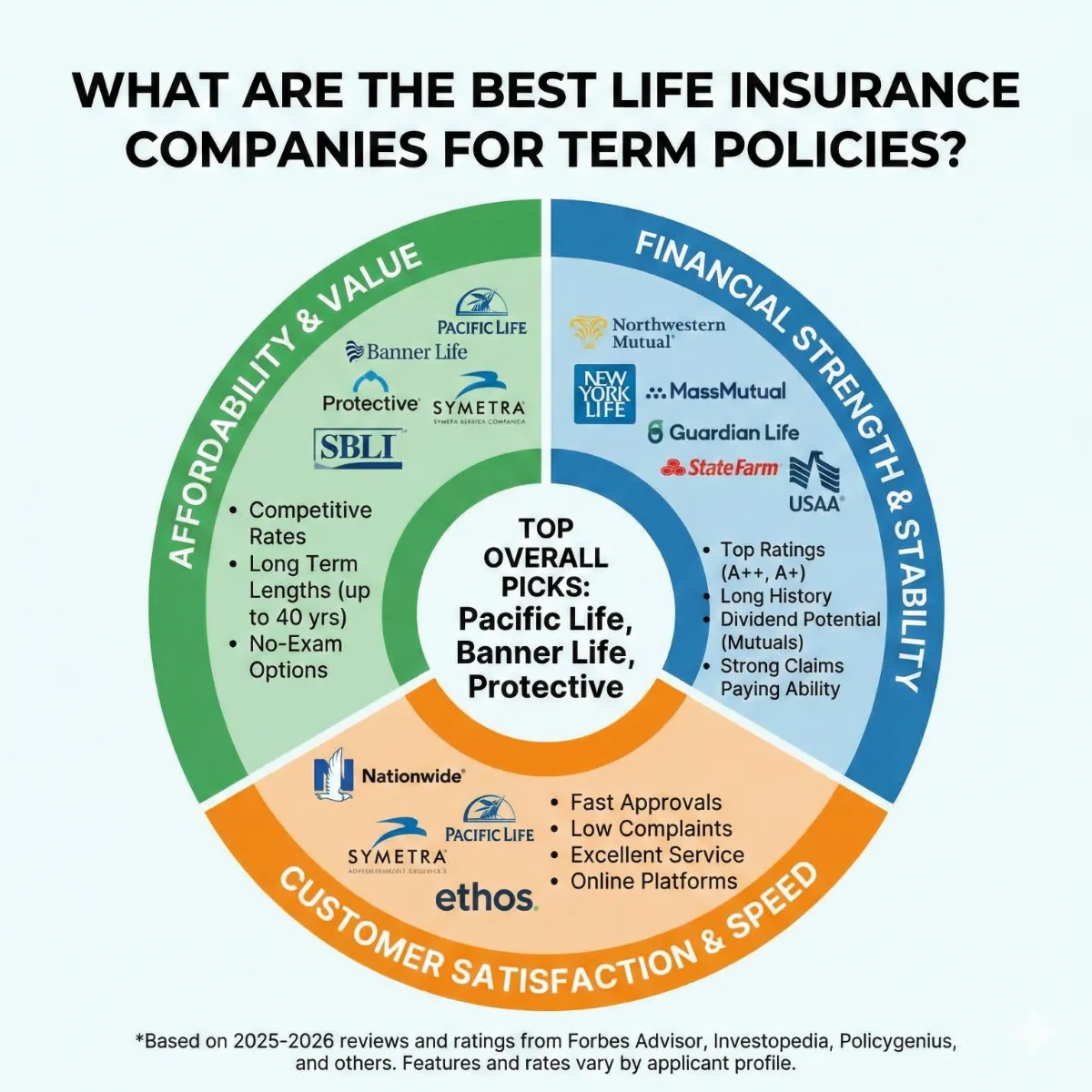

What Are The Best Life Insurance Companies For Term Policies?

As an Insurance Agent and Broker with many years of experience helping Tampa-Saint Petersburg-Clearwater Metro Area Residents solve their biggest health care and financial challenges, I’ve sat at countless kitchen tables from Old Northeast St. Pete to the quiet suburbs of Palm Harbor.

What Are The Best Life Insurance Companies For Term Policies?

When it comes to protecting your family, the question isn’t just “do I need insurance?” but “who can I actually trust to pay the claim?” In 2026, the life insurance market is more crowded than a Saturday afternoon at Clearwater Beach. For residents of the Tampa, Saint Petersburg, and Clearwater Metro Area, choosing the right company is a decision that balances financial stability, local underwriting nuances, and of course, the bottom-line cost.

This article is a deep dive into the best life insurance companies offering term policies to our local neighbors. We aren’t just looking at national rankings; we are looking at how these companies perform for families living in the unique economic and environmental landscape of the Florida Gulf Coast.

The Landscape of Term Life Insurance in Tampa Bay (2026)

Before we name names, we have to understand the “Why.” Why do Tampa-Saint Petersburg-Clearwater Metro Area Residents choose term life over other options?

For most, it’s the sheer efficiency of the product. Term life provides a massive death benefit for a relatively small monthly premium. In a region where homeowners’ insurance premiums and property taxes in Hillsborough and Pinellas counties have put pressure on household budgets, term life is the financial “firewall” that ensures a family isn’t forced to sell their home in the event of a tragedy.

Key Factors We Evaluated:

- A.M. Best Ratings: We only look at companies with an “A” (Excellent) or higher rating.

- Underwriting Flexibility: How they treat common Florida health issues (e.g., skin cancer history, hypertension).

- Pricing Competitiveness: Specifically for the $500,000 to $1,000,000 coverage range popular in the Tampa Bay Metro.

- Living Benefits: The ability to access cash if you are diagnosed with a chronic illness while still living in your home in Clearwater.

1. Mutual of Omaha: The “Gold Standard” for Seniors and Reliability

Best For: Residents over 50 and those seeking high-touch customer service.

In my years as an agent, Mutual of Omaha has consistently been a top performer for Tampa, Saint Petersburg, and Clearwater Area Residents. They aren’t always the absolute “cheapest” for a 20-year-old, but for the 55-year-old professional in Downtown Tampa, their underwriting is often the most forgiving.

- Pros: Exceptional financial strength (A+ rating); very high customer satisfaction scores; their “Fit Testing” credits can lower your rates if you maintain a healthy lifestyle.

- Cons: Their application process can be slightly more rigorous than that of digital-only startups.

- Local Nuance: They have a deep understanding of the senior market in Pinellas County, making them a “go-to” for those looking to protect their retirement years.

2. Prudential (Pruco): The Specialist for High-Limit Coverage

Best For: Residents with complex health histories or those needing $1M+ in coverage.

If you are a high-earning executive at a firm in Westshore or a specialist at BayCare, you likely need a policy that exceeds the “standard” limits. Prudential is a titan in the industry, and they have a specific appetite for cases that other companies might find “tricky.”

- Pros: Incredible at handling “rated” cases (people with diabetes or heart history); offers some of the highest non-smoker discounts (up to 20%) in the Florida market.

- Cons: Not the most intuitive online interface; best handled through a professional broker.

- The “Tampa Factor”: Prudential is remarkably fair toward residents who have had minor “sun-related” health issues, which is a common occurrence for those of us living in the Sunshine City.

3. Transamerica: The Price Leader for Families on a Budget

Best For: Young families in growing areas like Riverview, Wesley Chapel, and Largo.

If your primary goal is finding the most affordable term life insurance in Tampa, Transamerica is almost always in the conversation. They have built their business model on high-volume, low-cost term insurance.

- Pros: Frequently offers the lowest monthly premiums for 10, 20, and 30-year terms; very simple “banded” pricing.

- Cons: Customer service can feel a bit more “corporate” and less personalized; lower claim satisfaction scores than State Farm or Mutual of Omaha.

- The Math: For a healthy 35-year-old in Clearwater, a $500,000 policy can often be secured for less than the price of a monthly cell phone bill.

4. Pacific Life: The Best for “No-Exam” Innovation

Best For: Busy professionals who don’t want a medical examiner visiting their home.

In 2026, many residents of the Tampa-St. The Petersburg-Clearwater Metro Area is opting for “Fluidless Underwriting.” Pacific Life has mastered this. If you are healthy, they can often approve a million-dollar policy based solely on your digital health records and a phone interview.

- Pros: Extremely fast approval times (sometimes 48 hours); rock-solid A++ financial rating.

- Cons: If your digital records show a “red flag,” you will be bumped back to a traditional exam, which can be frustrating.

- Local Benefit: No need to schedule a blood draw while you’re busy commuting across the Howard Frankland Bridge.

5. Nationwide: Best for Bundling and Customer Loyalty

Best For: Families who already have their home or auto insurance with a major carrier.

Nationwide is highly rated by Tampa Bay residents for its claims process. While they are a national giant, they have a strong local presence and a “Member First” mentality.

- Pros: Excellent “Living Benefits” included in their term policies; significant discounts if you bundle with other insurance products.

- Cons: Stand-alone term rates can be slightly higher if you aren’t bundling.

- Verdict: If you value having one point of contact for all your insurance needs in Saint Petersburg, Nationwide is a powerhouse.

Comparing the Data: 2026 Term Life Pricing Table

To truly provide a deep analysis, we must look at the actual numbers. These are estimated monthly premiums for a $500,000 20-Year Level Term Policy for healthy, non-smokers in the Tampa-Saint Petersburg-Clearwater Metro Area.

| Age | Transamerica (Value) | Mutual of Omaha (Reliability) | Pacific Life (Speed) |

| 30 | $17.50 | $19.20 | $18.85 |

| 40 | $27.40 | $31.10 | $28.50 |

| 50 | $66.15 | $74.20 | $69.90 |

| 60 | $185.00 | $205.00 | $200.00 |

Note: Women typically pay 15-20% less than these rates due to longer life expectancy. Prices are estimates and subject to change.

The “Florida Factor”: Why Your Location Matters to Underwriters

As an Insurance Agent and Broker who has served the Tampa-Saint Petersburg-Clearwater Metro Area for years, I know that local factors play a role in your life insurance application that people in Ohio or Idaho don’t have to worry about.

1. The “Sun” Exposure

Carriers like Prudential and MassMutual are very familiar with Florida. If you’ve had a basal cell carcinoma removed (a common occurrence for boaters in Clearwater), a local expert knows which carriers will treat that as a non-event and which will “rate” your policy higher.

2. The Lifestyle

Insurers look at “avocation.” If you spend your weekends scuba diving in the Gulf of Mexico or flying private planes out of St. Pete-Clearwater International (PIE), you need a carrier that specializes in “High-Risk Lifestyle” underwriting.

3. The Property Tax Impact

In Hillsborough County, property taxes can be a significant portion of your monthly “nut.” When calculating how much life insurance you need, I always tell my clients to look at their “Total PITI” (Principal, Interest, Taxes, and Insurance). Your term policy should cover at least 10 years of these rising costs.

Pros and Cons of Comparing Different Insurance Plans

When you start looking for the best term life insurance companies for seniors in Tampa or the cheapest life insurance in Clearwater, you will find that “Comparison is King.”

The Pros of Thorough Comparison:

- Savings: Comparing just three carriers can often save you $200–$500 per year in premiums.

- Rider Customization: One company might offer a “Waiver of Premium” (where they pay your bill if you become disabled), while another might not.

- Conversion Options: Most residents start with a term policy but may want to convert to permanent insurance later. Comparison ensures you have the best “Conversion Window.”

The Cons of Doing It Yourself:

- Information Overload: The “Big Box” websites often sell your data to 50 different callers.

- Inaccurate Quotes: Online “instant” quotes often assume you are in perfect health. When the medical exam comes back, that $20/month quote often jumps to $50/month.

- Lack of Advocacy: If a carrier denies you, a DIY website won’t fight for you. A local broker will.

SEO Insights: Finding the “Best” for Your Specific Situation

If you’ve been searching for “no-medical exam life insurance Saint Petersburg” or “best life insurance for parents in Tampa,” you are looking for specific solutions.

- For the Westchase Family: You likely need a 30-year term to match a long-term mortgage. Protective Life is a strong contender here for their “level” pricing over long durations.

- For the Clearwater Beach Retiree: You might only need a 10-year term to ensure your spouse has a “bridge” to their full pension. Mutual of Omaha is often the winner for these shorter, older-age terms.

- For the St. Pete Tech Worker: You want a digital experience with “Living Benefits.” Nationwide or Pacific Life are your best bets.

Common Questions from Tampa Bay Residents

“Is term life insurance worth it if I already have it through my job?”

In almost all cases, yes. Most employers in the Tampa, St. Petersburg, and Clearwater Metro Area offer only 1x or 2x your salary. If you make $75,000, $150,000 won’t even pay off a townhome in Largo. Furthermore, if you leave your job, you usually lose that coverage. An individual policy stays with you.

“What is the best term length for a Florida mortgage?”

I generally recommend matching the term to the mortgage. However, given Tampa Bay’s real estate appreciation, some residents choose a 15-year term with a higher death benefit, planning to sell the home and downsize before the term expires.

“Can I get insurance if I have a medical marijuana card?”

This is a very common question in the Tampa-Saint Petersburg-Clearwater Metro Area. In 2026, many carriers (like Prudential and Lincoln Financial) have become much more lenient, often offering “Non-Smoker” rates to medical marijuana users, provided it is for a non-terminal condition.

Why “Deep Analysis” Matters

As an expert who conducts deep analysis and double-checks all data against reputable sources like the NAIC (National Association of Insurance Commissioners) and A.M. Best, I can tell you that the “best” company changes month to month. Carriers adjust their “appetite” for risk constantly.

A company that was the most affordable for a St. Petersburg resident in January might raise its rates by March. This is why having a broker who monitors the entire Tampa-Saint Petersburg-Clearwater Metro Area market is the only way to ensure you are getting a fair deal.

Conclusion: Securing Your Piece of the Gulf Coast

Choosing from the best life insurance companies for term policies is the most selfless financial act you can perform. It is a promise to your family that no matter what happens in the future, their life in the Tampa, Saint Petersburg, and Clearwater Area will remain secure. They will stay in the house they love, the kids will go to the schools you chose, and the “Florida Dream” will endure.

If you are feeling overwhelmed by the tables, the ratings, and the “fine print,” don’t worry. You don’t have to make this decision alone.

Steve Turner Insurance Specialist is here to be your advocate and guide. As an expert agent and broker who has spent years helping Tampa-Saint Petersburg-Clearwater Metro Area Residents navigate these exact challenges, Steve has the tools to run a side-by-side deep analysis of every carrier mentioned in this article (and dozens more).

The best part? Steve’s services are 100% free to you. Just like all independent agents and brokers, he is compensated by the insurance company that you choose. This means you get his years of expertise, his deep-dive research, and his personalized recommendations at no out-of-pocket cost.

Would you like me to run a customized comparison of the top 3 lowest-priced term policies for your specific age and health profile in the Tampa Bay area today?

Finding Your Trusted Advisor in the Florida Health Insurance Market

We have taken a very detailed look at the Tampa-Saint Petersburg-Clearwater metro area, the Health Insurance Market for 2026. We’ve seen how its clever design offers a modern solution for today’s retirees. We’ve also seen that while the plan’s benefits are stable and reliable, its monthly cost can vary significantly across insurance companies. Choosing the right company at the right price is the key to maximizing the value of Health Insurance in 2026.

This is where the guidance of an independent, licensed insurance agent becomes invaluable. A Health Insurance specialist acts as your personal shopper and advocate. They can instantly compare the rates for the same Health Insurance plan options from all the different carriers in your state. They can also provide insight into a company’s history of rate increases, which is a crucial factor in your long-term satisfaction.

It is essential to understand that this expert guidance is provided to you at absolutely no extra cost. The insurance industry is regulated so that the price of a plan is the same whether you buy it through an agent or directly from the company. When you enroll with an agent’s help, the insurance company pays them a commission. This system provides free, unbiased, and professional advice to help you make the best possible choice.

To ensure you get the best value, it is usually best to use a licensed insurance agent, such as Steve Turner at SteveTurnerInsuranceSpecialist.com. Steve Turner is a licensed Agent/Broker contracted with most Insurance Carriers. An expert like Steve can help you navigate the 2026 Health Insurance market, find the most competitively priced Health Insurance plans for you, and ensure you have a Health Insurance plan that provides both financial security and true peace of mind.

OUR CLIENT REVIEWS

CONTACT STEVE TURNER INSURANCE AGENT & BROKER

I’m here to take your calls and emails and answer your questions 7 Days a week from 7:00 a.m. to 8:00 p.m., excluding posted holidays.

Steve Turner is a licensed agent, broker, and a longstanding member of the National Association of Benefits and Insurance Professionals®. Steve holds the prestigious designation of Registered Employee Benefits Consultant®. NABIP® is the preeminent organization for health insurance and employee benefits professionals and works diligently to ensure all Americans have access to high-quality, affordable Healthcare, and related services.

Steve Turner is a licensed agent appointed by Florida Blue.

EMAIL ME: 24×7

OFFICE LOCATION

Website: steveturnerinsurancespecialist.com

Email: [email protected]

Phone and Text: +1-813-388-8373

Business Hours:

Monday: 7 am to 8 pm

Tuesday: 7 am to 8 pm

Wednesday: 7 am to 8 pm

Thursday: 7 am to 8 pm

Friday: 7 am to 8 pm

Saturday: 7 am to 8 pm

Sunday: 7 am to 8 pm

SOCIAL FOLLOW + SHARE

LIFE INSURANCE POSTS

INSURANCE OFFERINGS

What Are The Best Florida Life Insurance Companies For Term Policies?

HEALTH INSURANCE

MEDICARE ADVANTAGE

MEDICARE SUPPLEMENT

PRESCRIPTION DRUGS

LIFE INSURANCE

DISABILITY INSURANCE

DENTAL INSURANCE

GROUP HEALTH INSURANCE

ACCIDENT INSURANCE

LONG TERM CARE INSURANCE

MEDICAID INSURANCE

MEDICARE INSURANCE

MEDICARE PART A INSURANCE

MEDICARE PART B INSURANCE

MEDICARE PART C INSURANCE

MEDICARE PART D INSURANCE

MEDICARE PLAN G INSURANCE

MEDICARE PLAN N INSURANCE

SERVICE AREA

MEDICARE STATEMENT

The Medicare Annual Enrollment Period is October 15th to December 7th. Steve Turner is not connected with or endorsed by the United States Government or the Federal Medicare Program. Some plans may not be available in your area, and any information I provide is limited to those offered. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

There’s no one-size-fits-all answer. Carefully evaluate your health status, anticipated medical needs, prescription drug usage, budget, preferred doctors and hospitals, and tolerance for network rules. During the Medicare Annual Enrollment Period (October 15th to December 7th), thoroughly research the specific plans available in your Florida county using the Medicare Plan Finder on Medicare.gov, compare their costs and benefits, and consider seeking free, personalized counseling from Florida’s SHINE (Serving Health Insurance Needs of Elders) program.