the “why.” A professional agent will always start by helping you clarify your specific goals.

- Income Replacement: This is the primary reason for most working families. If you were to pass away, this benefit would replace your future income, allowing your family to maintain their standard of living, pay bills, and continue saving for the future.

- Mortgage & Debt Protection: Your largest debt is likely your mortgage. A life insurance policy can provide the funds to pay off the mortgage entirely, ensuring your family can remain in their home without the burden of a monthly payment.

- Final Expense & Burial Costs: The cost of a funeral, burial, and final medical bills can easily exceed $15,000. A smaller life insurance policy can be specifically designed to cover these expenses, so your family doesn’t have to face a financial burden during a time of grief.

- Legacy & Inheritance: You can use life insurance to leave a guaranteed, tax-free inheritance to your children, grandchildren, or a favorite charity, creating a lasting legacy.

- College Funding: A policy can be structured to ensure that funds are available for your children’s or grandchildren’s college education, no matter what.

- Business Succession Planning: For business owners, life insurance is a critical tool for funding buy-sell agreements or providing “key person” insurance to protect the business from the financial loss of a vital partner or employee.

Part 2: A Deeper Dive into the Life Insurance Plans We Offer

As an independent agency, we are not tied to any single carrier. This allows us to search the entire market and offer you the best type of plan from a top-rated company at the most competitive price. Our offerings fall into two main categories.

A. Term Life Insurance: Simple, Affordable Protection “For a Season”

Term life insurance is the simplest and most affordable type of life insurance.

- How It Works: You purchase coverage for a specific period, or “term,” typically 10, 20, or 30 years. If you pass away during that term, your beneficiaries receive the full, tax-free death benefit. If you outlive the term, the policy simply expires, and there is no payout. Think of it as “renting” your insurance coverage—you get the maximum protection for the lowest cost during the years you need it most.

- Best For:

- Young Families: To provide a large amount of income replacement while children are young.

- Mortgage Protection: To match the term of a 30-year mortgage.

- Covering a Specific Period of Need: Ensuring funds are available until your children graduate from college or until you reach retirement.

B. Permanent Life Insurance: Lifelong Protection That Builds Value

Permanent life insurance is designed to last your entire life, as long as you pay the premiums. It also includes a “cash value” component that grows over time. Think of it as “owning” your insurance.

- Whole Life Insurance: This is the most traditional form of permanent insurance. It is defined by its guarantees:

- The premium is fixed and will never increase.

- The death benefit is guaranteed.

- The cash value is guaranteed to grow at a fixed rate.

- Best For: Individuals seeking guarantees, legacy planning, and coverage for final expenses.

- Universal Life (UL) Insurance: UL offers more flexibility than Whole Life. You can often adjust your premium payments and your death benefit amount as your needs change over time. The cash value grows based on current interest rates. It can be a powerful tool for long-term financial planning.

- Final Expense / Burial Insurance: This is a specific type of small whole life policy, typically with a death benefit between $5,000 and $50,000. It is designed specifically to cover funeral costs and other final expenses. These plans often have very simplified underwriting, meaning they are much easier to qualify for, even with some health issues, making them an excellent option for seniors.

C. Hybrid & Specialized Plans: Modern Solutions for Modern Needs

- Life Insurance with a Long-Term Care (LTC) Rider: This is one of the most popular and innovative solutions on the market today. It is a permanent life insurance policy that allows you to accelerate a portion of your death benefit, tax-free, while you are still living to pay for qualified long-term care expenses, such as a nursing home, assisted living, or in-home care. If you never need long-term care, your beneficiaries receive the full death benefit. This powerful hybrid solution protects you from two of the biggest financial risks in retirement.

Part 3: Our Service Process – A Needs-Based, Consultative Approach

Our goal is to build a lifelong relationship with our clients. Our process is designed to be educational, thorough, and completely focused on finding the right solution for you.

- The Confidential Needs Analysis: We start with a deep-dive conversation to understand your complete financial picture, your family’s needs, and your long-term goals. We use a detailed financial needs analysis to calculate the appropriate amount of coverage.

- The Educational Consultation: We explain the fundamental differences between Term and Permanent insurance in simple, clear terms, helping you understand the pros and cons of each for your specific situation.

- The Unbiased Market Analysis: As an independent broker, we have access to quoting software that allows us to search the market and compare the rates from dozens of the nation’s top-rated life insurance carriers.

- Application & Underwriting Support: We guide you through the entire application process. We help you prepare for the medical underwriting (if required) and act as your advocate with the insurance company throughout the process.

- Policy Delivery & Annual Reviews: Once your policy is approved and delivered, we will sit down with you to explain all of its features and benefits. We also offer complimentary annual policy reviews to ensure that as your life changes, your coverage continues to meet your family’s needs.

Part 4: The Ultimate Vetting Checklist – 10 Questions to Ask Any Life Insurance Agent

Choosing the right agent is critical. Here are the ten essential questions you should ask.

1. “Are you an independent agent or a ‘captive’ agent who only works for one insurance company?”

- Why it matters: This is the most important question. A captive agent can only offer you their company’s products. An independent agent works for you and can search the entire market to find the best plan at the most competitive price.

2. “What is your process for conducting a financial needs analysis to determine how much coverage I actually need?”

- Why it matters: This tests their consultative approach. A great agent will have a thorough, documented process for this. A salesperson might just pull a number out of thin air.

3. “Can you explain the pros and cons of Term versus Permanent life insurance for someone in my specific situation?”

- Why it matters: This tests their ability to tailor their advice to you, not just recite a script. They should be able to clearly articulate why one type might be a better fit for your specific goals.

4. “Is there any cost for your services or for running these quotes?”

- Why it matters: The answer should always be “no.” Agents are compensated directly by the insurance companies when a policy is issued. You should never be charged a fee for an agent’s help.

5. “What is your process for helping me navigate the medical underwriting process, and how do you handle clients with pre-existing health conditions?”

- Why it matters: This shows how they will support you through the most complex part of the process. An experienced agent will know which carriers are more favorable to certain health conditions.

6. “How do you help clients decide if they should consider a policy with a Long-Term Care (LTC) rider?”

- Why it matters: This tests their knowledge of modern, hybrid products and their ability to discuss comprehensive retirement planning needs.

7. “How do you stay up-to-date on the offerings and, most importantly, the financial strength ratings of the many different life insurance companies?”

- Why it matters: A life insurance policy is a long-term promise. You want an agent who is diligent about only recommending financially strong, highly-rated companies (e.g., A.M. Best rating of A or higher).

8. “What ongoing service do you provide after the policy is in place?”

- Why it matters: This separates a transactional salesperson from a true relationship-focused agent. A great agent will offer annual reviews and be available for service for the life of the policy.

9. “Who is your ideal client? Do you specialize in working with young families, retirees, or business owners?”

- Why it matters: This helps you understand if their expertise aligns with your needs. An agent who specializes in final expense plans for seniors may not be the best fit for a young family needing large-term policies.

10. “Why should I work with you instead of just buying a policy directly online?”

- Why it matters: This asks them to directly state their value proposition. A great agent will explain that they can provide expert guidance, access to a much wider market of carriers, and advocacy during the underwriting process that an online algorithm cannot.

Part 5: Red Flags vs. Green Lights – Making Your Final Choice of Agent

🚩 Major Red Flags to Run From 🚩

- Pushes One Type of Policy for Everyone: Especially an agent who insists that expensive whole life insurance is the only “good” option for every situation.

- Represents Only One or Two Companies: They are a captive agent, not an independent broker.

- Rushes the Needs Analysis: They are more focused on getting an application than on understanding your needs.

- Uses High-Pressure Sales Tactics: Anyone who tells you that you “must decide today.”

✅ Bright Green Lights to Look For ✅

- Takes an Educational, Consultative Approach: They focus on teaching you your options.

- Is Independent and Represents a Wide Range of Top-Rated Carriers.

- Performs a Detailed, Personalized Financial Needs Analysis as the first step.

- Commits to a Lifelong Relationship with ongoing annual reviews and dedicated support.

- Acts as a trusted financial advisor, not just a salesperson.

Your Final Decision

Life insurance is a fundamental act of love and financial responsibility. It is the promise that your family’s future will be secure, no matter what life throws your way. The “best” plan is not a specific product, but the one that is custom-fit to your unique life, your budget, and the specific promises you want to keep.

By partnering with a knowledgeable, independent agent, you gain more than just a policy; you gain a trusted advisor who can simplify the complex, provide you with the best options the market has to offer, and serve as your advocate for all the years to come. Your focus should be on living a full life with the people you love. Let us help you put the protection in place that gives you the peace of mind to do just that.

Life INSURANCE AGENT AND BROKER

As your Life Insurance Agent and Broker, my goal is to “help you” and ensure, without a shadow of a doubt, that you and your family are secure and protected from risk. As a licensed Life Insurance agent, I take the burden off your shoulders by custom-tailoring Life Insurance packages to fit your needs.

I can help you save on severe medical emergencies and find a Life insurance plan that offers low- to no-cost doctor visits and prescription medication. I will show you plans where your doctors are in-network and a side-by-side comparison of your prescription costs with the different plans.

Life insurance is constantly changing, and I work tirelessly to stay informed about the latest developments in the market.

I am a long-standing National Association of Benefits and Insurance Professionals® (NABIP.ORG) member and hold the prestigious Registered Employee Benefits Consultant® designation (https://nabip.org/professional-development/rebc-designation). I can provide information on your market’s availability and any expected changes.

After you choose your Life Insurance plan, I provide ongoing support all year; you won’t have to call an (800) number any longer.

If you have any questions, issues, or concerns about your plan’s benefits, you can contact me via phone, text, or my simple-to-use email contact form using the buttons below.

Steve Turner, Your Helpful Licensed Agent and Broker

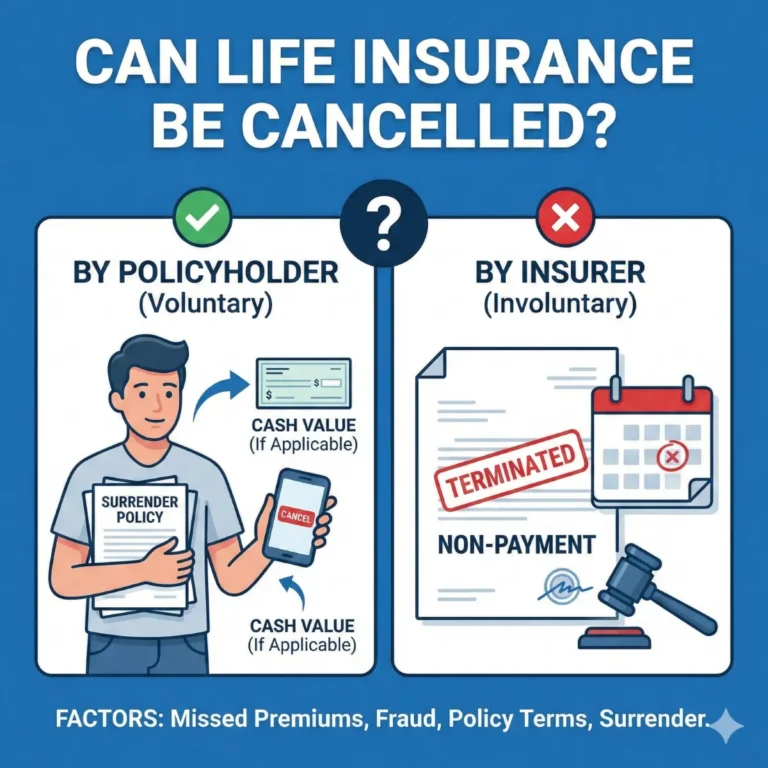

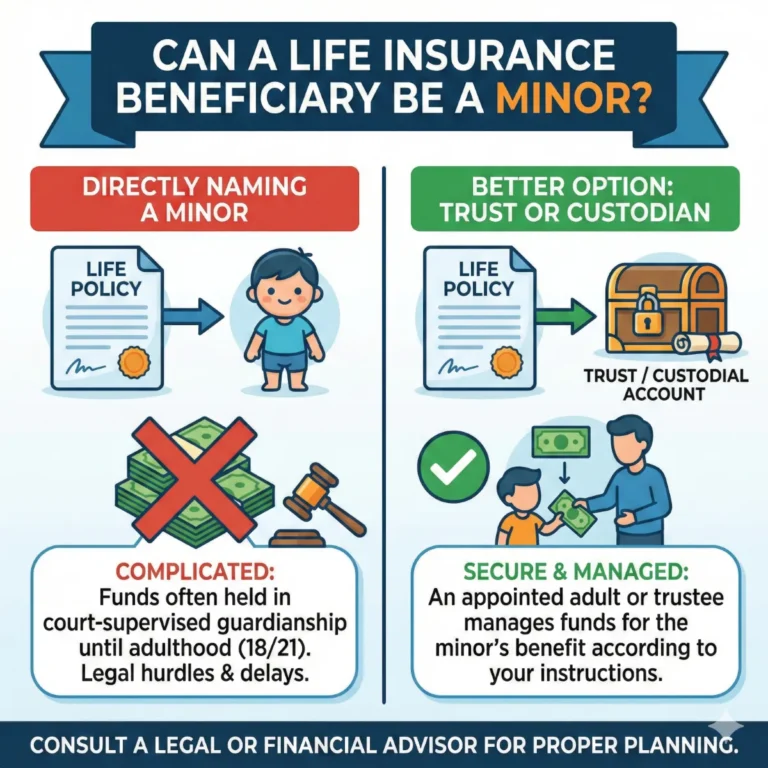

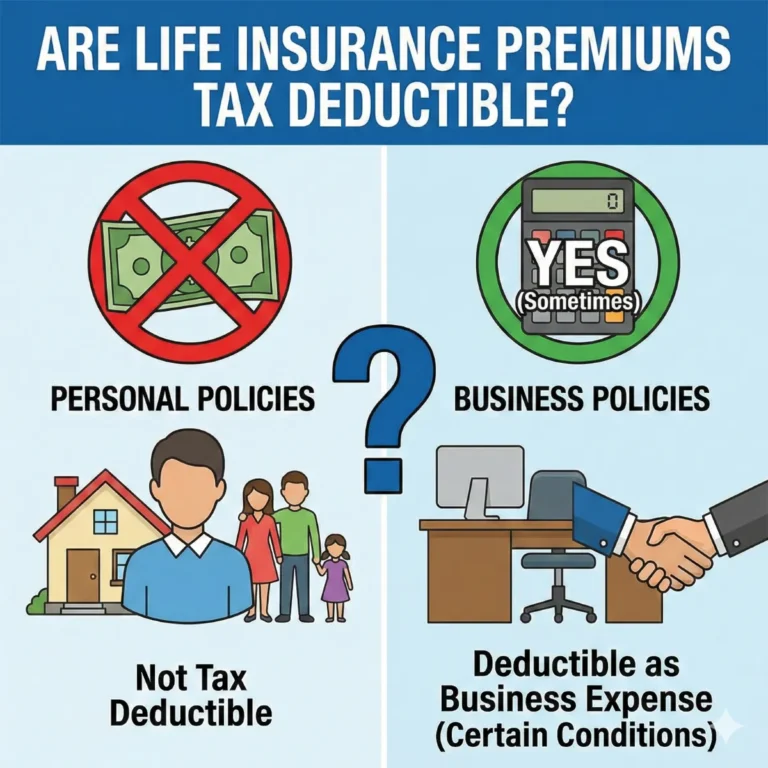

Life Insurance FAQ

OUR CLIENT REVIEWS

CONTACT STEVE TURNER INSURANCE AGENT & BROKER

I’m here to take your calls and emails and answer your questions 7 Days a week from 7:00 a.m. to 8:00 p.m., excluding posted holidays.

Steve Turner is a licensed agent, broker, and a longstanding member of the National Association of Benefits and Insurance Professionals®. Steve holds the prestigious designation of Registered Employee Benefits Consultant®. NABIP® is the preeminent organization for health insurance and employee benefits professionals and works diligently to ensure all Americans have access to high-quality, affordable Healthcare, and related services.

Steve Turner is a licensed agent appointed by Florida Blue.

EMAIL ME: 24×7

OFFICE LOCATION

Website: steveturnerinsurancespecialist.com

Email: [email protected]

Phone and Text: +1-813-388-8373

Business Hours:

Monday: 7 am to 8 pm

Tuesday: 7 am to 8 pm

Wednesday: 7 am to 8 pm

Thursday: 7 am to 8 pm

Friday: 7 am to 8 pm

Saturday: 7 am to 8 pm

Sunday: 7 am to 8 pm

SOCIAL FOLLOW + SHARE

SERVICE AREA FACTS UNITED STATES

The United States: Facts and Top Visitor Sites

The United States of America is a vast and diverse country encompassing a wide array of cultures, landscapes, and iconic landmarks. Here are some key facts and top attractions:

Facts about the USA

The United States is a vast and diverse country, offering a rich tapestry of culture, history, and natural beauty. Here is a comprehensive overview of key statistics and top visitor attractions across the nation.

Key U.S. Statistics and Economic Overview

The United States is a global leader in population, economy, and innovation, attracting people from all over the world.

- Population and Demographics: As of 2025, the U.S. population is projected to be over 343 million people, making it the third most populous country in the world. The population is diverse, with a significant Hispanic and Latino population that accounts for a large portion of the recent growth. The median age is around 39 years, and a growing segment of the population is over 65, reflecting an aging nation.

- Geography: Third largest country by land area, behind Russia and Canada. It stretches across 3.8 million square miles and boasts 4 million miles of roads.

- National Parks: 63 national parks across the nation.

- Government-owned Land: 37% of the land is owned by the government (federal, state, and local).

- Diversity: The US is a diverse country, with a growing non-white population. Non-Hispanic white people currently make up the largest ethnic group, but their share of the population has decreased over time. The Hispanic population has seen the most significant growth, increasing by 23% between 2010 and 2020.

- Languages: While English is the primary language, Spanish is the most common non-English language spoken at home, followed by Chinese and Tagalog.

- Aging Population: Americans are living longer, with the 65 and older population increasing significantly.

- Economy & Key Industries: The U.S. economy is the largest in the world by nominal GDP. Its economic strength is built on several key industries:

- Financial Services: This sector is a global powerhouse, centered in cities like New York, with major hubs for banking, insurance, and investment.

- Technology and Information Technology (IT): The U.S. is a world leader in technology, with major tech hubs in Silicon Valley, Austin, and Seattle, driving innovation in software, hardware, and digital services.

- Healthcare and Social Assistance: As the largest private employment sector in the country, healthcare is a massive industry with a high demand for skilled workers and ongoing innovation.

- Manufacturing: The U.S. manufacturing sector is a backbone of the economy, producing everything from automobiles and aerospace components to medical equipment and consumer goods.

- Work from Home Trends: More Americans are working remotely compared to pre-pandemic times. In 2022, 15% of Americans worked from home, up from 6% in 2019.

Top Places for Visitors to Explore in the USA

The United States offers an incredible variety of destinations, from iconic cities to breathtaking national parks.

- New York City, New York: A global icon, New York City is famous for its vibrant culture, world-class museums, and iconic landmarks. Visitors can explore Times Square, see a Broadway show, visit the Statue of Liberty, and walk through Central Park. The city offers an endless array of dining and shopping experiences.

- The Grand Canyon, Arizona: A breathtaking natural wonder carved by the Colorado River, the Grand Canyon National Park is a must-see. Visitors can take in panoramic views from the South Rim, hike into the canyon, or take a helicopter tour for a unique perspective.

- Las Vegas, Nevada: Known as “The Entertainment Capital of the World,” Las Vegas is famous for its casinos, luxury hotels, and spectacular live shows. The Las Vegas Strip is a bustling boulevard with unique attractions and a vibrant nightlife.

- Orlando, Florida: The “Theme Park Capital of the World,” Orlando is home to some of the world’s most famous attractions, including Walt Disney World Resort and Universal Orlando Resort. It is a top destination for families and anyone seeking a thrilling, magical vacation.

- Washington, D.C.: The nation’s capital is a city of history and monuments. Visitors can explore the National Mall, which connects the Lincoln Memorial, Washington Monument, and the U.S. Capitol. It’s also home to the Smithsonian Institution’s world-class museums.

- Yellowstone National Park, Wyoming: As the first national park in the U.S., Yellowstone National Park is a marvel of geothermal activity and wildlife. It is home to the famous Old Faithful geyser, the Grand Prismatic Spring, and a wide variety of animals, including bison, bears, and wolves.

- San Francisco, California: This iconic city on the West Coast is famous for the Golden Gate Bridge, its historic cable cars, and diverse neighborhoods. Visitors can explore Fisherman’s Wharf, Alcatraz Island, and the beautiful Golden Gate Park.

- Hawaii: The state of Hawaii is an archipelago in the Pacific Ocean known for its stunning natural beauty, volcanic landscapes, and rich Polynesian culture. Visitors can relax on beautiful beaches, hike through lush rainforests, and explore the Hawaii Volcanoes National Park on the Big Island.

- Great Smoky Mountains National Park, North Carolina/Tennessee: The Great Smoky Mountains National Park is the most visited national park in the U.S. and is known for its beautiful mountains, diverse plant and animal life, and rich Appalachian culture.

- New Orleans, Louisiana: This historic city on the Mississippi River is famous for its unique blend of cultures, live music, and vibrant festivals. The French Quarter is a lively neighborhood with historic architecture, delicious Creole cuisine, and jazz clubs.