Medicare Part B Insurance Tampa FL

Steve Turner Insurance Specialist offers you, your family and your business the complete array of Insurance Services you need to protect and provide for their Medicare Part B Insurance Tampa FL needs.

My goals are to (1) Listen to you tell me about your insurance needs, budget, and the outcome you require, and (2) Educate you on your various options, and (3) Setup the insurance plans you have selected and get your insurance coverage established.

Not sure what what type of insurance is best for your Personal, Family, or Business? No worries! Most of my clients aren’t sure when they first reach out to us. I’ll discuss with you all your insurance options pro’s and con’s so YOU can make the choices that fit your budget.

Tap the “+1.813.388.8373” button to call me now, or the “Book-A-Call” button to pick a time on my calendar for a chat. I look forward to answering your questions and helping you find the right insurance to fit your needs.

OUR RESULTS

LISTENING SKILLS

SCORE = 100

PLAN CHOICES

SCORE = 100

BUDGET FIT

SCORE = 100

Medicare Part B Insurance Tampa FL

As a Tampa, FL-based independent insurance agent with many years of experience, I must first clarify a crucial point that is a common source of confusion for Tampa residents: there are no “Medicare Part B Insurance Tampa FL Plans” that private companies or agents offer. Medicare Part B is your Medical Insurance benefit, provided directly by the federal government. It is not a commercial plan you can choose here in Tampa or anywhere else.

What we, as expert Tampa-based Medicare Part B Insurance agents, do offer are the private insurance solutions specifically designed to manage the significant and, most importantly, uncapped out-of-pocket costs that come with your Medicare Part B Insurance benefit. The primary financial risk of Medicare Part B Insurance for Tampa, FL, beneficiaries is its 20% coinsurance, which has no annual limit. Our service is to help Tampa, FL residents choose the best of two primary solutions to protect themselves from this risk:

Medicare Supplement (Medigap) Plans, which pay the 20% for you, or Medicare Advantage (Part C) Plans, which replace the 20% coinsurance with a system of predictable copayments and an annual out-of-pocket maximum. When choosing an agent in Tampa, it is essential to ask them to clearly explain how each of these two paths protects you from the unlimited 20% coinsurance risk of Part B.

A Tampa Expert’s Guide to Covering Your Doctor & Outpatient Costs

As a Tampa-based Medicare expert with many years of experience, I often have new clients here in Tampa come to me asking to compare “Medicare Part B Insurance Tampa FL plans.” It is a perfectly logical question, but it’s based on one of the most common points of confusion in the entire Medicare system. The simple truth is, Medicare Part B isn’t a plan you choose from a list like you would with other types of insurance. Medicare Part B Insurance Tampa FL is your foundational Medical Insurance from the federal government.

The real, critical choice Tampa, FL residents must make is how you will protect your retirement savings right here in Hillsborough County from Medicare Part B Insurance’s significant and potentially catastrophic out-of-pocket costs. This is where we, as independent insurance agents, provide our most valuable service to our Tampa clients. Our job is not to “offer” you Part B, but to provide you with the expert guidance and the private insurance solutions specifically designed to cover the costs that Medicare Part B Insurance Tampa FL leaves behind.

This guide will serve as a comprehensive resource for Tampa, FL beneficiaries. First, we will demystify what your government Part B benefit covers and, more importantly, what it costs you. Then, we will detail the private insurance solutions we offer to protect Tampa, FL residents from those costs. Finally, we will arm you with the essential questions you must ask to choose the right Tampa-area agent to be your trusted guide in this critical decision.

Part 1: Demystifying Medicare Part B Insurance Tampa FL – Your Federal Medical Benefit (And Its Costs)

Before you can choose a plan to cover the gaps, you need to understand the gaps themselves for Tampa beneficiaries. If Part A is your “Hospital Insurance,” Medicare Part B Insurance is your “Medical Insurance” for everything that happens outside of an inpatient hospital stay, such as at an outpatient clinic in Tampa.

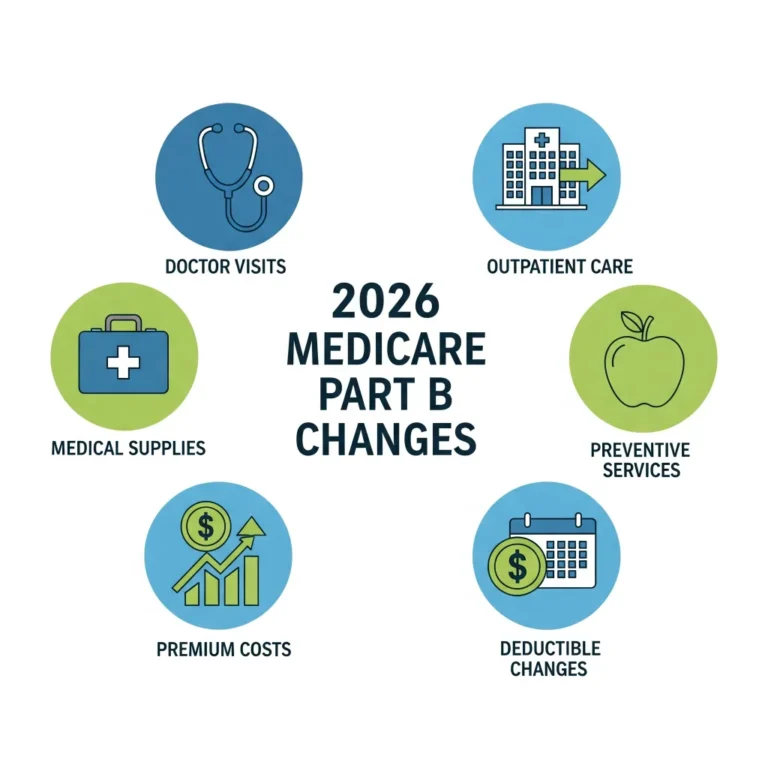

What Part B Covers:

- Doctor’s Visits: Including your primary care physician and specialists anywhere in the Tampa Bay area and beyond.

- Outpatient Medical Care: This includes services like outpatient surgery (perhaps at a Tampa surgical center), emergency room visits, lab work, X-rays, and chemotherapy.

- Preventive Services: Annual wellness visits, flu shots, and various cancer screenings available to Tampa residents.

- Durable Medical Equipment (DME): Items like walkers, wheelchairs, and oxygen.

- Ambulance Services and some other medical services and supplies.

The Significant Out-of-Pocket Costs of Medicare Part B Insurance Tampa FL (The Problem We Solve):

The costs for Medicare Part B Insurance Tampa FL are ongoing and, without additional coverage, completely uncapped. This presents a major financial exposure for Tampa seniors. For 2025, the projected costs for Tampa residents are:

- The Monthly Part B Premium: All beneficiaries pay a standard monthly premium, which is set by the government each year (projected to be around $178 for 2025). This amount is typically deducted directly from your Social Security check. Higher-income earners in Tampa, FL will pay more due to IRMAA.

- The Annual Medicare Part B Insurance Deductible: Before Medicare starts to pay, you must first pay an annual deductible for your Part B services (projected to be around $250 for 2025).

- The 20% Coinsurance: This is the single greatest financial risk in Original Medicare for our Tampa clients. After you have paid your annual deductible, you are responsible for 20% of the Medicare-approved amount for most doctor’s services and outpatient care. The most important thing to understand is that there is NO ANNUAL LIMIT on this 20% coinsurance. A serious illness with expensive treatments could leave a Tampa resident responsible for tens of thousands of dollars in a single year. Our entire job is to protect you from this unlimited risk.

Part 2: The Solutions We Offer – Private Plans to Manage Your Part B Costs

As an independent agency, we offer the two primary solutions Tampa, FL residents use to manage the uncapped costs of Medicare Part B. Your choice between these two paths in Tampa will define how you receive your healthcare in retirement.

A. Medicare Supplement (Medigap) Plans: The “Comprehensive Coverage” Solution

A Medigap plan is a private insurance policy that works with your Original Medicare. It pays for the costs that Medicare leaves behind.

- How It Works: You use your red, white, and blue Medicare card for all your Part B services. Medicare pays its 80% share first, and then your Medigap plan automatically pays its share.

- How It Covers Your Part B Costs: This is the core function of a Medigap plan. The most popular plan for new Tampa beneficiaries, Plan G, will cover your Part B costs almost completely. After you pay your small annual Part B deductible once per year, Plan G pays the 20% coinsurance for you, 100% of the time. This completely eliminates the risk of the uncapped 20% liability. Another popular option for Tampa residents, Plan N, also covers the 20% but requires you to pay a small copay (up to $20) for doctor visits.

- The Key Benefit for Tampa Residents: The biggest advantage of this path is freedom of choice. You can see any doctor in the entire United States, as long as they accept Original Medicare. There are no networks and no referrals needed. For Tampa’s “snowbirds” or anyone who travels, this provides unparalleled peace of mind. In exchange for this freedom and cost predictability, you will pay a monthly premium to the Medigap insurance company.

B. Medicare Advantage (Part C) Plans: The “All-in-One” Solution

A Medicare Advantage plan is a private insurance alternative that bundles all of your benefits into a single plan.

- How It Works: When you join a Medicare Advantage plan, you use the ID card from the private insurance company (e.g., Humana, UnitedHealthcare, Aetna) for all of your medical services. The private plan provides all your Part A and Part B benefits.

- How It Covers Your Part B Costs: Instead of paying the 20% coinsurance, you will pay the plan’s specific, predictable copayments for services. For example, a common plan structure in the Tampa Bay area might be a $10 copay for a primary care visit in South Tampa and a $45 copay for a specialist visit. You know your costs upfront.

- The Built-in Safety Net: Every Medicare Advantage plan has an annual Maximum Out-of-Pocket (MOOP) limit. This is the absolute most you will pay in a calendar year for all of your Part A and Part B covered services combined. This MOOP is the plan’s way of protecting Tampa beneficiaries from the unlimited 20% coinsurance risk of Original Medicare.

- The Key Benefit for Tampa Residents: The competitive Medicare Advantage market in Tampa leads to many plans with a $0 monthly premium and a rich package of extra benefits, including comprehensive dental, vision, and hearing coverage, which are not covered by Part B. The trade-off is that you must generally use the plan’s local Tampa network of doctors.

Part 3: Our Service Process – A Partnership for Your Healthcare Journey

Our goal as Tampa advisors is to be more than just an insurance agency; we want to be your trusted, lifelong advisor for all things Medicare. Our service process for Tampa residents is designed to be educational, thorough, and completely focused on your best interests.

- The Educational Consultation: We start with a no-cost, no-obligation meeting for Tampa residents to educate you on the foundational choices, especially how to protect yourself from Part B’s 20% coinsurance.

- The Comprehensive Needs Analysis: We take the time to listen. We’ll discuss your health status, your budget, your risk tolerance, and, most importantly, we will compile a complete list of your primary care doctors and specialists here in the Tampa area.

- The Unbiased Market Analysis: As an independent agency, we are appointed with all the major, top-rated carriers in Tampa, FL. We use our expert tools to analyze every single Medigap and Medicare Advantage plan available in your specific Tampa zip code.

- The Clear Recommendation & Enrollment: We will present you with the top 2-3 options that are the best fit for you, explaining the pros and cons of each in simple terms. Once you’ve made a decision, we handle the entire enrollment process for you.

- Lifelong Support: Our relationship doesn’t end after you enroll. We are your Tampa-based advocate. If you have a question about a doctor’s bill or a claim, you call us. Every year, we proactively contact our Tampa clients to conduct an annual review of your coverage.

Part 4: The Ultimate Vetting Checklist – 10 Questions to Ask Any Medicare Agent

Choosing the right agent in Tampa is just as important as choosing the right plan. Here are the ten essential questions you should ask any agent you consider working with.

- “Can you clearly explain how a Medigap plan versus a Medicare Advantage plan would handle the costs for an expensive outpatient surgery that costs $50,000?”

- Why it matters: This is a direct test of their ability to explain the core Part B risk. The answer should be: “With Original Medicare alone, you’d owe 20%, or $10,000. With a Medigap Plan G, you’d owe $0 after your deductible. With a Medicare Advantage plan, you’d pay a set copay for the surgery, maybe $500, and that amount would count toward your annual maximum out-of-pocket.”

- “Are you an independent agent, or are you a ‘captive’ agent who only works for one insurance company?”

- Why it matters: An independent agent works for you and can offer plans from a wide variety of companies. A captive agent can only offer you the products of their single employer.

- “What is your exact process for verifying that my primary care doctor and all of my specialists are in a Medicare Advantage plan’s network?”

- Why it matters: This tests their diligence. A great agent will never assume; they will use the insurance company’s official provider directory to meticulously check every single one of your Tampa-area doctors by name and location.

- “Is there any cost for your services, either now or in the future?”

- Why it matters: The answer must be “no.” Agents are compensated directly by the insurance companies when they help a beneficiary enroll. You should never be charged a fee for an agent’s help.

- “How do you help clients who are concerned about the monthly Part B premium? Do you help screen for Medicare Savings Programs?”

- Why it matters: This tests if their knowledge goes beyond just the insurance products. A knowledgeable agent will be aware of these state-run programs that can help low-income Tampa beneficiaries pay their Part B premium.

- “If I choose a Medicare Advantage plan, can you explain the difference between an HMO and a PPO, and which might be a better fit for me?”

- Why it matters: This tests their knowledge of the most common plan types here in Tampa. They should be able to clearly explain the trade-offs between the lower costs of an HMO and the greater flexibility of a PPO.

- “How do you stay up-to-date with the annual changes to Medicare plans, especially the constant updates to provider networks and drug formularies?”

- Why it matters: This tests their commitment to their profession. An expert will be ableto describe their annual carrier certifications and the professional tools they use to track changes.

- “What ongoing support do you provide if I have a question about a doctor’s bill or an Explanation of Benefits?”

- Why it matters: This tests their commitment to being your advocate. You want an agent who will be in your corner long after the sale is made.

- “If I choose a Medigap plan, how do you help me choose a carrier based on their rate increase history and financial stability?”

- Why it matters: This is a sophisticated Medigap question. Since the benefits are standardized, the key long-term differentiators are price and rate stability. An expert will have access to this historical data.

- “Why should I work with a local Tampa agent like you instead of just calling the 1-800 number on TV?”

- Why it matters: This asks them to directly state their value proposition. A great agent will explain that they provide personalized, local expertise, a wide range of choices, and serve as your personal advocate for life, which is something a national call center cannot offer.

Part 5: Red Flags vs. Green Lights – Making Your Final Choice of Agent

🚩 Major Red Flags to Run From 🚩

- Cannot clearly explain the unlimited 20% coinsurance risk of Original Medicare Part B.

- Represents Only One Company: They are a captive agent, not an independent broker looking out for your best interests.

- Does not meticulously check your doctor network for Medicare Advantage plans.

- Pushes one type of plan (e.g., only Medigap or only Advantage) without first conducting a thorough needs analysis.

- Uses high-pressure sales tactics or creates a false sense of urgency.

✅ Bright Green Lights to Look For ✅

- An Educational, Patient Approach: They focus on teaching you your options.

- Represents a Wide Range of Carriers: They are truly independent and can offer you a real, unbiased choice.

- Performs a Detailed, Personalized Needs Analysis, including a meticulous check of your doctors and prescriptions.

- Commits to a Lifelong Relationship with ongoing annual reviews and dedicated support.

- Feels like a trusted, local Tampa advisor.

Your Final Decision – Medicare Part B Insurance Tampa FL Residents

Protecting yourself from the open-ended and potentially catastrophic costs of Medicare Part B Insurance Tampa FL is the key to achieving financial security in your retirement healthcare here in Tampa. The choice you make between a Medigap plan and a Medicare Advantage plan will have a significant impact on both your monthly budget and how you access medical care for years to come.

You do not have to make this critical decision alone. By partnering with a knowledgeable, independent Tampa agent who is dedicated to your best interests, you gain a trusted advisor who can simplify the complex, provide you with the best options the market has to offer, and serve as your advocate for all the years to come.

Medicare Part B INSURANCE AGENT AND BROKER

As your Insurance Agent and Broker serving you, my goal is to “help you” and ensure, without a shadow of a doubt, that you and your family are secure and protected from risk. As a licensed Medicare Advantage and Medicare Supplement agent, I take the burden off your shoulders by doing a thorough needs analysis and researching the benefits best suited to you and your needs.

I can help you save on severe medical emergencies and find a plan that offers low- to no-cost doctor visits, prescription medication, and extra benefits such as dental, vision and hearing, gym membership, and over-the-counter items. I will show you plans where your doctors are in-network and a side-by-side comparison of your prescription costs with the different plans.

Medicare is constantly changing, and I work tirelessly to stay informed about the latest developments in the market. Not a year goes by without new government regulations, new or modified coverages, and new techniques for controlling benefit costs. To best serve their clients, professionals must understand each type of benefit or program’s provisions, advantages, and limitations to meet economic security.

I am a long-standing National Association of Benefits and Insurance Professionals® (NABIP.ORG) member and hold the prestigious Registered Employee Benefits Consultant® designation (https://nabip.org/professional-development/rebc-designation). I can provide information on your market’s availability and any expected changes.

After you choose your Medicare Insurance plan, I provide ongoing support all year; you won’t have to call an (800) number any longer.

If you have any questions, issues, or concerns about your plan’s benefits, you can contact me via phone, text, or my simple-to-use email contact form using the buttons below.

Steve Turner, your Helpful Licensed Agent and Broker

Medicare Part B Insurance Tampa FL FAQ

OUR CLIENT REVIEWS

CONTACT STEVE TURNER INSURANCE AGENT & BROKER

I’m here to take your calls and emails and answer your questions 7 Days a week from 7:00 a.m. to 8:00 p.m., excluding posted holidays.

Steve Turner is a licensed agent, broker, and a longstanding member of the National Association of Benefits and Insurance Professionals®. Steve holds the prestigious designation of Registered Employee Benefits Consultant®. NABIP® is the preeminent organization for health insurance and employee benefits professionals and works diligently to ensure all Americans have access to high-quality, affordable Healthcare, and related services.

Steve Turner is a licensed agent appointed by Florida Blue.

EMAIL ME: 24×7

OFFICE LOCATION

Website: steveturnerinsurancespecialist.com

Email: [email protected]

Phone and Text: +1-813-388-8373

Business Hours:

Monday: 7 am to 8 pm

Tuesday: 7 am to 8 pm

Wednesday: 7 am to 8 pm

Thursday: 7 am to 8 pm

Friday: 7 am to 8 pm

Saturday: 7 am to 8 pm

Sunday: 7 am to 8 pm

SOCIAL FOLLOW + SHARE

SERVICE AREA FACTS TAMPA FL

Tampa is a city on Tampa Bay, along Florida’s Gulf Coast. A major business center, it’s also known for its museums and other cultural offerings. Busch Gardens is an African-themed amusement park with thrill rides and animal-viewing areas. The historic Ybor City neighborhood, developed by Cuban and Spanish cigar-factory workers at the turn of the 20th century, is a dining and nightlife destination. ― Google

Population: 414,547 (2024)

Sales tax: 7.5% taxcloud.com

Area codes: 813, 656

Demonym(s): Tampan, Tampanian, Tampeño

Elevation: 48 ft (14.6 m)

Incorporated (City of Tampa): December 15, 1855 and; July 15, 1887

Incorporated (Town of Tampa): September 10, 1853 and; August 11, 1873

An Overview of Tampa, Florida

The city of Tampa is a vibrant hub on Florida’s Gulf Coast, known for its unique blend of historical charm, modern urban life, and stunning natural beauty. As a major city in the Tampa Bay metropolitan area, it has grown significantly in recent years, attracting new residents and visitors with its diverse culture, strong economy, and warm, subtropical climate. Tampa is much more than just a gateway to the Gulf beaches; it is a destination in its own right with a rich history and a bright future.

Key Statistics and Economic Drivers

- Population and Demographics: As of 2023, the city’s population is approximately 393,000, with an estimated metropolitan area population exceeding 3.4 million. The median age is around 35, making it a relatively young and dynamic city. Tampa is also racially and ethnically diverse, with a significant Hispanic or Latino population, a strong Black community, and a large number of foreign-born residents.

- Weather and Climate: Tampa’s weather is a major draw. The city has a humid, subtropical climate with two distinct seasons. The hot, humid season runs from May through October, with average daily highs in the low 90s °F. The milder, dry season from November through April sees average daily highs below 74°F. The warmest month is typically August, and the coolest is January.

- Economy: Tampa’s economy is robust and diverse. Key industries include financial and professional services, information technology, life sciences and healthcare, and defense and security. The city is also home to MacDill Air Force Base and a thriving maritime industry, with the Port of Tampa Bay being the largest in the state. Tourism remains a vital part of the economy, supporting tens of thousands of local jobs.

Top Places to Visit in Tampa

Tampa offers a wide array of attractions and activities for all ages and interests. You can find everything from thrilling amusement parks and world-class aquariums to historic neighborhoods and cultural gems.

- Busch Gardens Tampa Bay: A premier destination for adventure seekers, Busch Gardens combines a world-class amusement park with a zoo. Here you can ride some of the country’s most famous roller coasters, see exotic animals in natural habitats, and enjoy spectacular live entertainment.

- The Florida Aquarium: Located in downtown Tampa, the Florida Aquarium is a must-see for marine life lovers. It houses thousands of aquatic animals and plants from Florida and beyond. You can explore a simulated wetlands environment, a coral reef, and a huge tank with sharks, turtles, and other ocean inhabitants.

- Ybor City: Known as Tampa’s historic Latin Quarter, Ybor City is a National Historic Landmark District with a unique, vibrant atmosphere. You can explore the brick-lined streets, visit historic cigar factories, enjoy authentic Cuban and Spanish cuisine at the famous Columbia Restaurant, and experience the lively nightlife.

- ZooTampa at Lowry Park: This highly-rated zoo focuses on conservation and animal care. ZooTampa features more than 2,000 animals from Florida, Africa, Asia, and Australia, with many in naturalistic habitats. It’s a great place for families, offering animal encounters and interactive exhibits.

- Tampa Riverwalk: A scenic 2.6-mile path running along the Hillsborough River, the Tampa Riverwalk connects many of the city’s top attractions. You can stroll, bike, or jog along the waterfront, stopping at parks, museums like the Tampa Museum of Art, and dining spots such as Sparkman Wharf and Armature Works.

- Museum of Science & Industry (MOSI): MOSI provides an engaging and hands-on experience for visitors of all ages. You can explore interactive exhibits on a wide range of topics from outer space to the human body, participate in a ropes adventure course, and watch educational films in the IMAX theater.

- Adventure Island: If you need to beat the Florida heat, Adventure Island is the perfect place. This tropical-themed water park offers thrilling water slides, a lazy river, wave pools, and other splashy attractions, providing fun for the entire family.

- Henry B. Plant Museum: Housed in the beautiful Victorian-era Tampa Bay Hotel, the Henry B. Plant Museum showcases the lavish lifestyle of America’s Gilded Age. You can step back in time and view original furnishings and artifacts, learning about the history of the railroad and the hotel’s role in the Spanish-American War.

MEDICare Part B INSURANCE POSTS

SERVICE AREA

MEDICARE STATEMENT

The Medicare Annual Enrollment Period is October 15th to December 7th. Steve Turner is not connected with or endorsed by the United States Government or the Federal Medicare Program. Some plans may not be available in your area, and any information I provide is limited to those offered. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options.

There’s no one-size-fits-all answer. Carefully evaluate your health status, anticipated medical needs, prescription drug usage, budget, preferred doctors and hospitals, and tolerance for network rules. During the Medicare Annual Enrollment Period (October 15th to December 7th), thoroughly research the specific plans available in your Florida county using the Medicare Plan Finder on Medicare.gov, compare their costs and benefits, and consider seeking free, personalized counseling from Florida’s SHINE (Serving Health Insurance Needs of Elders) program.