Can Life Insurance Payout Go Into A Trust?

Can Life Insurance Payout Go Into A Trust? A Deep Dive for Tampa-Saint Petersburg-Clearwater Metro Area Residents

As an Insurance Agent and Broker with many years of experience helping Tampa-Saint Petersburg-Clearwater Metro Area Residents solve their biggest health care and financial challenges, I’ve found that the conversation often shifts from how much coverage you need to who should actually receive the check.

In the vibrant communities of Tampa, Saint Petersburg, and Clearwater, residents often grapple with a complex question: “Can a life insurance payout go into a trust?” The short answer is yes. In fact, naming a trust as your beneficiary is one of the most sophisticated moves you can make to protect your family from the delays of Florida probate, manage the inheritance for minor children, and potentially shield your assets from the heavy hand of federal estate taxes. In 2026, with the high cost of living and shifting estate tax exemptions, coordinating your life insurance with a trust is no longer just for the “ultra-wealthy” of Belleair or Davis Islands—it is a vital tool for any family in our metro area.

Why Florida Families Use Trusts for Life Insurance

Living in the Tampa-Saint Petersburg-Clearwater Metro Area means navigating Florida’s specific legal landscape. While Florida has no state-level estate tax, our probate courts can be notoriously slow, and our asset protection laws are unique.

1. Avoiding the Florida Probate Slow-Down

In Florida, even “simple” estates can spend months in probate court. If you name your “Estate” as your beneficiary, your life insurance proceeds—intended to provide immediate relief—become tied up in the Pinellas or Hillsborough County court systems.

Expert Note: By naming a trust as the beneficiary, the payout bypasses probate entirely. This ensures that funds are available within weeks, not months, to cover immediate needs like mortgage payments on your home in Safety Harbor or funeral expenses at a local Clearwater chapel.

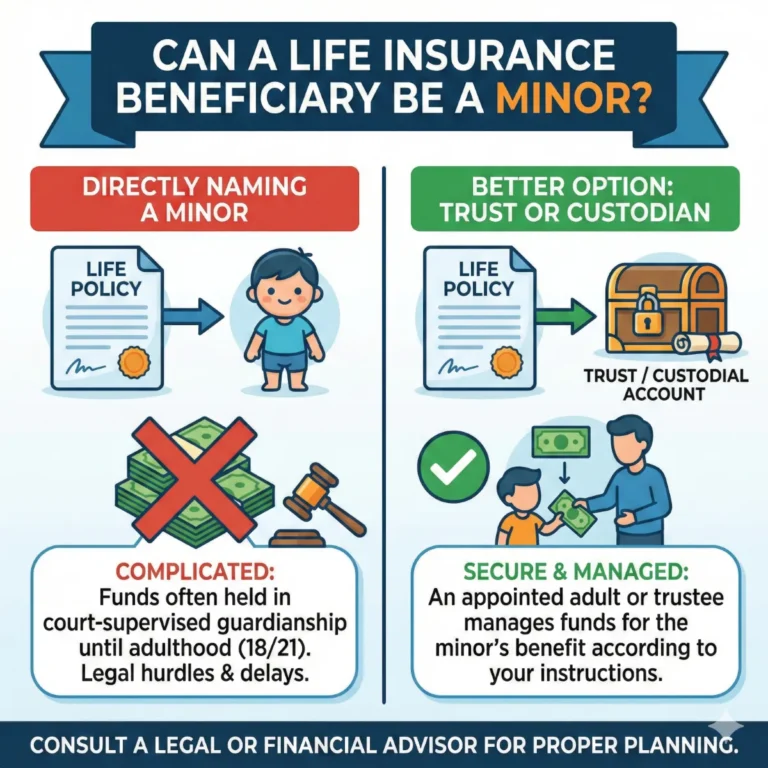

2. Protecting Minor Children in Tampa Bay

If you have children under 18 in Largo or Brandon, you cannot name them directly as beneficiaries. Insurance companies generally will not pay out a $500,000 check to a 10-year-old. Instead, a court-appointed guardian must be involved—a process that is expensive and restrictive.

- The Trust Solution: Naming a trust allows you to appoint a Trustee (a person or bank you trust) to manage the money for the child until they reach a certain age, such as 25 or 30, ensuring the money goes toward a degree from USF or a first home in St. Pete, rather than being spent all at once at 18.

3. Asset and Creditor Protection

Florida is known for its “debtor-friendly” laws, but those protections have limits. Once a life insurance payout hits a beneficiary’s bank account, it is fair game for their creditors.

By putting the payout into a Spendthrift Trust, you can ensure that the money is shielded from the beneficiary’s creditors, lawsuits, or even a messy divorce in Downtown Tampa.

Comparing Insurance Plans: Which Ones Work Best with Trusts?

When comparing insurance plans available to Tampa, Saint Petersburg, and Clearwater Area Residents, it is essential to examine the “engine” powering the trust.

1. Term Life Insurance

- Pros: The most affordable way to fund a trust. It’s perfect for young families in Palm Harbor who need a high level of protection at a low monthly cost.

- Cons: It expires. If you outlive the 20 or 30-year term, the trust remains empty.

- Best For: Families with young children or those protecting a specific debt, like a mortgage.

2. Whole Life Insurance (Permanent)

- Pros: Guaranteed to pay out as long as premiums are paid. It provides a permanent legacy for your heirs in the Tampa Bay Metro.

- Cons: Significantly higher premiums than term insurance.

- Best For: Residents looking for a guaranteed inheritance, estate tax liquidity, or funding for a Special Needs Trust.

3. Universal Life Insurance

- Pros: Offers flexibility in premium payments and death benefits. It can be a middle ground for business owners in Tampa’s Westshore District who need permanent coverage with adjustable costs.

- Cons: Requires active management to ensure the policy remains properly funded as internal costs rise.

| Feature | Term Life | Whole Life | Universal Life |

| Duration | Temporary (e.g., 20 years) | Permanent (Lifetime) | Permanent (Flexible) |

| Cost | Lowest | Highest | Moderate |

| Trust Utility | High for young families | Best for legacy/taxes | Best for flexibility |

The Irrevocable Life Insurance Trust (ILIT) vs. Revocable Trust

As an Insurance Agent and Broker, I spend a lot of time helping residents distinguish between these two “buckets.”

The Revocable Living Trust

Most Tampa-Saint Petersburg-Clearwater Metro Area Residents already have a Revocable Living Trust to avoid probate.

- Pros: You have total control. You can change the beneficiaries or even cancel the trust entirely.

- Cons: For tax purposes, the IRS still considers you the “owner.” The life insurance payout will be counted as part of your taxable estate.

The Irrevocable Life Insurance Trust (ILIT)

For larger estates in Belleair Shore or Snead Island, the ILIT is the gold standard.

- Pros: The trust itself owns the policy. Since you don’t own it, the payout is removed from your taxable estate.

- Cons: Once it’s set up, it’s permanent. You cannot change the terms or take the policy back.

- The “Crummey” Rule: To keep premium payments tax-free, the trust must send “Crummey Notices” to beneficiaries—a technicality that requires expert oversight.

Deep Analysis: The 2026 Estate Tax Landscape

In 2026, the federal estate tax exemption will have shifted. For many families in the Tampa, Saint Petersburg, and Clearwater Area, the risk of hitting the tax threshold is higher than in years past.

Expert Data Check: As of early 2026, the federal estate tax exemption is approximately $15 million per person (or $30 million per couple). However, for those with high-value real estate in St. Pete Beach or successful local businesses, a million-dollar life insurance policy can quickly push an estate toward these limits.

Using an ILIT to hold your life insurance payout ensures that 100% of the proceeds go to your family, rather than 40% to the IRS.

SEO Long Tail Keywords for Tampa Bay Residents

If you are researching this online, you’ve likely come across specific “SEO long tail keywords” like:

- “Best life insurance for trusts in Clearwater, FL”

- “Florida Life Insurance Trust Laws 2026”

- “How to name a trust as beneficiary for life insurance in Tampa.”

- “Avoid Florida probate with a life insurance trust.”

Using these specific terms helps you find specialized advice that understands the local Hillsborough and Pinellas County court systems and the nuances of the Florida market.

Steps to Put Your Life Insurance Payout Into a Trust

As a broker with years of experience, I recommend a structured “3-Step Approach” for Tampa, Saint Petersburg, Clearwater Metro Area Residents.

Step 1: Deep Analysis of Your Goals

Why do you want a trust? Is it to protect minor children in Largo? To keep the money from a spendthrift heir? Or to save on taxes? We must identify the “Why” before we choose the “How.”

Step 2: Selecting the Right Trustee

You need someone responsible. Many residents in St. Petersburg choose a family member, while others prefer a corporate trustee or a local law firm to ensure professional management.

Step 3: Coordinating the Paperwork

This is where many people fail. You must update your Beneficiary Designation Form with the insurance carrier.

- Incorrect: Naming “The Smith Family Trust.”

- Correct: Naming “The Trustee of the Smith Family Trust, dated January 1, 2026.”

Pros and Cons: A Final Summary

The Pros:

- Privacy: Unlike a will, a trust is a private document. Your neighbors in Tampa won’t know the size of your legacy.

- Immediate Liquidity: Funds bypass the probate court delays.

- Legacy Control: You decide how and when the money is spent (e.g., only on college tuition).

- Tax Savings: Potential removal of the payout from your taxable estate.

The Cons:

- Cost of Setup: You will need a Florida estate attorney to draft the trust.

- Complexity: Requires ongoing maintenance, especially with ILITs.

- Loss of Control: With irrevocable trusts, you can’t “change your mind” later.

Frequently Asked Questions from Local Residents

“Can I put my existing policy into a trust?”

Yes, but be careful of the “Three-Year Rule.” If you transfer a policy you already own into a trust and die within three years, the IRS will “claw back” that money into your taxable estate. For my older clients in Clearwater, we often consider buying a new policy within the trust to avoid this risk.

“What happens if I move out of the Tampa Bay area?”

Your trust and insurance policy are generally portable. However, if you move to a state with its own estate tax (like New York or Massachusetts), you will want to have a local professional review your plan.

“Is it expensive to maintain a trust?”

For a standard Revocable Living Trust, there is almost no ongoing cost. For an ILIT, you may have small annual fees if you use a professional trustee, but the tax savings often far outweigh the cost.

Conclusion: Securing Your Family’s “St. Pete” Dream

At the end of the day, the answer to “Can a life insurance payout go into a trust?” is not just “yes”—it’s that for many residents of the Tampa-Saint Petersburg-Clearwater Metro Area, it is the smartest way to ensure your legacy remains intact. Whether you are protecting your toddlers in Clearwater, your business in Tampa, or your legacy in St. Pete, a trust offers a level of control and protection that a simple beneficiary designation cannot.

Navigating the 2026 insurance market and coordinating with legal structures can feel like a full-time job. You shouldn’t have to do it alone.

Steve Turner Insurance Specialist is here to be your advocate and guide. As an expert agent and broker with many years of experience helping Tampa-Saint Petersburg-Clearwater Metro Area Residents solve their biggest health care and financial challenges, Steve understands that insurance is just one piece of your family’s security puzzle. He does the deep analysis, double-checks the data, and ensures your policy is perfectly aligned with your trust’s objectives.

The best part? Steve’s services are 100% free to you. Like all independent agents and brokers, he is compensated by the insurance company that you choose. This means you receive his years of expertise, his localized research, and his dedicated support without ever seeing a bill from his office.

Would you like me to provide a side-by-side premium comparison for a Term vs. Whole Life policy specifically structured to fund your family trust today?

Finding Your Trusted Advisor in the Florida Health Insurance Market

We have taken a very detailed look at the Tampa-Saint Petersburg-Clearwater metro area, the Health Insurance Market for 2026. We’ve seen how its clever design offers a modern solution for today’s retirees. We’ve also seen that while the plan’s benefits are stable and reliable, its monthly cost can vary significantly from one insurance company to another. Choosing the right company at the right price is the key to maximizing the value of Health Insurance in 2026.

This is where the guidance of an independent, licensed insurance agent becomes invaluable. A Health Insurance specialist acts as your personal shopper and advocate. They can instantly compare the rates for the same Health Insurance plan options from all the different carriers in your state. They can also provide insight into a company’s history of rate increases, which is a crucial factor in your long-term satisfaction.

It is essential to understand that this expert guidance is provided to you at absolutely no extra cost. The insurance industry is regulated so that the price of a plan is the same whether you buy it through an agent or directly from the company. When you enroll with an agent’s help, the insurance company pays them a commission. This system allows you to get free, unbiased, and professional advice to help you make the best possible choice.

To ensure you get the best value, it is usually best to use a licensed insurance agent, such as Steve Turner at SteveTurnerInsuranceSpecialist.com. Steve Turner is a licensed Agent/Broker contracted with most Insurance Carriers. An expert like Steve can help you navigate the 2026 Health Insurance market, find the most competitively priced Health Insurance plans for you, and ensure you have a Health Insurance plan that provides both financial security and true peace of mind.

OUR CLIENT REVIEWS

CONTACT STEVE TURNER INSURANCE AGENT & BROKER

I’m here to take your calls and emails and answer your questions 7 Days a week from 7:00 a.m. to 8:00 p.m., excluding posted holidays.

Steve Turner is a licensed agent, broker, and a longstanding member of the National Association of Benefits and Insurance Professionals®. Steve holds the prestigious designation of Registered Employee Benefits Consultant®. NABIP® is the preeminent organization for health insurance and employee benefits professionals and works diligently to ensure all Americans have access to high-quality, affordable Healthcare, and related services.

Steve Turner is a licensed agent appointed by Florida Blue.

EMAIL ME: 24×7

OFFICE LOCATION

Website: steveturnerinsurancespecialist.com

Email: [email protected]

Phone and Text: +1-813-388-8373

Business Hours:

Monday: 7 am to 8 pm

Tuesday: 7 am to 8 pm

Wednesday: 7 am to 8 pm

Thursday: 7 am to 8 pm

Friday: 7 am to 8 pm

Saturday: 7 am to 8 pm

Sunday: 7 am to 8 pm

SOCIAL FOLLOW + SHARE

LIFE INSURANCE POSTS

INSURANCE OFFERINGS

Can Life Insurance Payout Go Into A Trust?

HEALTH INSURANCE

MEDICARE ADVANTAGE

MEDICARE SUPPLEMENT

PRESCRIPTION DRUGS

LIFE INSURANCE

DISABILITY INSURANCE

DENTAL INSURANCE

GROUP HEALTH INSURANCE

ACCIDENT INSURANCE

LONG TERM CARE INSURANCE

MEDICAID INSURANCE

MEDICARE INSURANCE

MEDICARE PART A INSURANCE

MEDICARE PART B INSURANCE

MEDICARE PART C INSURANCE

MEDICARE PART D INSURANCE

MEDICARE PLAN G INSURANCE

MEDICARE PLAN N INSURANCE

SERVICE AREA

MEDICARE STATEMENT

The Medicare Annual Enrollment Period is October 15th to December 7th. Steve Turner is not connected with or endorsed by the United States Government or the Federal Medicare Program. Some plans may not be available in your area, and any information I provide is limited to those offered. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

There’s no one-size-fits-all answer. Carefully evaluate your health status, anticipated medical needs, prescription drug usage, budget, preferred doctors and hospitals, and tolerance for network rules. During the Medicare Annual Enrollment Period (October 15th to December 7th), thoroughly research the specific plans available in your Florida county using the Medicare Plan Finder on Medicare.gov, compare their costs and benefits, and consider seeking free, personalized counseling from Florida’s SHINE (Serving Health Insurance Needs of Elders) program.