Can Life Insurance Be A Business Expense?

As an Insurance Agent and Broker with many years of experience helping Tampa, Saint Petersburg, and Clearwater Area Residents solve their most complex health care and financial challenges, I have sat across the desk from hundreds of business owners. Whether you are running a boutique law firm in Downtown St. Pete, a medical practice in the Westshore District, or a high-tech startup in Clearwater, the goal is the same: maximizing protection while minimizing the tax bite.

One of the most frequent questions I receive during our annual reviews is: “Can life insurance be a business expense?” In the 2026 tax landscape, the answer is a nuanced “sometimes.” For most Tampa-Saint Petersburg-Clearwater Metro Area Residents, life insurance is a personal expense paid with after-tax dollars. However, when you step into the world of business ownership, the rules change. Under the right circumstances, life insurance isn’t just a safety net; it becomes a powerful, tax-advantaged business tool that can be deducted as a legitimate expense.

Can Life Insurance Be A Business Expense?

In this deep-dive analysis, we will explore IRS regulations, the specific plans available to our local business community, and the strategic “pros and cons” of incorporating life insurance into your corporate ledger.

1. The General Rule: Personal vs. Business

For the average resident in Hillsborough or Pinellas County, life insurance premiums are a personal expense. The IRS generally views these as “personal, living, or family expenses” under Internal Revenue Code Section 262. Just as you cannot deduct your personal grocery bill at the local Publix, you cannot deduct the premium on a policy intended to protect your spouse and children.

However, the game changes when the policy is used as a tool for recruitment, retention, or risk mitigation within a business. To be deductible, the policy must qualify as a “necessary and ordinary” business expense, and—this is the most critical part—the business must not be a direct or indirect beneficiary of the policy.

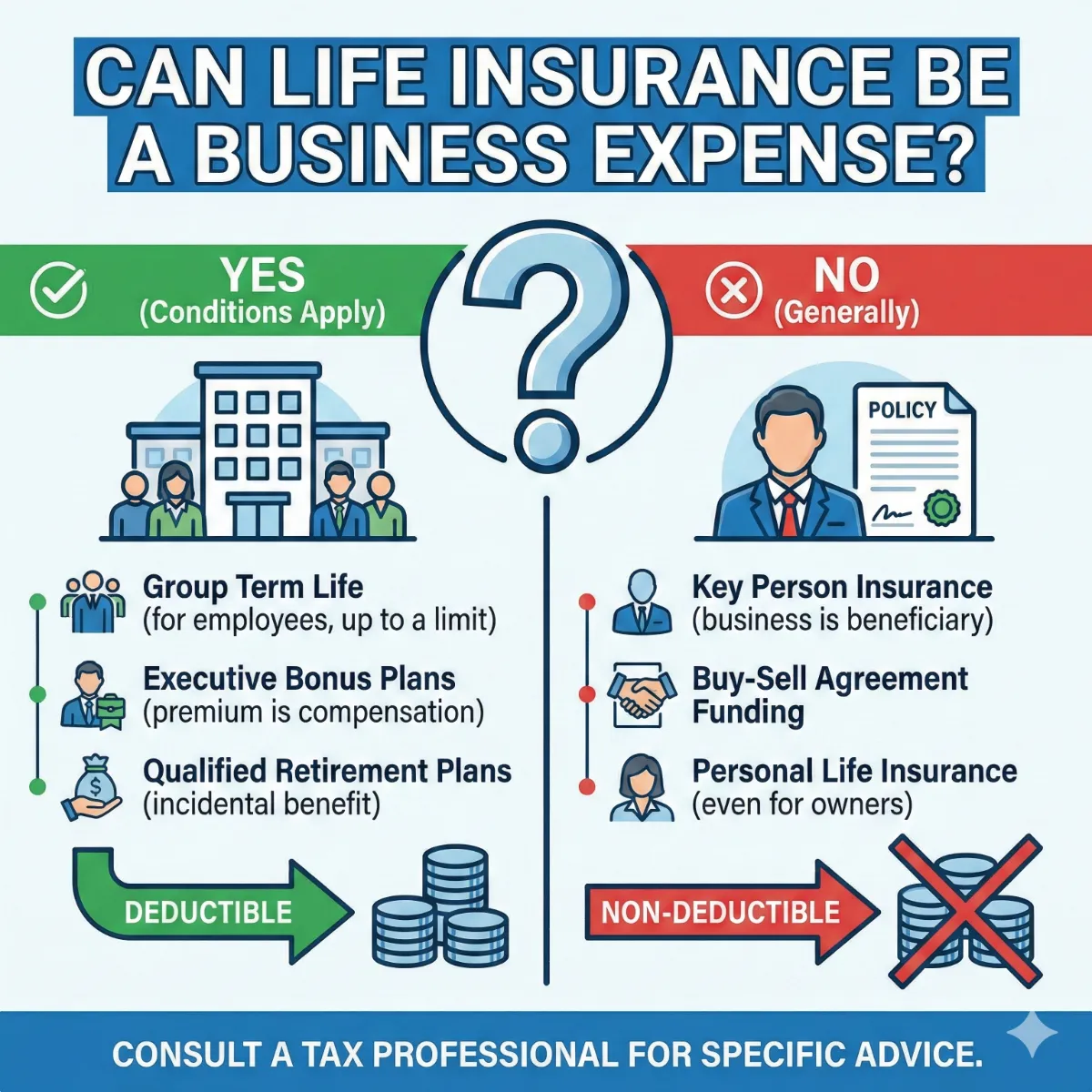

2. When It IS a Deductible Business Expense

For businesses in the Tampa, Saint Petersburg, and Clearwater Metro Area, there are three primary scenarios where premiums are generally tax-deductible.

A. Group Term Life Insurance (Section 79)

This is the most common way Tampa Bay Metro Area businesses utilize life insurance as a deduction. Under IRC Section 79, an employer can provide up to $50,000 of group term life insurance to employees, and the premiums are fully deductible by the business.

- The Benefit to the Employee: For the first $50,000 of coverage, the employee pays no income tax on the “value” of the benefit.

- Excess Coverage: If the business provides more than $50,000 in coverage, the business can still deduct the full premium. However, the employee must report the “imputed cost” of the excess coverage as taxable income (using the IRS “Table I” rates).

B. Executive Bonus Plans (Section 162)

Often used by high-end firms in Downtown Tampa to attract top talent, a Section 162 plan allows a business to pay the premiums on a life insurance policy owned by a key employee.

- The Structure: The business pays the premium directly to the insurance company.

- The Tax Treatment: The business deducts the premium as “compensation.” The employee reports the premium amount as a taxable bonus.

- The Advantage: It is a “selective” benefit. Unlike group plans, you don’t have to offer this to everyone. You can choose to bonus only your top performers in St. Pete or Clearwater.

C. Life Insurance as Alimony (Pre-2019 Agreements)

While not strictly a “business expense” for a corporation, for self-employed individuals or sole proprietors in the Tampa-Saint Petersburg-Clearwater Metro Area who have divorce agreements finalized before December 31, 2018, premiums paid for a policy required by the court may still be deductible as alimony. (Note: This does not apply to agreements finalized after that date due to the Tax Cuts and Jobs Act changes.)

3. When It Is NOT a Deductible Business Expense

As an expert who double-checks every data point, I must warn you: the IRS is very strict on “double-dipping.” If the policy payout is tax-free to the business, the premiums are almost never deductible.

A. Key Person Insurance

If your Clearwater-based business buys a policy on a “Key Person” (like a lead engineer or a founding partner) and the business is the beneficiary, the premiums are not deductible.

- Why? Under IRC Section 264(a)(1), you cannot deduct premiums if the taxpayer is a beneficiary.

- The Silver Lining: When the key person passes away, the death benefit flows into the business income tax-free, providing the liquidity needed to find a replacement or pay off business debts.

B. Buy-Sell Agreement Funding

In a “stock redemption” or “entity purchase” agreement, the business retains ownership of the policies on the partners. When a partner dies, the business uses the insurance money to buy back their shares.

- Tax Status: Non-deductible. The business is the beneficiary.

C. Collateral for a Business Loan

If your bank in Tampa requires you to have life insurance to secure a business loan, many owners assume those premiums are deductible. They are not. Even though the insurance is a requirement for the “business loan,” the IRS still views it as a personal asset used as collateral.

4. Comparing Insurance Plans: A Deep Analysis for Business Owners

When we compare insurance plans available to Tampa, Saint Petersburg, and Clearwater Area Residents, we have to look at the “Net Cost” of each policy. This involves calculating the After-Tax Cost.

If a business in Hillsborough County is in the 21% federal corporate tax bracket, the math for a deductible premium looks like this:

$$Net Cost = Premium \times (1 – Tax Rate)$$

For a $10,000 deductible premium, the actual out-of-pocket cost to the business is $7,900. If the premium is not deductible, the cost remains $10,000. This 21% “discount” is why structuring your plan correctly is vital.

5. Pros and Cons: Using Life Insurance in a Business Context

The Pros:

- Tax Efficiency: Deductible premiums (where allowed) lower the corporate tax bill.

- Retention: “Golden Handcuffs” like Section 162 plans keep your best employees from jumping ship to competitors in Orlando or Miami.

- Liquidity: Provides immediate cash to a St. Petersburg business during a crisis, preventing a “fire sale” of assets.

- Asset Protection: Under Florida law, the cash value in life insurance is generally protected from creditors—a massive “pro” for entrepreneurs.

The Cons:

- Complexity: Requires coordination between your Insurance Broker, CPA, and Attorney.

- Compliance: Failing to follow IRC Section 101(j) (Employer-Owned Life Insurance rules) can make the death benefit taxable—a catastrophic error.

- Cost: Permanent policies (Whole Life/Universal Life) have higher initial costs than term insurance.

6. The 2026 “Connelly” Impact: A Warning for Tampa Bay Business Owners

In 2026, we are still dealing with the fallout of the Supreme Court’s Connelly v. United States decision. This ruling changed how “Entity Purchase” buy-sell agreements are valued for estate taxes.

Expert Analysis: If your business in Tampa owns a life insurance policy to buy back your shares, the Supreme Court ruled that the insurance proceeds increase the value of the company for estate tax purposes. This can lead to a massive, unexpected estate tax bill for your heirs.

As a broker who stays on the cutting edge, I am currently helping my Clearwater and St. Pete clients pivot toward “Cross-Purchase” or “Trust-Owned” arrangements to avoid this “Connelly Trap.”

7. Strategic Advice for Tampa-Saint Petersburg-Clearwater Residents

If you are considering making life insurance a business expense, follow this local “Success Checklist”:

- Define the Goal: Are you trying to save on taxes today (Deductible Group Term) or protect the business for tomorrow (Non-deductible Key Person)?

- Select Local Carriers: While we examine national titans like Mutual of Omaha and MassMutual, we also assess how carriers navigate the specific regulatory environment in Florida.

- Audit Your Current Buy-Sell: If you haven’t updated your buy-sell agreement since 2024, you are likely at risk due to the Connelly decision.

- Use “Notice and Consent”: Under IRC 101(j), you must get written consent from an employee before you buy a policy on their life. If you miss this step, the IRS will tax the death benefit.

8. Summary Table: Deductibility at a Glance (2026)

| Insurance Type | Is it Deductible? | Who is the Beneficiary? | Best For… |

| Group Term (first $50k) | Yes | Employee’s Family | Employee Benefits |

| Section 162 Bonus | Yes | Employee’s Choice | Executive Retention |

| Key Person | No | The Business | Business Continuity |

| Buy-Sell (Entity) | No | The Business | Ownership Transfer |

| Collateral Assignment | No | The Lender | Securing a SBA Loan |

9. SEO Long Tail Keywords for Local Business Searches

To find the best solutions in our metro area, residents often search for these specific terms:

- “Best group life insurance rates for small businesses in Tampa”

- “Tax-deductible life insurance for Clearwater law firms”

- “Key man insurance quotes Saint Petersburg, Florida.”

- “Executive bonus plan life insurance Hillsborough County”

- “Buy-sell agreement funding strategies for St. Pete entrepreneurs”

10. Frequently Asked Questions (Expert Double-Check)

“Can I deduct my own life insurance as a self-employed person in Tampa?”

Generally, no. The IRS views your own life insurance as a personal expense, even if you pay for it out of your business account. The exception is if you are paying employee premiums.

“Does Florida have a state tax on life insurance premiums?”

Florida does not have a state income tax, so there is no “state-level” deduction to worry about. However, insurance companies pay a 1.75% Premium Tax to the state, which is usually factored into your quoted rate.

“What if I use my life insurance to fund my retirement?”

Many business owners in Clearwater use Cash Value Life Insurance (like IUL or Whole Life) to build a “supplemental retirement fund.” While the premiums are not deductible, the cash grows tax-deferred, and the income you take out in retirement is generally tax-free through policy loans.

Conclusion: Turning a Cost into a Catalyst

So, can life insurance be a business expense? In the Tampa, Saint Petersburg, and Clearwater Metro Area, it absolutely can—provided you have the right architecture in place. It can be the “Golden Handcuffs” that keep your best employees in St. Pete, the shield that protects your practice in Tampa, or the tax-deductible benefit that secures your family in Clearwater.

However, the difference between a “Tax-Deductible Tool” and a “Tax Trap” is found in the details. You need a deep analysis of your corporate structure, your long-term goals, and the latest IRS rulings.

Steve Turner, Insurance Specialist, is here to answer all your questions. As a dedicated agent and broker who has spent many years helping Tampa-Saint Petersburg-Clearwater Metro Area Residents solve their biggest health care and financial challenges, Steve knows that business ownership is hard enough without having to guess at insurance regulations. He performs the double-checks, runs the side-by-side comparisons, and works with your CPA to ensure your plan is airtight.

The best part? Steve’s services are 100% free to you. Like all independent agents and brokers, he is paid by the insurance company that you choose. This means you get expert, unbiased analysis and a localized strategy for your business at no out-of-pocket cost.

Would you like me to run a customized “Tax-Efficiency Audit” of your current business life insurance policies to see if we can unlock any new deductions for your Tampa Bay company today?

Finding Your Trusted Advisor in the Florida Health Insurance Market

We have taken a very detailed look at the Tampa-Saint Petersburg-Clearwater metro area, the Health Insurance Market for 2026. We’ve seen how its clever design offers a modern solution for today’s retirees. We’ve also seen that while the plan’s benefits are stable and reliable, its monthly cost can vary significantly from one insurance company to another. Choosing the right company at the right price is the key to maximizing the value of Health Insurance in 2026.

This is where the guidance of an independent, licensed insurance agent becomes invaluable. A Health Insurance specialist acts as your personal shopper and advocate. They can instantly compare the rates for the same Health Insurance plan options from all the different carriers in your state. They can also provide insight into a company’s history of rate increases, which is a crucial factor in your long-term satisfaction.

It is essential to understand that this expert guidance is provided to you at absolutely no extra cost. The insurance industry is regulated so that the price of a plan is the same whether you buy it through an agent or directly from the company. When you enroll with an agent’s help, the insurance company pays them a commission. This system allows you to get free, unbiased, and professional advice to help you make the best possible choice.

To ensure you get the best value, it is usually best to use a licensed insurance agent, such as Steve Turner at SteveTurnerInsuranceSpecialist.com. Steve Turner is a licensed Agent/Broker contracted with most Insurance Carriers. An expert like Steve can help you navigate the 2026 Health Insurance market, find the most competitively priced Health Insurance plans for you, and ensure you have a Health Insurance plan that provides both financial security and true peace of mind.

OUR CLIENT REVIEWS

CONTACT STEVE TURNER INSURANCE AGENT & BROKER

I’m here to take your calls and emails and answer your questions 7 Days a week from 7:00 a.m. to 8:00 p.m., excluding posted holidays.

Steve Turner is a licensed agent, broker, and a longstanding member of the National Association of Benefits and Insurance Professionals®. Steve holds the prestigious designation of Registered Employee Benefits Consultant®. NABIP® is the preeminent organization for health insurance and employee benefits professionals and works diligently to ensure all Americans have access to high-quality, affordable Healthcare, and related services.

Steve Turner is a licensed agent appointed by Florida Blue.

EMAIL ME: 24×7

OFFICE LOCATION

Website: steveturnerinsurancespecialist.com

Email: [email protected]

Phone and Text: +1-813-388-8373

Business Hours:

Monday: 7 am to 8 pm

Tuesday: 7 am to 8 pm

Wednesday: 7 am to 8 pm

Thursday: 7 am to 8 pm

Friday: 7 am to 8 pm

Saturday: 7 am to 8 pm

Sunday: 7 am to 8 pm

SOCIAL FOLLOW + SHARE

LIFE INSURANCE POSTS

INSURANCE OFFERINGS

Can Life Insurance Be A Business Expense in Florida?

HEALTH INSURANCE

MEDICARE ADVANTAGE

MEDICARE SUPPLEMENT

PRESCRIPTION DRUGS

LIFE INSURANCE

DISABILITY INSURANCE

DENTAL INSURANCE

GROUP HEALTH INSURANCE

ACCIDENT INSURANCE

LONG TERM CARE INSURANCE

MEDICAID INSURANCE

MEDICARE INSURANCE

MEDICARE PART A INSURANCE

MEDICARE PART B INSURANCE

MEDICARE PART C INSURANCE

MEDICARE PART D INSURANCE

MEDICARE PLAN G INSURANCE

MEDICARE PLAN N INSURANCE

SERVICE AREA

MEDICARE STATEMENT

The Medicare Annual Enrollment Period is October 15th to December 7th. Steve Turner is not connected with or endorsed by the United States Government or the Federal Medicare Program. Some plans may not be available in your area, and any information I provide is limited to those offered. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

There’s no one-size-fits-all answer. Carefully evaluate your health status, anticipated medical needs, prescription drug usage, budget, preferred doctors and hospitals, and tolerance for network rules. During the Medicare Annual Enrollment Period (October 15th to December 7th), thoroughly research the specific plans available in your Florida county using the Medicare Plan Finder on Medicare.gov, compare their costs and benefits, and consider seeking free, personalized counseling from Florida’s SHINE (Serving Health Insurance Needs of Elders) program.