Can Life Insurance Be Taxed?

As an Insurance Agent and Broker with many years of experience helping Tampa, Saint Petersburg, and Clearwater Area Residents solve their most complex health care and financial challenges, I’ve found that few topics carry more weight—or cause more confusion—than the intersection of life insurance and taxes.

Whether you are walking the pier in St. Pete, enjoying the sunset in Clearwater, or navigating the business district of Downtown Tampa, you want to know that the safety net you’ve built for your family is ironclad. In 2026, the tax landscape has become even more intricate. With the sunset of major federal tax provisions and new IRS interpretations of cash value growth, the question “Can life insurance be taxed?” requires a sophisticated, localized answer.

Can Life Insurance Be Taxed?

In this deep-dive analysis, we will explore every angle of life insurance taxation—from the death benefit to living withdrawals—specifically tailored for residents of the Tampa-Saint Petersburg-Clearwater Metro Area.

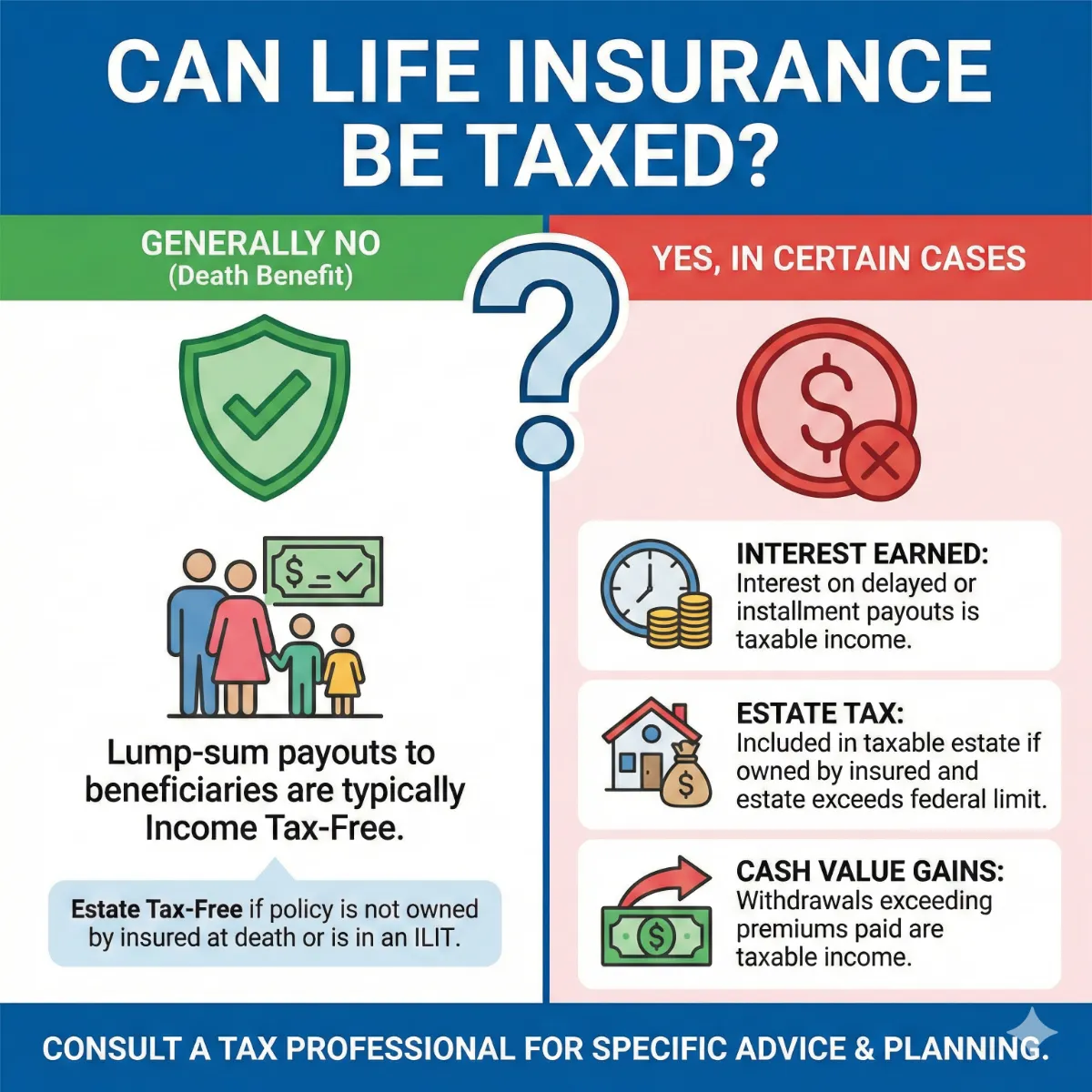

1. The Core Principle: Is the Death Benefit Taxable?

For the vast majority of families in Hillsborough and Pinellas County, the short answer is a welcome one: No. Under Internal Revenue Code Section 101(a), life insurance death benefits are generally received by beneficiaries income tax-free.

This is the primary reason life insurance remains the most efficient vehicle for wealth transfer in the United States. If you leave a $1,000,000 death benefit to your spouse in Tampa, they receive $1,000,000 (provided the policy is structured correctly). They do not have to report it as “income,” and it does not push them into a higher tax bracket.

The “Interest” Exception

However, there is a nuance often overlooked. Many insurance companies offer a “delayed payout” or an “installment” option. If the death benefit remains with the insurance company and earns interest before being paid out to a beneficiary in Clearwater, that interest portion is considered taxable income.

2. The 2026 “Sunset”: Life Insurance and Estate Taxes

While the income tax on a death benefit is rare, the estate tax is a different story. In 2026, we are witnessing a pivotal shift in federal law. The high estate tax exemptions introduced years ago have “sunsetted.”

The New Exemption Limits

As an expert broker who double-checks the data, I am currently advising high-net-worth clients in areas like Belleair and Davis Islands that the federal estate tax exemption has dropped significantly—now sitting at approximately $7 million per individual (or $14 million for married couples).

If your total estate—including your home, investments, and the full face value of your life insurance—exceeds these limits, the IRS can take up to 40% of the excess.

Florida Advantage: One of the greatest “pros” of living in the Tampa-Saint Petersburg-Clearwater Metro Area is that Florida has no state-level estate or inheritance tax. Our neighbors in states like New York or New Jersey often face a double-tax hit, but here in the Sunshine State, we only have to navigate the federal hurdles.

The Solution: The ILIT (Irrevocable Life Insurance Trust)

To prevent the death benefit from being taxed as part of your estate, many local residents utilize an ILIT. By placing the policy inside a trust, you remove it from your “incidents of ownership.” This ensures the payout remains entirely tax-free for your heirs.

3. Taxation of “Living Benefits” and Cash Value

For residents of the Tampa Bay Metro who own permanent policies (Whole Life, Universal Life, or IUL), the “Cash Value” is often viewed as a “private bank.” But tapping into that bank requires a strategic understanding of Cost Basis.

FIFO (First-In, First-Out) Accounting

The IRS allows you to withdraw money from your life insurance policy tax-free up to your basis—the total amount of premiums you have paid into the policy.

- Example: If a resident in St. Petersburg has paid $100,000 in premiums over 20 years and the cash value has grown to $180,000, they can withdraw the first $100,000 without incurring any tax liability.

- The Catch: Any withdrawal over that $100,000 is considered “gain” and is taxed as ordinary income, not at the lower capital gains rate.

Policy Loans: The Tax-Free Secret

This is a major “pro” when comparing different insurance plans available to Tampa, Saint Petersburg, and Clearwater Area Residents. Unlike a withdrawal, a policy loan is generally tax-free, even if the loan amount exceeds your basis.

- Warning: If the policy lapses or is surrendered while a loan is outstanding, the IRS treats the unpaid loan as a distribution, which can trigger a massive, unexpected tax bill.

4. The “Transfer-for-Value” Rule: A Dangerous Trap

This is a technicality that often catches Tampa Bay business owners off guard. Generally, if you sell or transfer a life insurance policy to another person for “valuable consideration” (money or something of value), the death benefit loses its tax-free status.

If you are a business owner in Downtown Tampa looking to sell your company and include a life insurance policy in the deal, you must be extremely careful. Without proper structuring (such as transferring to a partner or a corporation where the insured is an officer), the IRS may tax the death benefit minus the purchase price and subsequent premiums.

5. Modified Endowment Contracts (MEC)

In our metro area, we have many savvy investors who want to “over-fund” their policies to maximize tax-deferred growth. However, if you put too much money into a policy too quickly (exceeding the “7-Pay Test”), the IRS reclassifies it as a Modified Endowment Contract (MEC).

The Consequences of a MEC:

- LIFO Taxation: Withdrawals are taxed as “gains first.”

- 10% Penalty: If you are under age 59½, you pay a 10% penalty on withdrawals, similar to an IRA.

- Irreversibility: Once a policy becomes a MEC, it can never be “undone.”

As your Insurance Agent and Broker, I perform a deep analysis of your premium schedule to ensure your policy stays on the right side of the MEC line.

6. Comparing Insurance Plans for Tax Efficiency

When comparing different insurance plans available to Tampa, Saint Petersburg, and Clearwater Area Residents, we must weigh the tax benefits against the costs.

| Plan Type | Income Tax on Payout | Tax-Deferred Growth? | Loan Accessibility |

| Term Life | No | No (No Cash Value) | No |

| Whole Life | No | Yes | High |

| Universal Life | No | Yes | High |

| Variable Life | No | Yes (Market Linked) | Moderate |

Pros and Cons:

- Term Life Pros: Simplest tax profile. You pay with after-tax dollars, and your family gets a tax-free check.

- Permanent Life Pros: Acts as a “tax-advantaged bucket” for retirement. In the high-cost environment of 2026, having a tax-free source of income in retirement is a major win for Clearwater and St. Pete residents.

7. The “Goodman Triangle” (Gift Tax Risk)

This is a specific “con” that I often fix for new clients in Hillsborough and Pinellas counties. It occurs when three different people occupy the three main roles of a policy:

- The Owner (e.g., The Father)

- The Insured (e.g., The Mother)

- The Beneficiary (e.g., The Child)

If the Mother passes away, the IRS views this as the Father (the Owner) giving a taxable gift to the Child (the Beneficiary). This can trigger a Gift Tax on the entire death benefit.

- The Fix: Ensure the Owner and the Insured are the same person, or the Owner and Beneficiary are the same person.

8. Group Term Life: The $50,000 “Imputed Income” Rule

Many professionals working for major employers in Tampa (like BayCare, Raymond James, or Publix) receive life insurance as a benefit.

- The Rule: The first $50,000 of coverage is tax-free.

- The Tax: If your employer provides more than $50,000 in coverage, the “cost” of that extra coverage (calculated by the IRS) is added to your W-2 as “Imputed Income.” You pay income tax on that amount every year.

9. SEO Long Tail Keywords for Tampa Bay Residents

If you are searching for answers online, you likely use terms like “best life insurance for seniors in Clearwater” or “how to avoid estate tax on life insurance in Tampa.” These are “SEO long tail keywords,” and they are vital for finding accurate, local information.

By searching for “tax-free retirement income with life insurance St. Petersburg,” you are looking for the exact “Living Benefit” strategies we discuss in my office. In 2026, the goal isn’t just to have insurance; it’s to have a tax-efficient financial strategy.

10. Deep Analysis: Why Your Location in Florida Matters

Living in the Tampa-Saint Petersburg-Clearwater Metro Area provides a unique backdrop for these tax discussions.

Local Health Care Costs

We are home to world-class facilities like Tampa General and Moffitt Cancer Center. As we live longer, the “Living Benefits” of life insurance (like Chronic Illness riders) become more valuable.

Expert Note: In Florida, payouts from “Accelerated Death Benefit” riders for terminal or chronic illness are generally received 100% tax-free, allowing you to pay for care without selling off your assets in Clearwater.

Conclusion: Strategy Over Luck

The answer to “Can life insurance be taxed?” is a resounding “sometimes.” While the death benefit is usually safe, the way you own, fund, and access your policy can create significant tax liabilities if not handled with expert care.

For residents of the Tampa-Saint Petersburg-Clearwater Metro Area, the 2026 tax landscape requires a proactive approach. You need a broker who does more than just sell a policy; you need a strategist who performs a deep analysis of your entire estate and double-checks every carrier’s fine print.

Steve Turner Insurance Specialist is here to be your advocate. As an agent and broker with many years of experience helping Tampa-Saint Petersburg-Clearwater Metro Area Residents solve their biggest health care and financial challenges, Steve understands the local market better than anyone. He takes the time to ensure your policy is structured to minimize taxes and maximize the legacy you leave behind.

The best part? Steve’s services are 100% free to you. Like all independent agents and brokers, he is paid by the insurance company that you choose. This means you get expert, unbiased advice and a deep-dive tax analysis at no out-of-pocket cost.

Would you like me to run a customized “Tax-Efficiency Audit” on your current life insurance policies to see if you are at risk for the 2026 estate tax sunset?

Finding Your Trusted Advisor in the Florida Health Insurance Market

We have taken a very detailed look at the Tampa-Saint Petersburg-Clearwater metro area, the Health Insurance Market for 2026. We’ve seen how its clever design offers a modern solution for today’s retirees. We’ve also seen that while the plan’s benefits are stable and reliable, its monthly cost can vary significantly from one insurance company to another. Choosing the right company at the right price is the key to maximizing the value of Health Insurance in 2026.

This is where the guidance of an independent, licensed insurance agent becomes invaluable. A Health Insurance specialist acts as your personal shopper and advocate. They can instantly compare the rates for the same Health Insurance plan options from all the different carriers in your state. They can also provide insight into a company’s history of rate increases, which is a crucial factor in your long-term satisfaction.

It is essential to understand that this expert guidance is provided to you at absolutely no extra cost. The insurance industry is regulated so that the price of a plan is the same whether you buy it through an agent or directly from the company. When you enroll with an agent’s help, the insurance company pays them a commission. This system allows you to get free, unbiased, and professional advice to help you make the best possible choice.

To ensure you get the best value, it is usually best to use a licensed insurance agent, such as Steve Turner at SteveTurnerInsuranceSpecialist.com. Steve Turner is a licensed Agent/Broker contracted with most Insurance Carriers. An expert like Steve can help you navigate the 2026 Health Insurance market, find the most competitively priced Health Insurance plans for you, and ensure you have a Health Insurance plan that provides both financial security and true peace of mind.

OUR CLIENT REVIEWS

CONTACT STEVE TURNER INSURANCE AGENT & BROKER

I’m here to take your calls and emails and answer your questions 7 Days a week from 7:00 a.m. to 8:00 p.m., excluding posted holidays.

Steve Turner is a licensed agent, broker, and a longstanding member of the National Association of Benefits and Insurance Professionals®. Steve holds the prestigious designation of Registered Employee Benefits Consultant®. NABIP® is the preeminent organization for health insurance and employee benefits professionals and works diligently to ensure all Americans have access to high-quality, affordable Healthcare, and related services.

Steve Turner is a licensed agent appointed by Florida Blue.

EMAIL ME: 24×7

OFFICE LOCATION

Website: steveturnerinsurancespecialist.com

Email: [email protected]

Phone and Text: +1-813-388-8373

Business Hours:

Monday: 7 am to 8 pm

Tuesday: 7 am to 8 pm

Wednesday: 7 am to 8 pm

Thursday: 7 am to 8 pm

Friday: 7 am to 8 pm

Saturday: 7 am to 8 pm

Sunday: 7 am to 8 pm

SOCIAL FOLLOW + SHARE

LIFE INSURANCE POSTS

INSURANCE OFFERINGS

Can Life Insurance Be Taxed in Florida?

HEALTH INSURANCE

MEDICARE ADVANTAGE

MEDICARE SUPPLEMENT

PRESCRIPTION DRUGS

LIFE INSURANCE

DISABILITY INSURANCE

DENTAL INSURANCE

GROUP HEALTH INSURANCE

ACCIDENT INSURANCE

LONG TERM CARE INSURANCE

MEDICAID INSURANCE

MEDICARE INSURANCE

MEDICARE PART A INSURANCE

MEDICARE PART B INSURANCE

MEDICARE PART C INSURANCE

MEDICARE PART D INSURANCE

MEDICARE PLAN G INSURANCE

MEDICARE PLAN N INSURANCE

SERVICE AREA

MEDICARE STATEMENT

The Medicare Annual Enrollment Period is October 15th to December 7th. Steve Turner is not connected with or endorsed by the United States Government or the Federal Medicare Program. Some plans may not be available in your area, and any information I provide is limited to those offered. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

There’s no one-size-fits-all answer. Carefully evaluate your health status, anticipated medical needs, prescription drug usage, budget, preferred doctors and hospitals, and tolerance for network rules. During the Medicare Annual Enrollment Period (October 15th to December 7th), thoroughly research the specific plans available in your Florida county using the Medicare Plan Finder on Medicare.gov, compare their costs and benefits, and consider seeking free, personalized counseling from Florida’s SHINE (Serving Health Insurance Needs of Elders) program.