What Type of Insurance Pays Off Home Loan Upon Death?

As a Life Insurance Agent and Broker with many years of experience helping Tampa, Saint Petersburg, and Clearwater Area Residents solve their most complex health care and financial challenges, I know that for most families in the Bay Area, a home is more than just a roof—it’s the cornerstone of their financial legacy.

Whether you’ve recently settled into a bungalow in Old Northeast St. Pete, a waterfront estate in Clearwater Beach, or a new development in Wesley Chapel, your mortgage is likely your largest monthly obligation. The question of what happens to that debt if you are no longer there to pay it is one of the most important financial decisions you will ever make.

In this comprehensive guide, we are going to break down the different types of insurance that can pay off a home loan upon death, comparing the pros and cons of each specifically for Tampa-Saint Petersburg-Clearwater Metro Area Residents. By the end of this analysis, you will know exactly which path secures your family’s future in the Florida sunshine.

What Type of Insurance Pays Off Home Loan Upon Death? Why This Matters in 2026

The real estate market in the Tampa-Saint Petersburg-Clearwater Metro Area has seen significant shifts over the last few years. While home insurance reforms in Florida have begun to stabilize some costs, property values remain high, and mortgage interest rates have hovered around 6%.

For a typical family in Hillsborough or Pinellas County, losing a primary breadwinner doesn’t just mean emotional trauma; it often means a fast track to foreclosure if the remaining spouse cannot maintain the mortgage, property taxes, and the ever-rising cost of homeowners’ insurance.

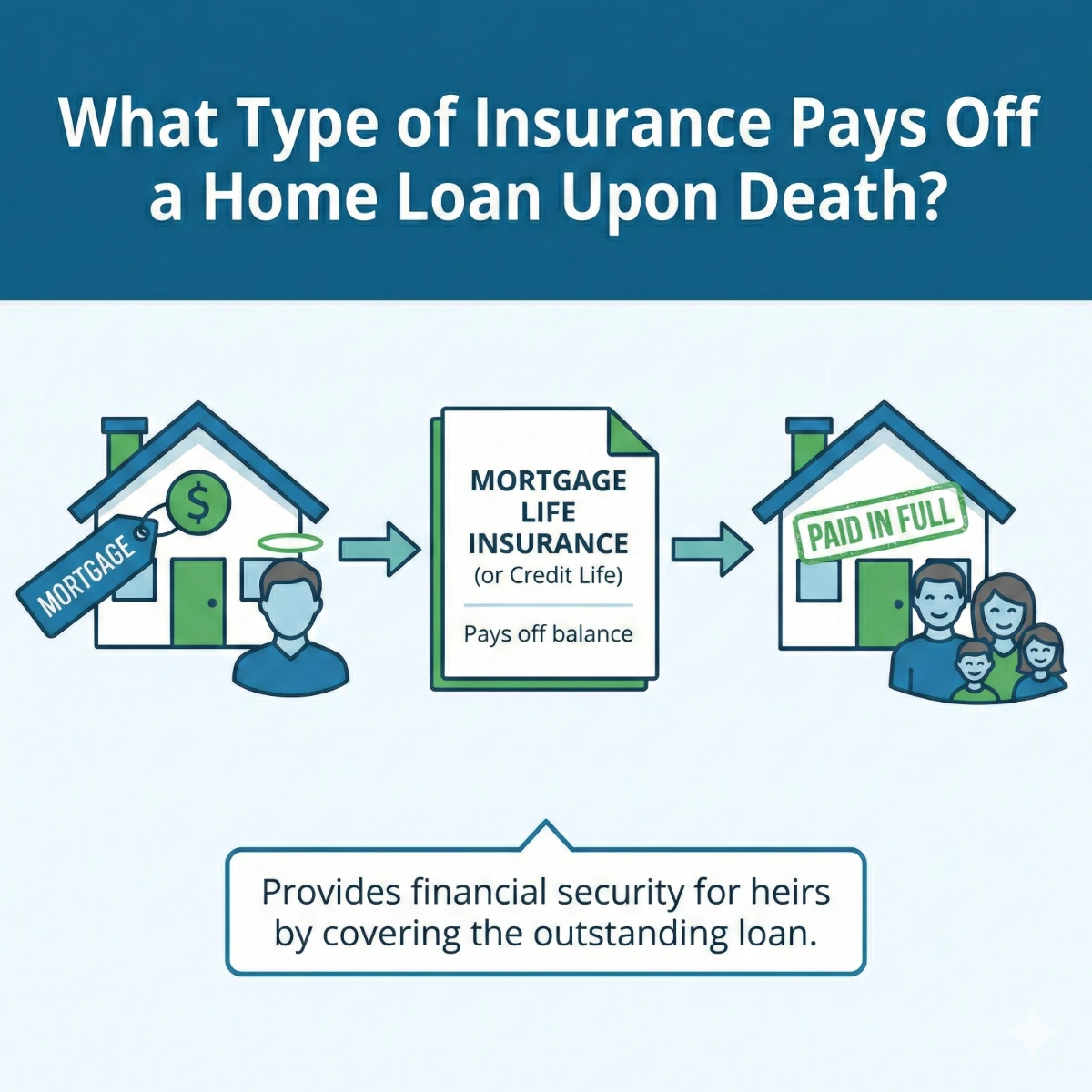

1. Mortgage Protection Insurance (MPI)

Often called “Mortgage Life Insurance,” this specialized product is designed with one singular purpose: to pay off your mortgage balance if you pass away.

How MPI Works for Tampa Bay Homeowners

Unlike a standard life insurance policy, where the money goes to your spouse or children, the beneficiary of an MPI policy is usually the lender. If the insured person dies, the insurance company pays the bank directly, and the house is owned “free and clear.”

The Pros of Mortgage Protection Insurance

- Guaranteed Issue: Many MPI plans in the Tampa, Saint Petersburg, and Clearwater Areas do not require a medical exam. This is a massive benefit for residents with pre-existing conditions (like diabetes or heart disease) who might be denied traditional life insurance.

- Simplification: No guesswork for your family. They don’t have to decide whether to pay off the house or invest the money; the debt simply vanishes.

- Ride-Along Benefits: Many modern MPI policies include “living benefits.” If you have a stroke or are diagnosed with a terminal illness while living in Clearwater, the policy may pay out while you are still alive to help with mortgage payments.

The Cons of Mortgage Protection Insurance

- Decreasing Benefit: Because the policy is tied to your mortgage, the “death benefit” decreases as you pay down your loan. However, your premiums usually stay the same.

- Lack of Flexibility: Your family never touches the money. If they had rather used the funds for funeral costs, property taxes, or moving expenses, they are out of luck.

- Higher Relative Cost: Because there is often no medical underwriting, the insurance company assumes greater risk, reflected in higher premiums for healthy individuals.

2. Term Life Insurance: The Most Popular Alternative

For most Tampa, Saint Petersburg, and Clearwater Area Residents, traditional Term Life Insurance is the gold standard for protecting a mortgage.

How Term Life Insurance Works

You purchase a policy for a set amount (e.g., $500,000) for a set period (e.g., 30 years to match your mortgage). If you pass away during that term, your beneficiaries receive a tax-free lump sum.

Why Term Life Wins on Flexibility

If you live in South Tampa and have a $400,000 mortgage, you might buy a $600,000 term policy. If you pass away, your spouse receives the full $600,000. They can pay off the mortgage or keep making monthly payments and use the lump sum to fund a college education for the kids at USF or UT.

Pricing and Comparison

Typically, a healthy 35-year-old in the Tampa-Saint Petersburg-Clearwater Metro Area will pay significantly less for a term life policy than an MPI policy with the same initial face value.

3. Comparing Insurance Plans: At a Glance

| Feature | Mortgage Protection Insurance (MPI) | Term Life Insurance | Whole Life / Permanent Insurance |

| Beneficiary | The Lender (Bank) | Your Family / Heirs | Your Family / Heirs |

| Benefit Amount | Decreases as mortgage drops | Stays Level | Stays Level (plus cash value) |

| Medical Exam | Often not required | Usually required | Usually required |

| Cost (Premium) | Moderate to High | Lowest | Highest |

| Best For | Residents with health issues | Healthy families on a budget | High-net-worth estate planning |

4. Deep Analysis: The Mathematics of the Payoff

When we look at the financial impact for Tampa, Saint Petersburg, and Clearwater Area Residents, we have to consider the math behind the mortgage.

Suppose you have a $350,000 mortgage at 6.5% interest. Over 30 years, the total cost of that loan is roughly:

$$Total = P \times \frac{r(1+r)^n}{(1+r)^n – 1} \times n$$

Where $P$ is the principal, $r$ is the monthly interest rate, and $n$ is the number of months. In our local market, where property taxes can add another $500–$1,000 to the monthly escrow, having an insurance policy that covers not just the principal, but the “total monthly impact,” is vital.

5. Pricing for Residents in the Tampa Bay Metro (2026 Projections)

The cost of these policies varies based on your age, health, and the specific area you live in (since insurers consider local mortality data).

Sample Monthly Premiums for a $400,000 Policy

(Estimated for a healthy, non-smoking male in Pinellas/Hillsborough County)

| Age | 30-Year Term Life | Mortgage Protection (MPI) |

| 30 | $28 – $35 | $45 – $60 |

| 40 | $45 – $55 | $75 – $95 |

| 50 | $95 – $120 | $160 – $210 |

| 60 | $250+ | $400+ |

Broker’s Tip: In the Tampa-Saint Petersburg-Clearwater Metro Area, we are seeing a trend where residents “ladder” their policies. They might buy a 30-year term to cover the mortgage and a smaller 10-year term to cover the years when their children are still at home. Prices are estimates and subject to change.

6. The “Florida Factor”: Homestead and Probate

Many Tampa, Saint Petersburg, and Clearwater Area Residents ask: “Doesn’t my house just go to my spouse automatically?”

While Florida has strong Homestead Laws that protect your primary residence from many creditors, the mortgage lender is not one of them. The bank has a secured interest. If the mortgage isn’t paid, they can and will foreclose, regardless of Homestead status.

Furthermore, without the liquidity provided by insurance, your family might be forced to sell the home quickly to settle the estate, often losing out on the equity they’ve built during the Tampa Bay real estate boom.

7. SEO Long-Tail Keywords to Consider

If you are researching this online, you’ve likely seen terms like “best life insurance for homeowners Tampa” or “how to pay off mortgage upon death Florida.” These are more than just search terms; they represent the specific needs of our community.

Residents in Clearwater are often looking for policies that address the high costs of coastal living, while residents in St. Petersburg are increasingly focused on protecting the rapid equity gains in downtown corridors.

8. Pros and Cons of “Living Benefits.”

In 2026, many insurance plans available to Tampa, Saint Petersburg, and Clearwater Area Residents now include “Living Benefits” at no extra cost.

- Pro: If you are diagnosed with a chronic illness and can no longer work at your job in Downtown Tampa, you can “accelerate” a portion of your death benefit to pay the mortgage while you are still alive.

- Con: Using these benefits reduces the amount your family receives upon your eventual passing.

9. Common Misconceptions

“I have PMI, so I’m covered.”

This is the most dangerous myth I encounter. Private Mortgage Insurance (PMI) protects the lender if you default on your loan; it does nothing for your family if you die. You are paying for a policy that offers you zero benefit.

“My work life insurance is enough.”

Most employer-provided life insurance in the Tampa-Saint Petersburg-Clearwater Metro Area is only 1x or 2x your salary. For a resident earning $75,000, a $150,000 policy won’t even cover half of the average mortgage in Safety Harbor or St. Pete Beach.

10. Summary of Recommendations

For the vast majority of Tampa, Saint Petersburg, and Clearwater Area Residents, a Term Life Insurance policy with a “Level Death Benefit” is the most cost-effective way to ensure a home loan is paid off upon death. It offers:

- Lower premiums.

- More flexibility for the surviving family.

- The ability to cover more than just the mortgage (like those pesky Florida property taxes).

However, if you have health issues that make qualifying for term insurance difficult, a Mortgage Protection Insurance (MPI) policy is a fantastic “safety net” that ensures your family will never lose their home.

Closing: Expert Guidance for Your Family’s Security

Navigating the world of life and mortgage insurance can feel like trying to find a parking spot at Clearwater Beach on a Saturday afternoon—confusing, crowded, and occasionally frustrating. But it doesn’t have to be.

Steve Turner Insurance Specialist is here to help. As a dedicated agent and broker serving the Tampa-Saint Petersburg-Clearwater Metro Area, Steve has the expertise to shop the entire market for you. He compares every major carrier to find the one that fits your health profile and your budget.

The best part? Steve’s services are 100% free to you. Like all independent agents and brokers, he is paid directly by the insurance company that you choose. This means you get expert, unbiased analysis and local expertise at no out-of-pocket cost.

Would you like me to run a side-by-side quote comparison between a Term Life policy and an MPI policy based on your current mortgage balance?

Finding Your Trusted Advisor in the Florida Health Insurance Market

We have taken a very detailed look at the Tampa-Saint Petersburg-Clearwater metro area, the Health Insurance Market for 2026. We’ve seen how its clever design offers a modern solution for today’s retirees. We’ve also seen that while the plan’s benefits are stable and reliable, its monthly cost can vary significantly from one insurance company to another. Choosing the right company at the right price is the key to maximizing the value of Health Insurance in 2026.

This is where the guidance of an independent, licensed insurance agent becomes invaluable. A Health Insurance specialist acts as your personal shopper and advocate. They can instantly compare the rates for the same Health Insurance plan options from all the different carriers in your state. They can also provide insight into a company’s history of rate increases, which is a crucial factor in your long-term satisfaction.

It is essential to understand that this expert guidance is provided to you at absolutely no extra cost. The insurance industry is regulated so that the price of a plan is the same whether you buy it through an agent or directly from the company. When you enroll with an agent’s help, the insurance company pays them a commission. This system provides free, unbiased, and professional advice to help you make the best possible choice.

To ensure you get the best value, it is usually best to use a licensed insurance agent, such as Steve Turner at SteveTurnerInsuranceSpecialist.com. Steve Turner is a licensed Agent/Broker contracted with most Insurance Carriers. An expert like Steve can help you navigate the 2026 Health Insurance market, find the most competitively priced Health Insurance plans for you, and ensure you have a Health Insurance plan that provides both financial security and true peace of mind.

OUR CLIENT REVIEWS

CONTACT STEVE TURNER INSURANCE AGENT & BROKER

I’m here to take your calls and emails and answer your questions 7 Days a week from 7:00 a.m. to 8:00 p.m., excluding posted holidays.

Steve Turner is a licensed agent, broker, and a longstanding member of the National Association of Benefits and Insurance Professionals®. Steve holds the prestigious designation of Registered Employee Benefits Consultant®. NABIP® is the preeminent organization for health insurance and employee benefits professionals and works diligently to ensure all Americans have access to high-quality, affordable Healthcare, and related services.

Steve Turner is a licensed agent appointed by Florida Blue.

EMAIL ME: 24×7

OFFICE LOCATION

Website: steveturnerinsurancespecialist.com

Email: [email protected]

Phone and Text: +1-813-388-8373

Business Hours:

Monday: 7 am to 8 pm

Tuesday: 7 am to 8 pm

Wednesday: 7 am to 8 pm

Thursday: 7 am to 8 pm

Friday: 7 am to 8 pm

Saturday: 7 am to 8 pm

Sunday: 7 am to 8 pm

SOCIAL FOLLOW + SHARE

LIFE INSURANCE POSTS

INSURANCE OFFERINGS

What Type of Insurance Pays Off Home Loan Upon Death in Florida?

HEALTH INSURANCE

MEDICARE ADVANTAGE

MEDICARE SUPPLEMENT

PRESCRIPTION DRUGS

LIFE INSURANCE

DISABILITY INSURANCE

DENTAL INSURANCE

GROUP HEALTH INSURANCE

ACCIDENT INSURANCE

LONG TERM CARE INSURANCE

MEDICAID INSURANCE

MEDICARE INSURANCE

MEDICARE PART A INSURANCE

MEDICARE PART B INSURANCE

MEDICARE PART C INSURANCE

MEDICARE PART D INSURANCE

MEDICARE PLAN G INSURANCE

MEDICARE PLAN N INSURANCE

SERVICE AREA

MEDICARE STATEMENT

The Medicare Annual Enrollment Period is October 15th to December 7th. Steve Turner is not connected with or endorsed by the United States Government or the Federal Medicare Program. Some plans may not be available in your area, and any information I provide is limited to those offered. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

There’s no one-size-fits-all answer. Carefully evaluate your health status, anticipated medical needs, prescription drug usage, budget, preferred doctors and hospitals, and tolerance for network rules. During the Medicare Annual Enrollment Period (October 15th to December 7th), thoroughly research the specific plans available in your Florida county using the Medicare Plan Finder on Medicare.gov, compare their costs and benefits, and consider seeking free, personalized counseling from Florida’s SHINE (Serving Health Insurance Needs of Elders) program.