Can Life Insurance Beneficiary Be A Minor?

As an Insurance Agent and Broker with many years of experience helping Tampa, Saint Petersburg, and Clearwater Area Residents solve their biggest health care and financial challenges, I’ve sat at many kitchen tables in Hillsborough, Pinellas, and Pasco counties. One of the most common—and potentially most complicated—questions I hear from parents and grandparents is: “Can a minor be a life insurance beneficiary?”

The short answer is yes, you can name a minor as a beneficiary on a life insurance policy. However, as any resident of the Tampa-Saint Petersburg-Clearwater Metro Area knows, the “can” and the “should” are two very different things in the world of Florida law. In 2026, the legal landscape for protecting our children’s financial future has become more nuanced, and making a simple mistake today could result in your loved ones facing years of court battles and thousands of dollars in legal fees tomorrow.

Can Life Insurance Beneficiary Be A Minor?

In this deep-dive analysis, we will explore the pitfalls of naming a minor directly, the superior alternatives available to Tampa-Saint Petersburg-Clearwater Metro Area Residents, and how to compare different insurance plans to ensure your family is protected without the red tape.

The Reality of Naming a Minor as a Beneficiary in Florida

In the Tampa Bay Metro, we love our children and grandchildren, and our natural instinct is to leave them everything. But there is a massive legal hurdle: minors cannot legally own significant property or receive large sums of money directly.

If you name your 10-year-old child as the direct beneficiary of a $500,000 term life policy, and you pass away while they are still a minor, the insurance company will not cut a check to that child. Instead, because the child is not of legal age to enter into a contract or manage assets, the following typically occurs:

1. The Guardianship Trap

Under Florida law, if a minor is set to receive assets exceeding $15,000, the court must appoint a Guardian of the Property. This isn’t just a simple paperwork exercise at the Pinellas County Courthouse or the Hillsborough County Clerk’s Office. It is a formal, ongoing legal process.

- Court Oversight: The court will decide who manages the money. It might be the surviving parent, but it might not.

- Legal Fees: You can expect to pay anywhere from $3,000 to $6,000 just to establish the guardianship, with ongoing annual reporting fees that drain the child’s inheritance.

- Bonding Requirements: The guardian often has to pay for a “surety bond” to ensure they don’t mismanage the funds, adding another layer of expense.

2. The “Age of Majority” Cliff

Even if you navigate the guardianship, a second problem arises when the child turns 18. In Florida, once a child reaches the age of majority (18), the guardianship ends, and the child receives the entire lump sum.

As a broker who has served the Tampa, Saint Petersburg, and Clearwater Metro Area for decades, I always ask parents: “Do you want your 18-year-old to receive $500,000 all at once?” For most, the answer is a resounding “no.” At 18, many young adults lack the financial maturity to manage such a windfall, which could be spent on depreciating assets rather than the intended college education at USF or Hillsborough Community College.

Superior Alternatives for Tampa-Saint Petersburg-Clearwater Metro Area Residents

If naming a minor directly is a “Big Mistake,” what should you do instead? As an expert agent, I double-check the latest 2026 statutes to provide my clients with three primary strategies.

1. The Florida Uniform Transfers to Minors Act (UTMA)

The Florida UTMA (Statute Chapter 710) is a simpler way to name a minor. Instead of naming “Jane Doe,” you name “John Doe, as custodian for Jane Doe, under the Florida Uniform Transfers to Minors Act.”

- Pros: It avoids the immediate need for a court-appointed guardian. You choose the person (the custodian) who manages the money.

- Cons: In 2026, the UTMA still generally terminates at age 21 (or up to 25 if specifically elected at creation). While better than age 18, it still lacks the long-term control of a trust.

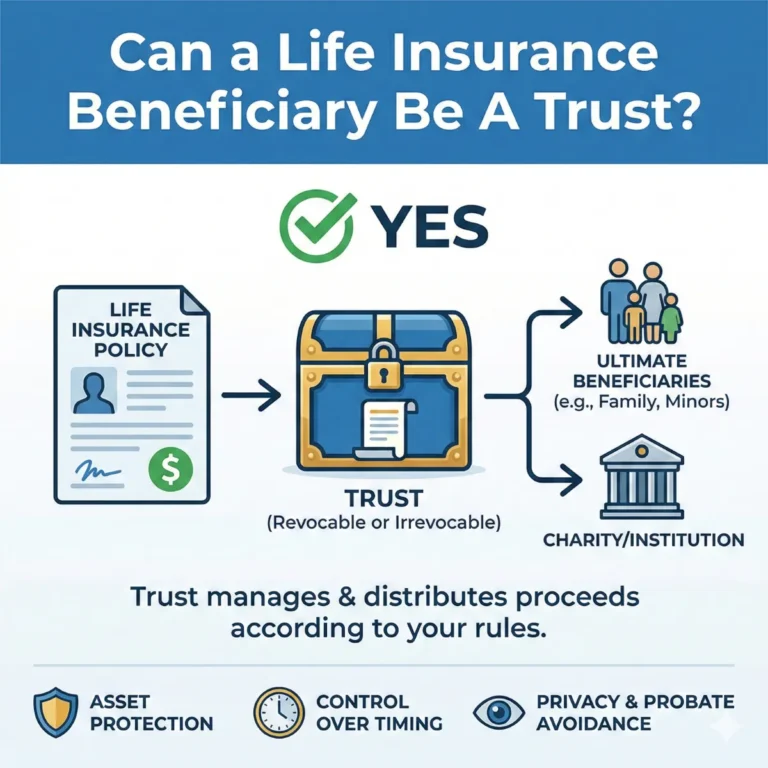

2. Establishing a Revocable Living Trust

This is the “Gold Standard” for families in Clearwater, St. Pete, and Tampa. You create a trust and name the trust as the beneficiary of the life insurance policy.

- Total Control: You decide exactly when the child gets the money (e.g., 25% at age 25, 25% at age 30).

- Spendthrift Protection: The money inside the trust is protected from the child’s future creditors or a messy divorce.

- Instructional Guidance: You can stipulate that the funds may be used only for “HEMS” (Health, Education, Maintenance, and Support).

3. Naming an Adult Custodian/Trustee

If you don’t want the complexity of a trust, you can name a trusted adult as the beneficiary with the understanding that they will use it for the child. However, I strongly advise against this. As an expert, I’ve seen cases where that adult gets sued, goes through a divorce, or simply spends the money themselves. The life insurance company only recognizes the named beneficiary’s legal right to the cash.

Comparing Insurance Plans: Which is Best for Your Family?

When comparing insurance plans available to Tampa, Saint Petersburg, and Clearwater Area Residents, we must consider the specific needs of the beneficiaries.

Term Life Insurance: The Budget-Friendly Shield

For most young families in Largo, Brandon, and Wesley Chapel, Term Life is the best fit.

- Pros: Highly affordable. You can secure a $1,000,000 death benefit for a low monthly premium, ensuring your children are protected through their college years.

- Cons: It expires. If you outlive the 30-year term, there is no payout for the kids.

Whole Life Insurance: The Permanent Pillar

Whole life is often chosen by grandparents in Safety Harbor or Sun City Center, looking to leave a guaranteed legacy.

- Pros: It never expires. It builds cash value that you can potentially borrow against to help with a grandchild’s private school tuition today.

- Cons: Significantly higher premiums than term insurance.

Indexed Universal Life (IUL): The Growth Engine

IUL is popular among the tech-savvy professionals in Downtown Tampa and Downtown St. Pete.

- Pros: Offers potential for market-linked growth without the risk of market losses. It’s an excellent vehicle for long-term wealth transfer to a trust.

- Cons: Requires more active management and understanding of “caps” and “participation rates.”

| Plan Type | Best For… | Tampa Bay Local Use Case |

| Term Life | Young Parents | Covering the mortgage on a Clearwater home until kids are 22. |

| Whole Life | Grandparents | Leaving a “Final Expense” fund plus a gift for grandkids. |

| IUL | Wealth Accumulators | Creating a tax-advantaged college fund while providing protection. |

Deep Analysis: The 2026 Costs of Care and Education in Tampa Bay

To understand how much insurance you need for your minor beneficiaries, we have to look at local data. In 2026, the costs in the Tampa-Saint Petersburg-Clearwater Metro Area are rising:

- Average Funeral Costs: A traditional burial in Pinellas County now averages between $12,000 and $15,000.

- Cost of Living: For a family of four in Tampa, the monthly cost of living (excluding rent) is roughly $5,500.

- Education: Four years at a state university in Florida is projected to cost over $100,000 for a child born today, including room and board.

As your broker, I perform a Needs Analysis that double-checks these local figures against your specific family goals to ensure your minor beneficiaries aren’t just “covered,” but are truly provided for.

Pros and Cons of “Child Riders”

Many of my clients in Saint Petersburg ask about adding a “Child Rider” to their own policy.

- The Pro: It’s incredibly cheap (often $5-$10 a month for $10,000-$20,000 of coverage). It ensures that if the unthinkable happens to a child, funeral costs are covered without financial strain.

- The Con: It is usually a small amount. It is not a substitute for a parent’s high-limit policy that provides for the child’s life after the parent is gone.

SEO Insights: Finding the Best Life Insurance for Families in Tampa

If you’ve been searching for “best life insurance for parents in Clearwater” or “how to name a child as beneficiary in Florida,” you are looking for more than just a price. You are looking for a strategy.

In the Tampa-Saint Petersburg-Clearwater Metro Area, we have access to top-tier carriers like Mutual of Omaha, Transamerica, MassMutual, and Nationwide. As an independent broker, I don’t work for them; I work for you. I use deep analytical tools to compare their “Child Rider” options, “Convertibility” features, and financial strength ratings (A.M. Best) to ensure the company you choose today will be there for your minor children 20 years from now.

Common Misconceptions (Double-Checked for Accuracy)

“My ex-spouse won’t get the money if I name the kids.”

False. If you name your minor children directly, and you pass away, the court will likely appoint the surviving parent (your ex-spouse) as the guardian of that property. If you want to prevent this, you must use a trust and name a different trustee.

“I don’t need a trust if I only have $50,000 in insurance.”

False. As we noted, Florida’s threshold for a formal guardianship is only $15,000. Even a minor policy can trigger the court system in Tampa or Clearwater.

“Social Security will take care of them.”

Partially True. Children of a deceased worker can receive survivor benefits, but in 2026, these are rarely enough to cover a mortgage in St. Petersburg or a private education. Life insurance is the “gap filler” that maintains their standard of living.

Steps to Protect Your Minor Beneficiaries Today

- Review Your Current Designations: Pull your policies for your home in Clearwater or your job in Tampa. If you see a minor’s name listed alone, call me immediately.

- Consult an Estate Attorney: I work closely with local attorneys who specialize in Florida probate and trust law to ensure your “Revocable Living Trust” is drafted correctly.

- Update Your Beneficiaries: We will coordinate with the insurance company to ensure the beneficiary is listed as your trust or a UTMA custodian.

- Compare Plans Annually: Life changes fast in the Tampa Bay Metro. A new baby, a new home in Safety Harbor, or a divorce means your insurance needs a “health check.”

Conclusion: Ensuring a Seamless Legacy

The question of whether a life insurance beneficiary can be a minor is straightforward, but the answer is complex. By naming a minor directly, you risk trapping their inheritance in a web of court oversight and unnecessary fees right here in the Tampa, Saint Petersburg, and Clearwater Metro Area. By utilizing trusts and custodial accounts, you ensure that every dollar you intended for their future actually reaches them—on your terms.

Don’t leave your child’s financial security to the chance of the court system. You deserve a professional who does the deep analysis, double-checks the data against current Florida law, and finds the absolute best plan for your unique family.

Steve Turner Insurance Specialist is an agent and broker here to answer all your questions. With years of experience helping Tampa-Saint Petersburg-Clearwater Metro Area Residents navigate these exact challenges, Steve brings the clarity and expertise you need to make the right choice.

The best part? Steve’s services are 100% free to you. Like all independent agents and brokers, he is compensated by the insurance company that you choose. This means you receive his years of expertise, localized research, and dedicated support at no out-of-pocket cost to you.

Would you like me to run a side-by-side comparison of the top term life policies that offer the best “Child Rider” and “Trust Ownership” flexibility for your family in the Tampa Bay area today?

Finding Your Trusted Advisor in the Florida Health Insurance Market

We have taken a very detailed look at the Tampa-Saint Petersburg-Clearwater metro area, the Health Insurance Market for 2026. We’ve seen how its clever design offers a modern solution for today’s retirees. We’ve also seen that while the plan’s benefits are stable and reliable, its monthly cost can vary significantly from one insurance company to another. Choosing the right company at the right price is the key to maximizing the value of Health Insurance in 2026.

This is where the guidance of an independent, licensed insurance agent becomes invaluable. A Health Insurance specialist acts as your personal shopper and advocate. They can instantly compare the rates for the same Health Insurance plan options from all the different carriers in your state. They can also provide insight into a company’s history of rate increases, which is a crucial factor in your long-term satisfaction.

It is essential to understand that this expert guidance is provided to you at absolutely no extra cost. The insurance industry is regulated so that the price of a plan is the same whether you buy it through an agent or directly from the company. When you enroll with an agent’s help, the insurance company pays them a commission. This system allows you to get free, unbiased, and professional advice to help you make the best possible choice.

To ensure you get the best value, it is usually best to use a licensed insurance agent, such as Steve Turner at SteveTurnerInsuranceSpecialist.com. Steve Turner is a licensed Agent/Broker contracted with most Insurance Carriers. An expert like Steve can help you navigate the 2026 Health Insurance market, find the most competitively priced Health Insurance plans for you, and ensure you have a Health Insurance plan that provides both financial security and true peace of mind.

OUR CLIENT REVIEWS

CONTACT STEVE TURNER INSURANCE AGENT & BROKER

I’m here to take your calls and emails and answer your questions 7 Days a week from 7:00 a.m. to 8:00 p.m., excluding posted holidays.

Steve Turner is a licensed agent, broker, and a longstanding member of the National Association of Benefits and Insurance Professionals®. Steve holds the prestigious designation of Registered Employee Benefits Consultant®. NABIP® is the preeminent organization for health insurance and employee benefits professionals and works diligently to ensure all Americans have access to high-quality, affordable Healthcare, and related services.

Steve Turner is a licensed agent appointed by Florida Blue.

EMAIL ME: 24×7

OFFICE LOCATION

Website: steveturnerinsurancespecialist.com

Email: [email protected]

Phone and Text: +1-813-388-8373

Business Hours:

Monday: 7 am to 8 pm

Tuesday: 7 am to 8 pm

Wednesday: 7 am to 8 pm

Thursday: 7 am to 8 pm

Friday: 7 am to 8 pm

Saturday: 7 am to 8 pm

Sunday: 7 am to 8 pm

SOCIAL FOLLOW + SHARE

LIFE INSURANCE POSTS

INSURANCE OFFERINGS

Can Life Insurance Beneficiary Be A Minor?

HEALTH INSURANCE

MEDICARE ADVANTAGE

MEDICARE SUPPLEMENT

PRESCRIPTION DRUGS

LIFE INSURANCE

DISABILITY INSURANCE

DENTAL INSURANCE

GROUP HEALTH INSURANCE

ACCIDENT INSURANCE

LONG TERM CARE INSURANCE

MEDICAID INSURANCE

MEDICARE INSURANCE

MEDICARE PART A INSURANCE

MEDICARE PART B INSURANCE

MEDICARE PART C INSURANCE

MEDICARE PART D INSURANCE

MEDICARE PLAN G INSURANCE

MEDICARE PLAN N INSURANCE

SERVICE AREA

MEDICARE STATEMENT

The Medicare Annual Enrollment Period is October 15th to December 7th. Steve Turner is not connected with or endorsed by the United States Government or the Federal Medicare Program. Some plans may not be available in your area, and any information I provide is limited to those offered. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

There’s no one-size-fits-all answer. Carefully evaluate your health status, anticipated medical needs, prescription drug usage, budget, preferred doctors and hospitals, and tolerance for network rules. During the Medicare Annual Enrollment Period (October 15th to December 7th), thoroughly research the specific plans available in your Florida county using the Medicare Plan Finder on Medicare.gov, compare their costs and benefits, and consider seeking free, personalized counseling from Florida’s SHINE (Serving Health Insurance Needs of Elders) program.